‘Free market’ IPA champions negative gearing rort

You’ve gotta love the right-wing think tank, the Institute of Public Affairs (IPA), the self proclaimed “voice for freedom”.

One of its senior research analysts, Sinclair Davidson, has published an occasional paper entitled “What politicians need to know about negative gearing”, which lobbies against reform. Let’s take a look at Davidson’s key arguments.

Davidson begins his salvo by repeating the myth that “low and middle income earners benefit most from negative gearing. To abolish negative gearing would make investment more difficult for low and middle income earners”. He then backs up his claim by stating that “80% of net taxpayers have taxable income of less than $90,000 while 80% of Landlords claiming an interest deduction have a taxable income between $100,000 and $150,000”.

First of all, I find it hilarious that Davidson has set $100,000 to $150,000 as the threshold for a “low to middle income” property investor. This makes absolutely no sense given that the average taxable income in 2012-13 (the latest ATO data that he draws upon) was just over $55,000.

Further, as has been argued ad nauseam on this site, the ATO’s statistics are flawed for this purpose because they measure “taxable income”, which is what is left after deductions like negative gearing. They also do not take account of tax-free income like superannuation earnings for over-60s.

But don’t just take my word for it. Here’s the RBA’s head of financial stability, Luci Elliss’ opinion on the matter:

The Property Council has cited Australian Taxation Office statistics to prove cutting negative gearing would hurt many people on low and middle incomes. It says 66.5 per cent of investors who made a loss on a rental property had taxable income of $80,000 or less.

But Dr Ellis said the RBA analysis was based on the Household, Income and Labour Dynamics survey which covers all income and all households while the Tax Office data cited by the Property Council only looked at the taxable incomes of people who lodged tax returns.

Dr Ellis said because of these limitations the ATO figures do not capture the fact that many negatively geared properties are owned by people with low taxable income but high “actual income”, mostly because they were drawing untaxable income from superannuation [or reducing taxable income via negative gearing].

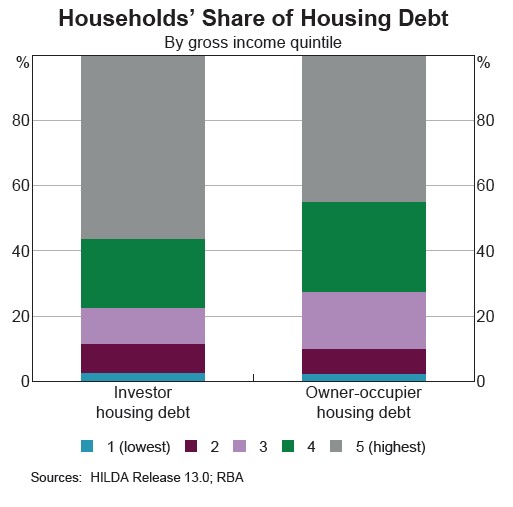

The RBA has also produced the below chart showing that nearly 80% of investment property debt is held by the top 40% of income earners:

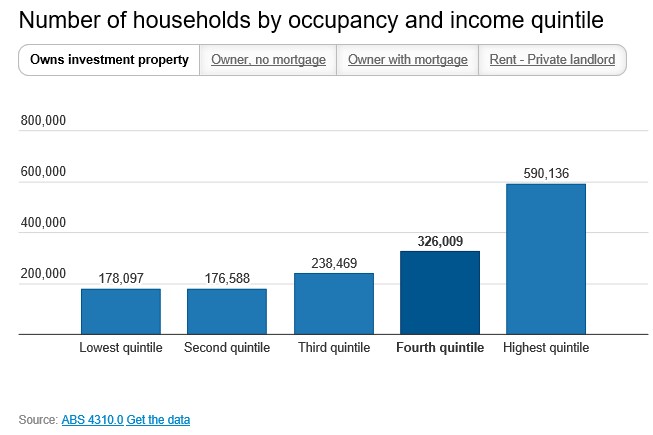

The ABS’ latest housing occupancy and cost data also showed that the richest 20% of households accounted for 39% of all housing investors, with the top 40% of households accounting for 61% of all housing investors (chart from Greg Jericho):

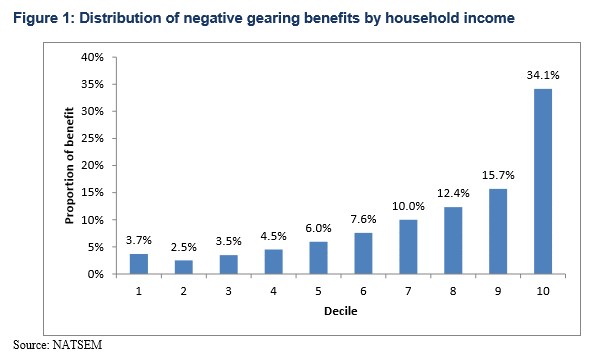

Whereas modelling last year from the National Centre for Social and Economic Modelling (NATSEM) revealed that one third (34.1%) of the benefits of negative gearing were captured by the top 10% of income earners, whereas 15.7% of negative gearing benefits goes to the next 10% of income earners (see next chart).

So, whichever way you cut it, Davidson’s claim that “low and middle income earners benefit most from negative gearing” is complete and utter rubbish.

Davidson’s next line of argument is that “changing negative gearing will make it more difficult for these [so-called low and middle income] Australians to provide for themselves in retirement”. He then goes on to argue that “being a landlord offers an opportunity for low and middle income earners to develop their own business and so build up a nest egg for retirement. At the same time they provide valuable housing stock and residential space to the population…

Let’s get a few things straight. Only one-in-10 taxpayers are negatively geared property investors. They are making life more difficult for the other 90% by bleeding the Budget of billions of dollars in tax revenue and inflating the cost of housing. They are also doing absolutely nothing to “provide valuable housing stock and residential space to the population“, given that nearly 19 out of 20 property investors purchase existing homes. All they are doing is substituting homes for sale into homes for let.

It stands to reason, then, that the retirement prospects of the majority of the population would be improved by negative gearing’s removal. Homes would be cheaper, meaning that households would not need to devote as much of their lifetime’s earnings to pay them off. There would be more Budgetary revenue, leaving room for tax cuts or increased spending on services. And there would be no impact on the rental market.

Prosper’s Dr Gavin Putland explains the fallacy of Davidson’s argument well:

If you want to retire in reasonable comfort, it helps to own your home outright, so that you are not burdened with rent or mortgage payments after you stop working. Hence you want to be able to buy your first home while you are still young enough to pay off the mortgage. Hence you don’t want to be competing with investors who can augment their borrowing capacity through the negative-gearing deduction while you can’t. While you are still renting, you want the rent to be low enough to leave you enough spare income to save a deposit. Hence you want negative gearers to add to the overall supply of housing — not merely outbid prospective owner-occupants for established homes, turning homes-for-sale into homes-to-let and throwing the prospective owner-occupants onto the rental market. And if your circumstances are such that home ownership is not a realistic option, you want the rent to be low enough to leave you enough spare income to save for your retirement in other ways…

Only to the extent that landlords contribute to the rate of construction can we conclude, as Davidson does (p.15), that “they provide valuable housing stock and residential space to the population.” Otherwise, concerning the alleged opportunity to “build up a nest egg for retirement”, we must ask “Whose retirement?”

Davidson ends by arguing that “the tax system should encourage entrepreneurship and risk-taking”, and that “ this is something that should be applauded not penalised through the tax system”, and to remove negative gearing would “constitute a distortion in the economy”.

There is nothing “entrepreneurial” in using taxpayer lurks to purchase an existing dwelling. It does nothing for the real economy. And it is these tax lurks – negative gearing and the CGT discount – that are causing great distortion by channeling excessive investment into housing, most of it pre-existing dwellings. Even the timid RBA acknowledged these distortions in its June 2015 submission to the Home Ownership Inquiry:

The Bank believes that there is a case for reviewing negative gearing… the interaction of negative gearing with other parts of the taxation system may have the effect of encouraging leveraged investment in property. In particular, the switch in 1999 from calculating CGT at the full marginal rate on the real gain to calculating it as half the taxpayer’s marginal rate on the nominal gain resulted in capital gain-producing assets being more attractive than income-‐producing assets for some combinations of tax rates, gross returns and inflation.

This effect is amplified if the asset can be purchased with leverage, because the interest deductions are calculated at the full marginal rate while the subsequent capital gains are taxed at half the marginal rate. Since property can usually be purchased using higher leverage than other assets that produce capital gains, property is especially affected by this feature of the tax system.

And here I was thinking that the IPA was supposed to be dedicated to “free” markets without distortions. I guess not.

unconventionaleconomist@hotmail.com