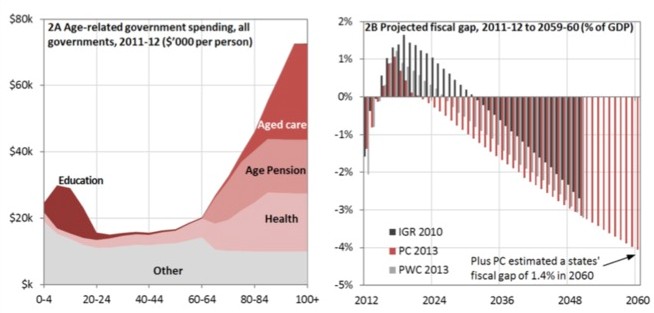

Earlier this week, I argued that for the Government’s so-called crack-down on welfare payments to be credible, it must include the retirement and pension system, which is one of the biggest and fastest growing areas of Budget expenditure (see next chart).

The Government later confirmed that its review of the welfare system would only focus on the Newstart and disability pensions, whilst ignoring retirees receiving government support.

Advertisement

Today, a bunch of reports are out confirming my view that it is the aged, not working-aged Australians, that are causing the increase in welfare spending.

The first, from Toni Wren, debunks Social Services minister, Kevin Andrews’, claim that there has been unsustainable welfare “blowouts”, whist also showing that it is the aged that are primarily responsible for the increases in welfare spending over the past decade:

The figures Minister Andrews were referring to show that just over 5 million Australians were dependent on income support as at June 2012.

The minister then concluded that this number was a “blowout” compared to a decade earlier.

A closer examination finds the total number has gone up by 4 per cent over the decade…

ABS demographic statistics tell us our nation’s population grew by 15 per cent over the same period. So welfare numbers increased 4 per cent while the population increased 15 per cent.

Actually, that means welfare numbers went down as a proportion of the population over the decade, so where is the blowout?..

In June last year, the largest group were age pensioners – nearly 2.3 million recipients – an increase of 26 per cent over the last decade. This is, of course, due to the ageing of the population, but also due to the relaxation in the income and asset tests undertaken by the Howard government, which entitled more people to a part-pension (and then the flow-through when the former Labor government increased the weekly rate by $30).

Minister Andrews has ruled out any changes to the age pension in the review currently under way. But he did say the government was examining the Disability Support Pension. In June last year, there were just under 830,000 people reliant on this payment – just over a third of the total number of age pensioners.

Advertisement

A similar view has been taken by The Guardian’s Greg Jericho, who argues that the the welfare debate scapegoats the unemployed and disabled and ignores the rising number of Australians on the age pension:

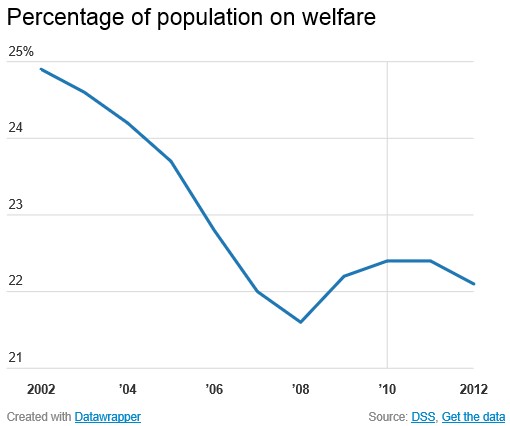

…the percentage of the population on welfare has fallen significantly over the past decade. In 2002 it wasn’t one in five on welfare, it was one in four. Since 2008, rather than an unsustainable growth, the percentage of those on welfare has risen from 21.6% to 22.1%.

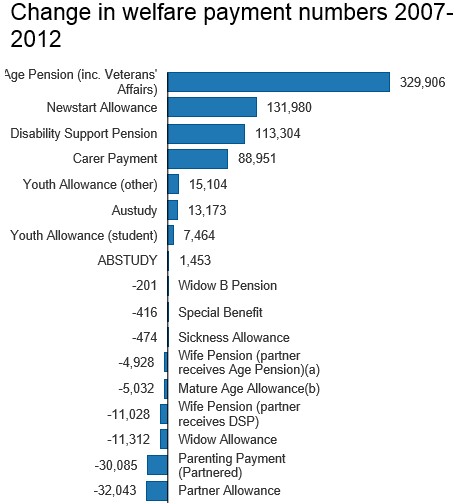

And if we look at the “dramatic” increase since 2007, a rather different picture emerges than one Andrews would suggest wherein the major problem is the growth of people on disability support pensions (DSP) and Newstart:

Seventy-one percent of the increase in welfare payments from 2007 to 2012 was in age pension payments. Rather oddly, this is the one payment area which Andrews is ruling out being considered in the review chaired by Patrick McClure…

Twenty years ago there were almost six people in the labour force for every person on the age pension. Now it is down to 5.3 people per pensioner and the trend is heading further down.

The welfare problem is by and large an ageing population problem. And it is a problem that will be much better served with a bit more context and a lot less of political parties blaming each other, the unemployed or those on disability pensions.

As noted by Toni Wren above, one of the reasons for the blow-out in aged pension costs is the relaxation in the income and asset tests undertaken by the Howard Government, as well as the $30 weekly increase in the pension granted by the former Labor Government. According to Curtin University’s Alan Tapper, Alan Fenna and John Phillimore, these changes led to a marked increase in benefits paid to the aged:

Advertisement

What stands out is the recent surge in net benefits, which took place mostly under Coalition government. Critics might argue that in this period the long Australian tradition of relative restraint on expenditure on the elderly, under both Labor and Coalition, was here abandoned…

Perhaps most alarmingly, the Curtin University study also found that the bulk of assistance provided to the elderly is not based on need, but purely aged-based, with elderly Australians tending to be quite well-off when compared against younger Australians:

We might suppose that increasing support for the elderly is an expression of increased recognition of need. To test this claim we need to be able to rank ‘neediness’. This can be partly done in terms of ‘equivalent final incomes’… Table 6 shows the equivalent final incomes of the elderly and all households. Note that this table exaggerates the increase in EFI between the two surveys, because here the EFI for 2003–04 has not been adjusted by the CPI. The point of the comparison is not the relative change between 2003–04 and 2009–10 within each group, but the gains and losses of the different groups relative to each other in this period.

…the most interesting comparison is that with all households. Rapid gains to the elderly in this period have brought them close to the EFI for all households. The gap in 2003–04 stood at about 21 per cent (based on an estimate that the EFI for all elderly households was about 505). In 2009–10 it had fallen to only about five or six per cent (estimating that the elderly EFI was about 960)…

As Table 7 shows, wealthier households are older households. Net worth peaks at around age 60. A sharper picture is obtained if we take household size into account using equivalence scales. Here we have used the square root of household size (a method that approximates quite closely to the ‘OECD modified’ scale used by the ABS to calculate equivalent final incomes). The resulting ‘equivalent net worth’ indicates that even households aged 75 and over are one-third better off than the mean for all households, while households in the 65–74 age group are 60 per cent better off than the mean…

Given that equivalent final incomes for the elderly are now close to the average for all households, and that the net-worth distribution is skewed in favour of older households, we can reasonably infer that an integrated measure would show that households headed by persons 65 and over are better off than the average for all households under that age.

If all this is right, the Australian system of social transfers to the elderly is much more than a safety net. Viewed in ‘lifecycle’ terms, it shifts resources from the income-rich but asset-poor stages of life to the asset-rich but income-poor stage. Viewed in terms of the ‘vertical’ dimension, it is a system of upwards redistribution from the less well off to the better off…

Advertisement

It is inappropriate for the Coalition to only focus welfare cuts on the working-aged population, whilst ignoring the swathes of wealthy retirees receiving government support. Such an approach is not only inequitable and inconsistent, but also places the Budget in a precarious position as the population ages.

Instead, in addition to overhauling Australia’s superannuation system so that tax concessions are more evenly spread and balances are not exhausted too quickly, means testing of the aged pension must be tightened to ensure that it goes only to those retirees most in need (see here).

Otherwise, the shrinking working-aged population will be left to bear the brunt of Budget expenditure cuts at the same time as it incurs the cost of supporting its relatively well-off parents.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.