Stocks keep trying and failing to rally, media keeps telling punters to buy and trashing its credibility, the sell side is focused on this tactical cause or that without tying it all together. Yet it is not over. The Mining GFC is a very large unwind born of two business cycles:

- the post-millennial global business cycle was characterised by the rise of ‘Chimerica’, an unprecedented unity of super-powered economies in the US and China where the former consumed and the latter exported both goods and capital to the other;

- that enabled the US to run super low interest rates and a low currency even as its current account and fiscal deficits exploded. Other developed markets took the hint and did the same;

- it enabled the rising power in China to supercharge its growth via supply side expansion which in turn drew in huge quantities of commodities as it modernised its entire capital base;

- the globe’s “emerging markets” (EM) took the hint and followed suit, also exporting goods and capital to the US while also massively expanding their commodity supply for China;

- chapter one of the cosy relationship ended in the GFC when the US (and other DMs) hit peak debt in its housing market and its banks, which were importing all of that EM capital, imploded;

- but it was not the end yet for Chimerica. Now China stepped up with massive domestic stimulus and the US crashed its interest rates and dollar. The result was a blow off cycle for commodity prices, demand and production as Chinese capital exports reversed;

- the boom was so gigantic that even non-commodity intensive economies like the US figured out ways to cash in by developing new techniques for drawing oil literally from stone;

- the US productive economy rebounded as it slowly deleveraged and repaired its deficits;

- but that now meant that its interest rates and currency would rise and the capital flood powering EMs began to reverse;

- China found itself enormously oversupplied in just about everything and the debt that was powering its domestic construction took on bubble-like proportions so it was forced to slow lest it implode like the US before it;

- the EMs had all assumed that the boom would run forever and had dramatically over-invested in commodity supply expansion so as the US slowly repaired and China slowed, they faced a crash in commodity prices;

- but the commodity gluts were now historically vast and despite everyone’s best efforts to ration supply, the glut of everything was far too big to be grown out of;

- worse, commodity supply expansion had itself constituted such a huge component of the global growth cycle that as it was cut, growth slowed and commodity demand fell.

That’s where we are now. MB reckons that the odds now favour an end only when commodity prices fall to historical lows so deep that it triggers a new global crisis in commodity debt that crashes global supply via a balance sheet recession.

To understand the lineaments of this cycle you need to have been around for the last one as well. Perhaps that’s why markets, staffed with juiced-up kids, can’t seem to remember! Most importantly, understand that no policy measure that boosts the US dollar in any way can succeed in ending the rout and that includes just about any monetary measure to stimulate the global economy outside of the US Federal Reserve and possibly not it, either, if everyone else is printing money just as fast or faster.

And so we move to overnight action which saw a firm US dollar:

Brent oil trying but largely failing to rally:

Base metals likewise:

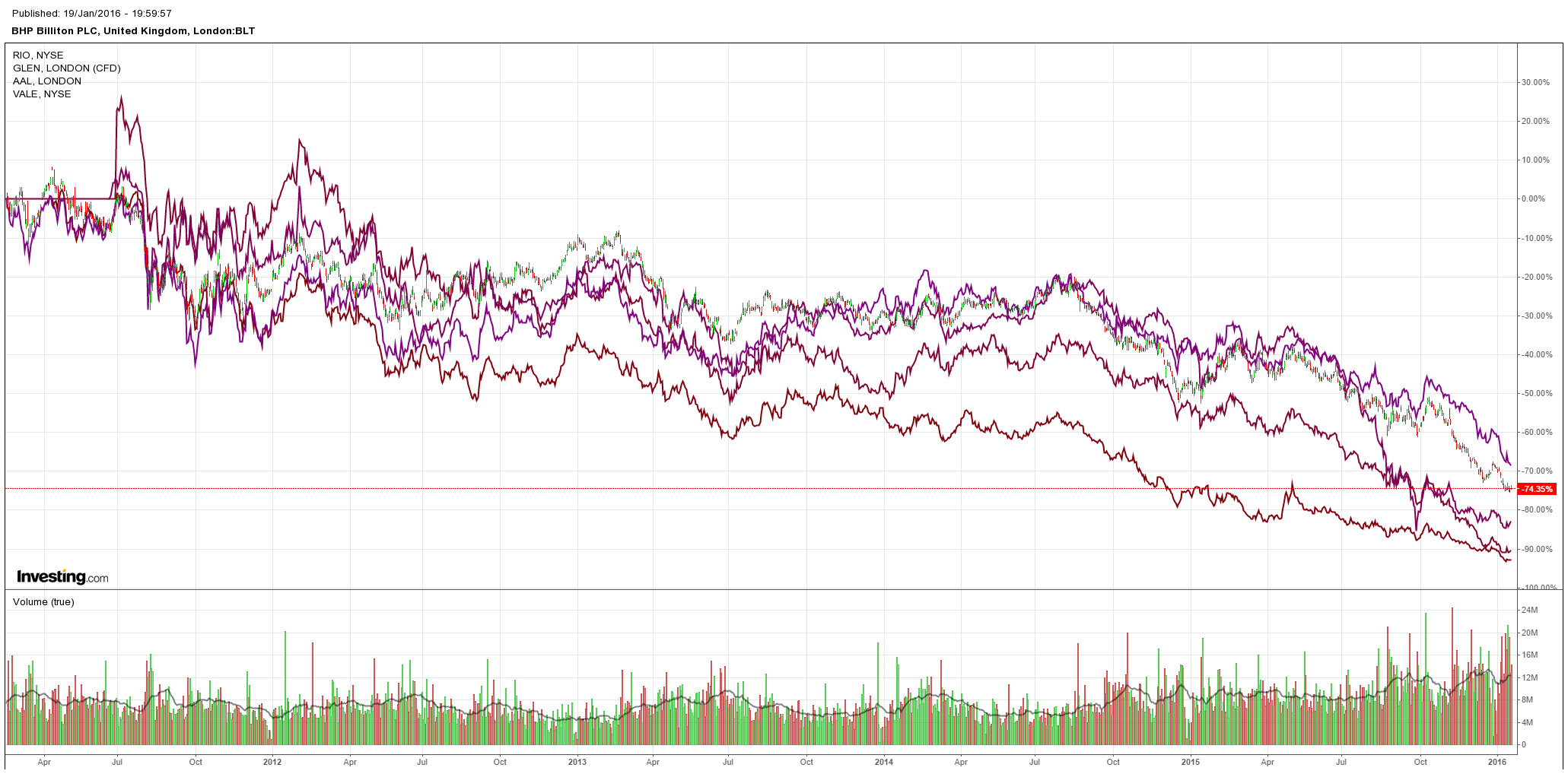

And big miners:

Commodity currencies did catch a little bid:

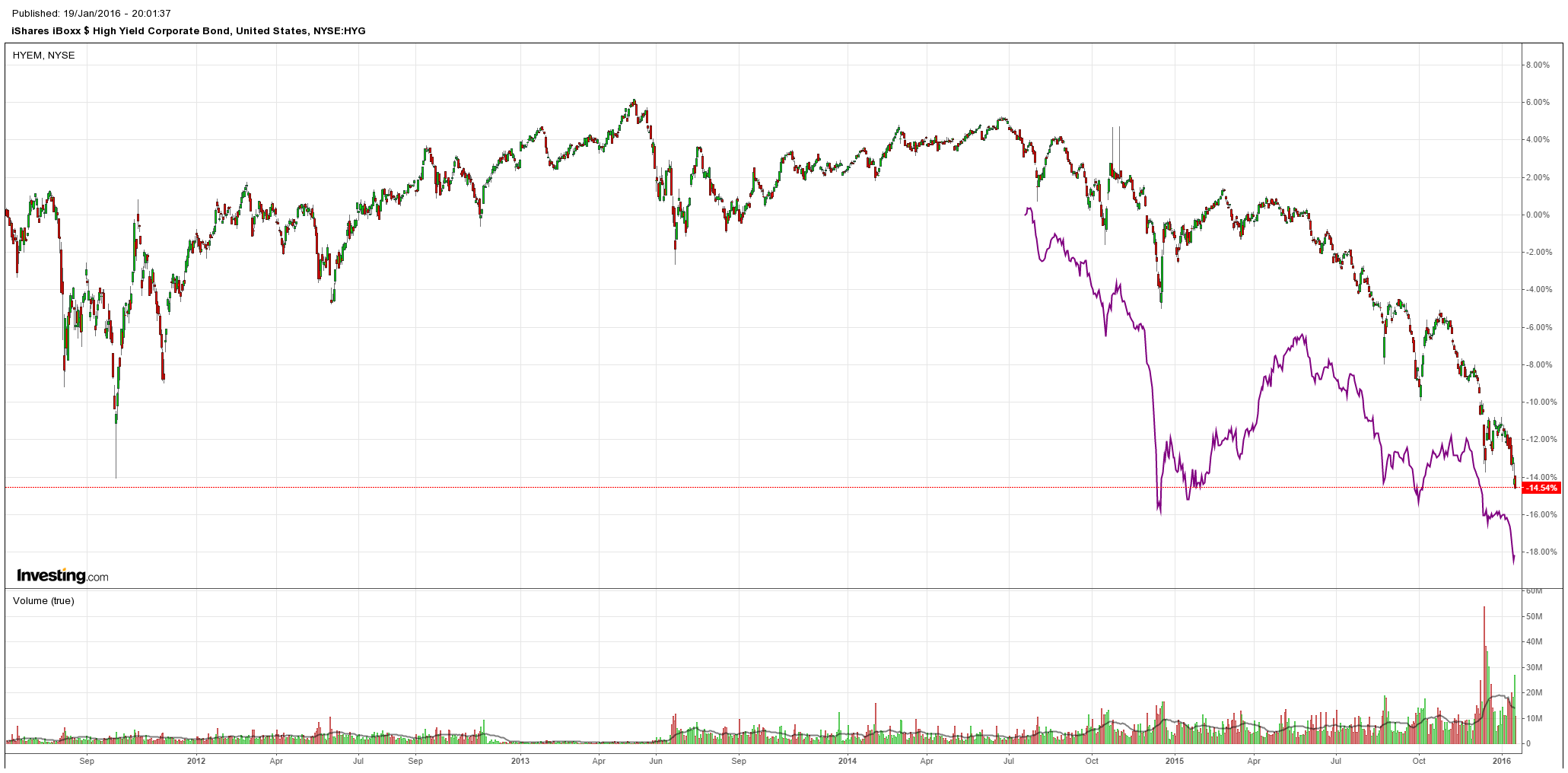

But, crucially, US high yield debt kept sinking as its energy sector reels (EM was slightly better):

There will be ebbs and flows but it will not be over until commodity prices are so low that the debt underpinning the oversupply at the margin implodes which will very likely end the business cycle itself.