Since the Turnbull Government announced on Budget night that it would cut the company tax rate from 30% to 25% over a decade, this site has waged a war against the proposal.

Our concerns centre around two main issues.

First, the benefits from cutting company taxes would primarily flow offshore to foreign owners/shareholders. To understand why, one needs to understand Australia’s dividend imputation system.

Local owners of unincorporated businesses are essentially taxed at their personal tax rate, because of dividend imputation. Hence, lowering the company tax rate from 30% to 25% would provide local owners and shareholders with minimal benefits, since any reduction in company taxes would be offset by a commensurate reduction in imputation credits.

By contrast, foreign owners/shareholders are major beneficiaries of a company tax cut because they cannot avail themselves of imputation credits. Since most of the BCA’s big business members have some degree of foreign ownership, it is they that reap the lion’s share of benefits from any company tax cut.

Former Treasurer and Prime Minister, Paul Keating, explained it best when he penned the following earlier this year:

“Australia’s dividend imputation system works such that the company tax is, in effect, a withholding tax – a tax temporarily held by the Commonwealth which is returned to shareholders when their dividends are paid. So, whether the company tax is withheld by the Commonwealth at a rate of 30% or 25% is immaterial – the Commonwealth is going to return the money to shareholders anyway, regardless of the rate. But the shareholders who will receive a benefit are foreign shareholders”.

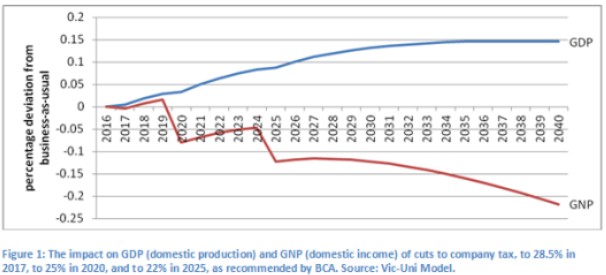

For this reason, modelling from Victoria University senior research fellow, Janine Dixon, found that cutting the company tax rate would actually lower national income (GNP) and living standards because of the benefits flowing offshore:

Our second (and related) reason for opposing a company tax cut is that its huge cost to the budget would need to be made up by either raising taxes elsewhere or cutting government expenditure on public services and/or infrastructure – neither of which is a desirable outcome.

On this matter, The Australian’s David Uren has today reported that the cost of cutting company taxes would most likely be borne by Australian workers via higher taxation:

…the budget’s medium-term projections show the cost of the company tax cuts, which rises to $14 billion a year, is intended to have no effect on the budget bottom line.

Treasury officials confirm this means that if one revenue source is falling as a share of GDP, there would have to be a combination of other revenue sources rising…

Grattan Institute executive director John Daly said the government needed to tap a revenue source that was growing faster than the economy. “They are relying on a source of revenue that increases as a percentage of GDP and the only thing that I know that looks like that is PAYG, with every other major revenue source rising at the same pace as GDP,” he said…

Scott Morrison has described “bracket creep” as a “silent tax”, warning that it erodes incentives to work…

Parliamentary Budget Office estimates done for the Labor Party show the cost of the company tax cuts will rise from $1.5bn in 2019-20 to reach $7.6bn by 2024-25 and $14.2bn by 2026-27. In that final year, the tax cuts are equivalent to 0.5 per cent of GDP…

If personal income tax had to cover the full cost of the company tax cuts, it would rise to about 13 per cent of GDP — its highest level since 1988.

Treasury projections released last year (i.e. well before the company tax cut plan was announced) already showed that the share of taxation collected through personal income taxes would rise inexorably over the next decade as bracket creep (aka “fiscal drag”) increases workers’ tax burdens:

And that this result was undesirable:

As a result, without conscious change, the economic cost of raising tax from our current tax mix will also increase. Many studies, both in Australia and internationally, have suggested that reducing reliance on direct taxes would lead to higher incomes…

A higher tax burden reduces the immediate reward for effort. At low levels of income, it can be a barrier to participation.

At higher levels of income, a rising personal tax burden increases the benefits from tax planning and tax minimisation.

With the Federal Budget facing immense structural pressures and a “revenue problem” – as acknowledged by Treasurer Scott Morrison in his recent speech – there was never any sense in gifting tens-of-billions of dollars to foreign owners/shareholders, and in the process worsening the Budget position, lowering national income, and penalising Australian workers.

The Turnbull Government signaled last week that it would abandon company tax cuts for big business. Let’s hope it follows through.