Treasurer Scott Morrison has used Donald Trump’s Presidential victory and yesterday’s weak wages growth to spruik for cutting Australia’s company tax rate. From The AFR:

The Coalition has seized on weak wage growth to fire up support for company tax cuts amid warnings from business that Australia must match Donald Trump ‘s own tax cut plans or miss out on up to $400 billion in global investment.

Treasurer Scott Morrison warned that failure to keep pace with President-elect Trump’s plan to lower the US company tax rate to 15 per cent from over 35 per cent will erode Australia’s competitiveness because its rate would be double the US, hurting profitability and ultimately workers’ wages…

Mr Morrison said the slump drives home the need for the tax cuts he argues would generate stronger economic growth, and boosts profits “which will then support higher wages growth”.

“With the rest of the world looking to stimulate investment and growth through more competitive tax rates, Australia, as a net importer of capital, risks falling behind and becoming uncompetitive.”

Scott Morrison is obviously an avid believer in “trickle down economics”: the notion that if you cut tax rates at the top, it will magically flow down to lower paid workers. It’s a curious position given both the Coalition and business groups are the ones that fight hardest against raising the minimum wage on the grounds that such wages growth is “unaffordable” and “harmful” to the economy. Would they change track if company taxes are cut?

Yet again, Scott Morrison has ignored several inconvenient truths around cutting company taxes.

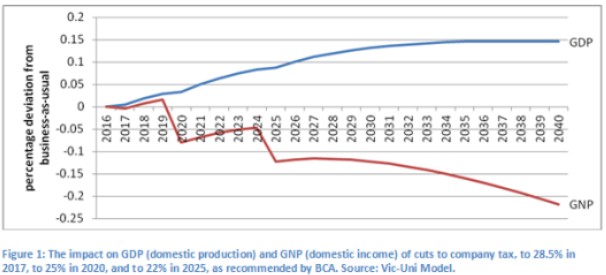

First, there is a strong argument to be made that cutting company taxes would lower national income, which is a far better measure of living standards than GDP (see below chart).

Australia’s unique dividend imputation system means that domestic investors/owners are largely unaffected by the company tax rate, since any profits paid to them are taxed at their personal income tax rate.

Hence, lowering the company tax rate would provide local owners and shareholders with minimal benefits, since any reduction in company taxes would be offset by a commensurate reduction in imputation credits.

By contrast, foreign owners/shareholders are major beneficiaries of a company tax cut because they cannot avail themselves of imputation credits. So a cut to the company tax rate provides them with the lion’s share of the benefits, and therefore represents a transfer from Australian taxpayers to foreign owners/shareholders, hence lowering national income.

Moreover, because of Australia’s dividend imputation system, many of the international studies about the economic impacts of cutting company tax rates, as well as comparisons of company taxes across nations, are not readily applicable to Australia.

Second, the huge cost to the budget from cutting company taxes would need to be made up by either raising taxes elsewhere or cutting government expenditure on public services and/or infrastructure. Such actions would necessarily act as a drain on economic activity, thus counter-acting any benefits from cutting company taxes.

Indeed, the most likely ‘victim’ of company tax cuts would be personal income taxes, which would need to rise to make up the revenue shortfall. As noted by The Australian’s David Uren recently:

Scott Morrison has described “bracket creep” as a “silent tax”, warning that it erodes incentives to work…

Parliamentary Budget Office estimates done for the Labor Party show the cost of the company tax cuts will rise from $1.5bn in 2019-20 to reach $7.6bn by 2024-25 and $14.2bn by 2026-27. In that final year, the tax cuts are equivalent to 0.5 per cent of GDP…

If personal income tax had to cover the full cost of the company tax cuts, it would rise to about 13 per cent of GDP — its highest level since 1988.

So Morrison is arguing to boost wages via a company tax cut, even though the same company tax cut will likely lead to an increase in personal income taxes? Doesn’t make a whole lot of sense, does it?

Finally, the modelling used to support the company tax cut showed minimal benefits to either GDP or employment, as explained by The Australia Institute’s Richard Denniss:

According to Treasury’s in-house modelling, and the modelling it commissioned from Chris Murphy, if the company tax rate is lowered from 30 per cent to 25 per cent then gross domestic product will double by September 2038, while without the tax cut it won’t double until December 2038. Wow, a whole three months earlier. Both modelling exercises conclude that in 20 years’ time the unemployment rate will be 5 per cent regardless of whether we spend $50 billion on company tax cuts or not…

The “benefits” are more accurately described as rounding error than significant reform.

The Grattan Institute came up with similar conclusions, while also noting that national income would likely be lowered by cutting company taxes, at least over the first decade.

Presumably for these reasons, former Treasurer Peter Costello last month claimed that the Coalition’s company tax cut policy lacked funding, balance or coherency. And he’s right.

With the Federal Budget facing immense structural pressures and a “revenue problem” – as acknowledged by Treasurer Scott Morrison in his recent speech – there is little sense in gifting tens-of-billions of dollars to foreign owners/shareholders, and in the process worsening the Budget position and lowering national income.

The are far greater national priorities than cutting company taxes. Scott Morrison just needs to take the blinkers off.

unconventionaleconomist@hotmail.com