By Chris Becker

Well Friday capped off a good week if you were long risk, although on the day the ASX200 disappointed. With the most closely watched economic release of the month – US non-farm payrolls (or NFP) or broad unemployment numbers – coming in unexpectedly good on Friday night, this sent 10 year treasuries selling off as US equity markets were bid up.

The commodity complex also responded with copper up nearly 4% on LME, alongside other base metals and WTI Crude futures and spot also responded strongly. Notably ICE was subdued and Natural Gas fell over 6%, but AUDUSD was very bullish rising above 1.03 or nearly 2/3rds of a cent. Most institutions are expecting Chinese markets – and our own materials sector (XMJ) to rally come Monday…

This spells risk-on.

Remember, the following views are my own, do not constitute advice and are for information purposes only. I may have positions in any or all of the below and their associated markets both long and short, on an intra-day, daily and weekly basis for my own account. Please seek advice from a licensed adviser before making any investment decisions.

Commodities

First, let’s look at commodities because its here we are seeing some rebounds, and as I suggested a few weeks back an overly strong bearish attitude has indeed turned into a bounce in commodity stocks and indices.

For Australian investors particularly, there’s three major commodities to watch: crude oil, copper and iron ore. I’ll leave the last to Houses and Holes with his excellent daily updates (although it’s non tradeable for retail/private investors – Fortescue Metals (FMG) and Atlas Iron (AGO) both of which I trade regularly as proxies).

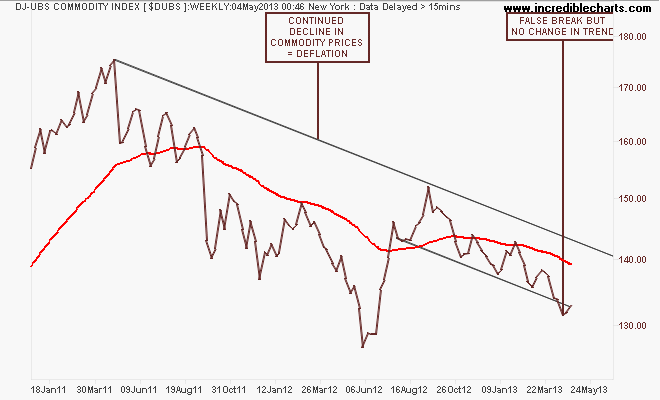

The medium term view in commodity prices is summed up in the DJ-UBS Commodity Index, a basket of commodity future prices. The trend is still clear, from the mid-2011 high, with a recent breakdown in the trend channel proving false, but no apparent change in trend for now:

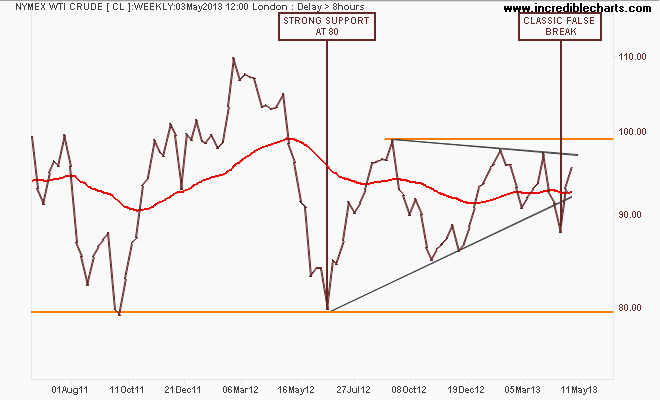

Looking at the main components, the most closely watched – WTI Crude – had recently broken down out of its ascending triangle pattern in what has been a false break. This is very bullish – a failed breakout usually means the underlying pattern bias is strong as this has wiped out the shorts and only longs remain. The target to watch is above $96USD per barrel and then above $100USD for the full enchilada:

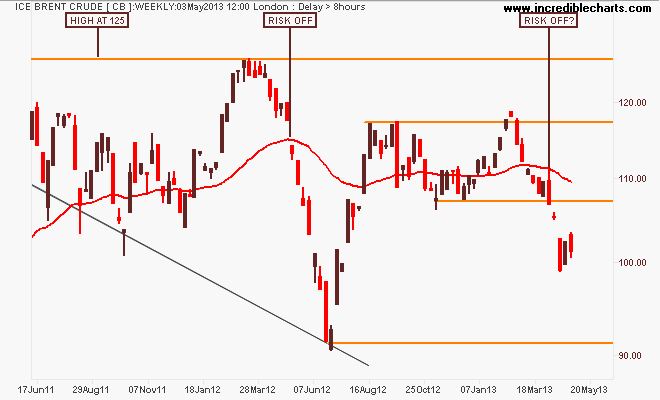

ICE Brent Crude – a marker of European demand – is not reflecting this bullishness and on the weekly chart is still signalling a bearish 2nd quarter with strong resistance overhead which I still think reflects the weak European post-Christmas cycle:

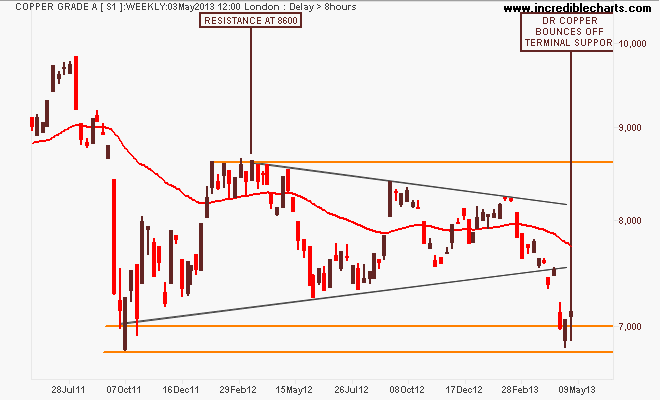

Finally, Dr Copper (so called because its the only “real” economic expert out there) has bounced off its September 2011 lows this week. Using the weekly chart of the London spot price, the symmetrical triangle pattern – an indication of a stalemate between bulls and bears – had broken to the downside and was on its way below terminal support at 7000. The last couple of weeks, perhaps in reflection of gold’s rebound, has shown strong support for the key industrial metal – can this continue? This week’s long tail under the candle suggests so:

While gold (which we’ll see in the next section) has rebounded some from its crash in the last few days, and the best proxy for commodities – Chinese equity markets (and hence ASX200 Materials) may have also found some light at the end of a dark tunnel, commodity prices themselves remain quite bearish.

Currencies and Gold

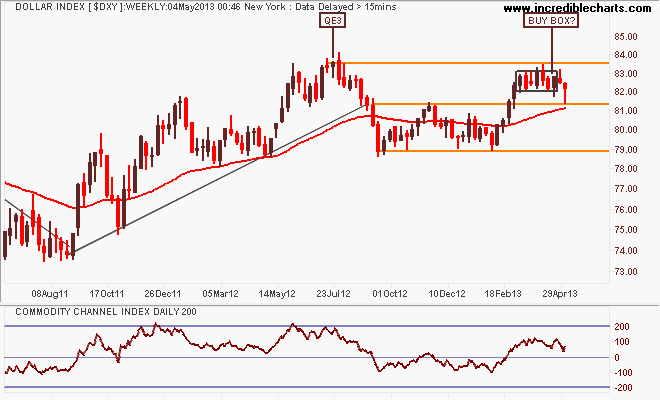

The US Dollar Index (DXY), made up of a basket of major currency pairs against the USD is a good way of measuring the so-called “risk on/risk off” meme prevalent in asset markets, with a lower USD usually meaning higher risk as US stock markets rise and push other risk assets higher, such as our own share market.

On the weekly chart you can see that King Dollar has attempted to breach its pre QE3 high forming a “buy box” recently. However this week we’ve seen it move down to its former resistance, now support like at 81.5 points and finishing the week…err…weak:

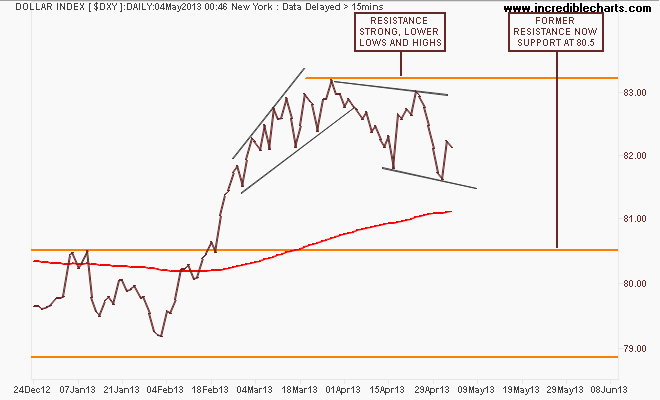

Whilst my long term oscillator in the chart above (200 day CCI) remains a long bias, here’s the daily chart showing some short term weakness baking in to the USD, with a series of lower highs and lows after the successful bearish megaphone blowoff – a target of 80.5 points is possible here:

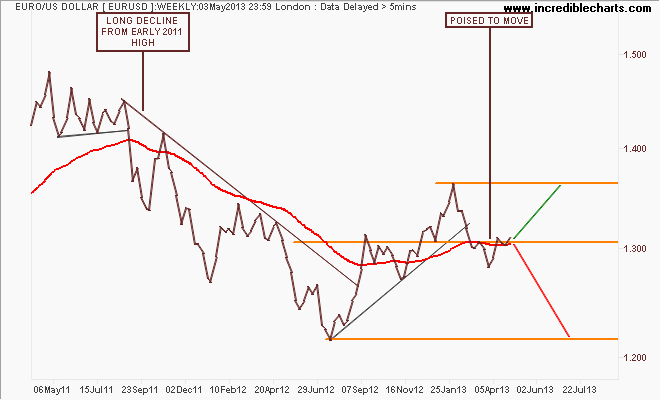

The first general opposite of the DXY is the euro (EUR/USD). After its break of the year plus down trend in August last year, which was followed by a blowoff as it tried to reach 1.37 on the back of QE3, the euro has retraced and consolidated at the key level of 1.30:

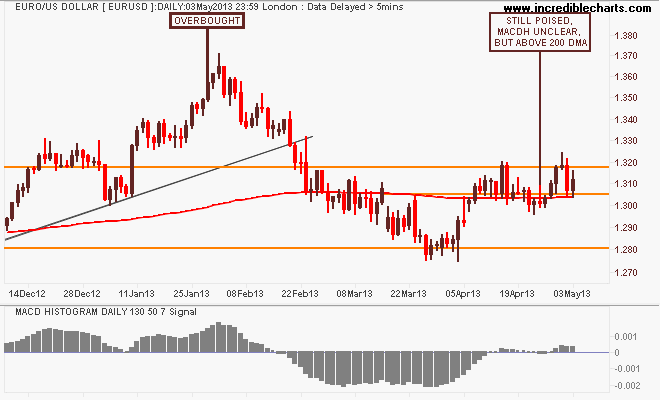

I would contend that failure to breakout above this key level could see the euro retrace back to support at 1.22, but given the DXY weakness and the general risk on mood an equally likely scenario is a rise up to the former blowoff level at 1.37; as seen on the daily charts, the MACDH indicator is unclear, but daily prices remain ABOVE the 200 day moving average:

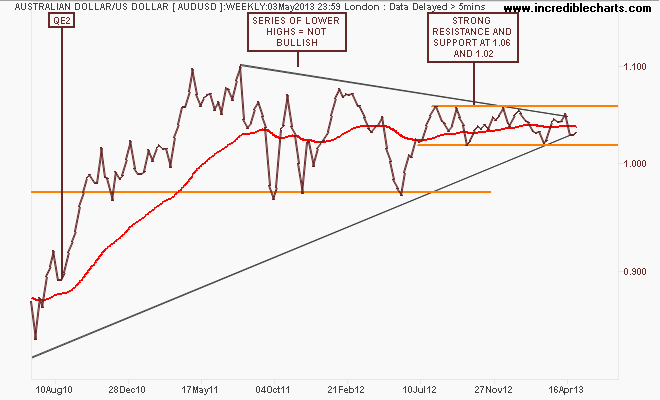

Given the Aussie “battler” (AUDUSD) is the premier commodity proxy, the question remains as the Federal Budget blows out – but more importantly, general commodity price weakens remains entrenched, why hasn’t it fallen further?

Probably still more safe harbour buying even as the RBA remains in a clear easing cycle. The weekly chart remains a fascinating picture, giving an insight into how this is playing out. The key takeaway in the medium term is that clear, strong channel between support and resistance at 1.02 and 1.06 respectively since mid 2012 remains intact. Lots of option strategies on the table here to consider……

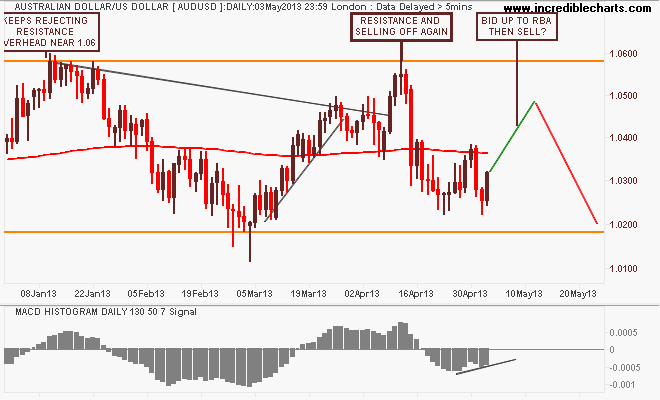

The shorter term picture is equally fascinating, with strong bids in recent weeks keeping the AUD off the floor between 1.02 and 1.03 – finishing with a strong bid on Friday night. Now, moving into the RBA meeting next Tuesday on the back of a commodity rally and risk on mood, the risk is growing of a whipsaw up through 1.04 and then a selloff if the RBA cuts rates.

Or the market ignores the battler and bids it up through 1.05 as the dance fires up in risk:

I’ll finish the currency section with the undollar currency of the moment, gold (USD).

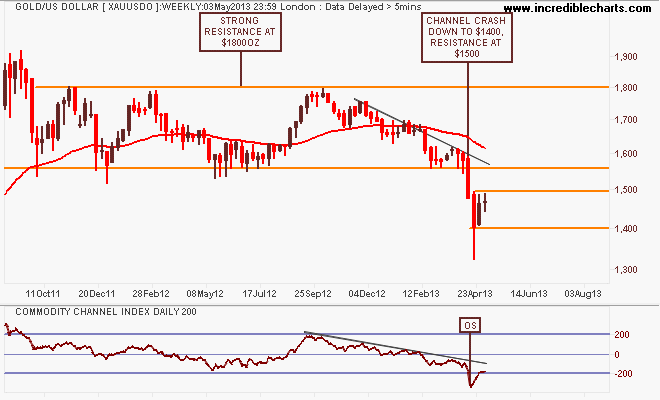

Three weeks after crashing through support (I don’t care how this happened, conspriacies et al, it happened, I shorted, I walked away) gold’s inevitable rebound is losing momentum as it struggles to push past $1500 per ounce – notice the 200 day CCI is barely above the normal oversold level:

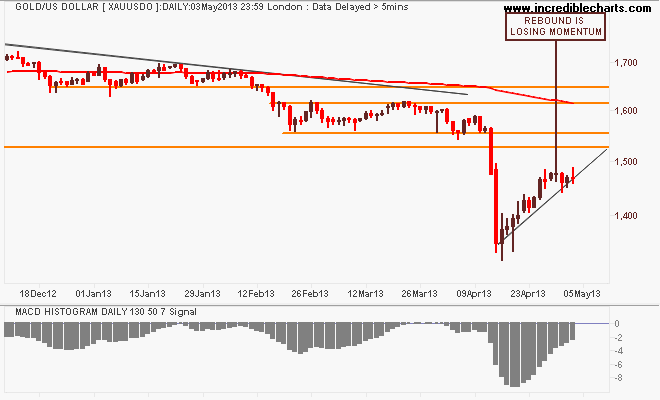

You can see this loss of momentum on the daily chart clearer, and while this doesn’t spell more doom for the shiny metal – a weaker dollar as posited above will only help, as will near-panic physical gold buying – this remains a swing trade alone IMO – everything remains too bearish right now. Having said that, I’m still long on the swing, but tightening my stops daily:

Equity Markets

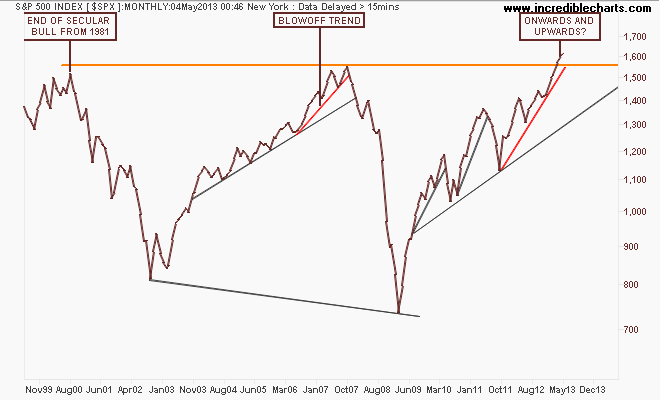

Before I get to the Aussie market, let’s look at the US S&P500 starting with the monthly chart showing a probable end to the US secular bear market, going on 13 years from the tech bubble high in 2000:

Note how the index before the GFC almost broke that high after a blowoff trend (marked in red) that accelerated in 2006 from the main trend. Note also that this pattern has been repeated – albeit with a lot more volatility and acceleration due to continued bouts of QE – with an accelerated uptrend from the August 2011 low. Not the same, but very similar.

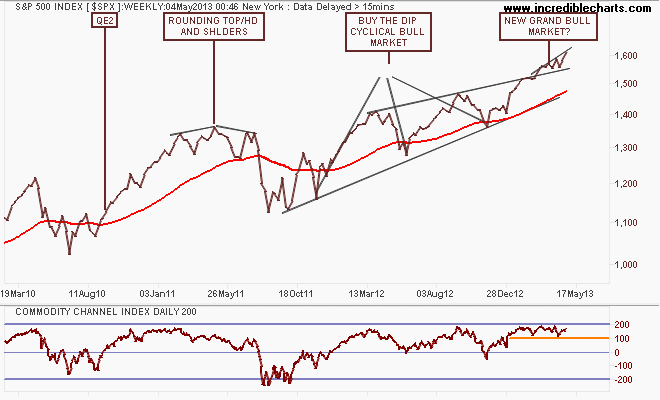

The weekly chart below shows this blowoff in greater detail, with a series of higher highs that is smaller on each up cycle. But the market remains on trend with the weekly price staying above the upper trend line, as reflected in its overbought status according to CCI:

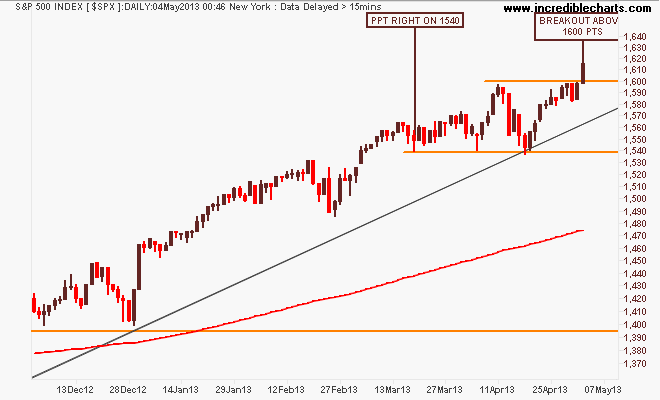

Looking at the short term point of view, note the key levels of support at 1540 points and resistance at 1600, with the latter clearly broken through on Friday’s session. Looks like “Sell in May” and go away will be a tougher decision this year: book massive profits or ride this liquidity led roller coaster up and up and…

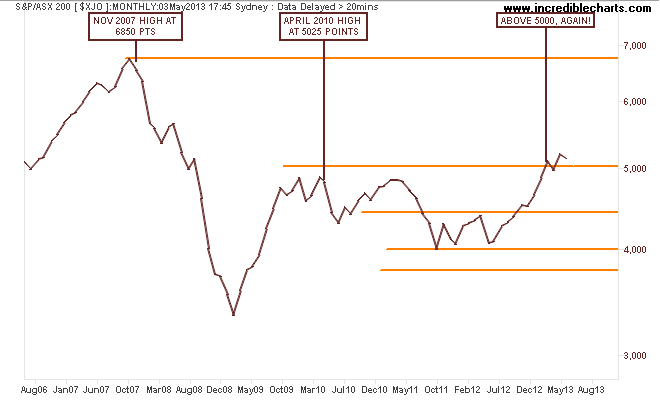

I contend that our own share market, the S&P/ASX200 index is only halfway through its own secular bear market – mainly on the back of the banking sector, which is completely dependent on an easing cycle in interest rates AND continued increases in national income AND access to wholesale credit markets at cheap prices. IMO, only one of the above is assured….

Note these important levels: the key levels at 3800-4000 (strong support), 4400 (intermediate resistance and the outer edge of the index’s real value), 4900-5000 (strong resistance, but now broken) and 6850 (the former high of the 2003-2007 bubble).

So on a long term view, it seems likely now that the key level of 5000 points will form strong support for further rallies or consolidation to come.

My medium term view remains that the recent rally has been unsustainable – and completely carried by the financials sector as the RBA eased rates to re-inflate the housing sector. That the materials sector has corrected sharply during this time as commodity prices came off the boil as Chinese authorities try to transition their economy continues to add to the risk of a correction and back to the trajectory from the first uptick in the August 2012 lows, around 4600-4700 points.

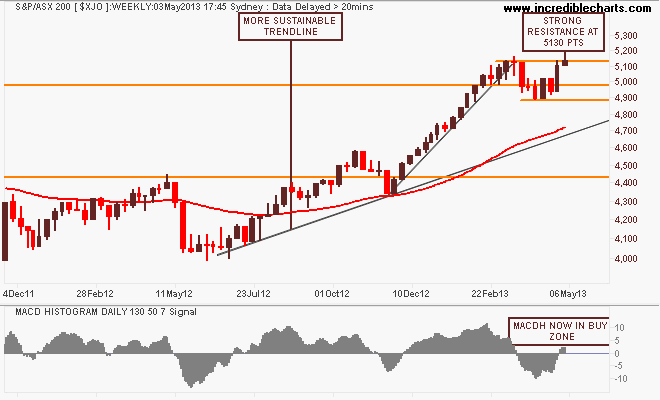

On the weekly chart, the market is finding resistance at 5130 points as it absorbs “Bank Week” that just passed (with some beautiful – if you’re a shareholder and not a taxpayer – financial results) and as the three main banks go ex-dividend in the coming weeks – although the MACD is in the buy zone:

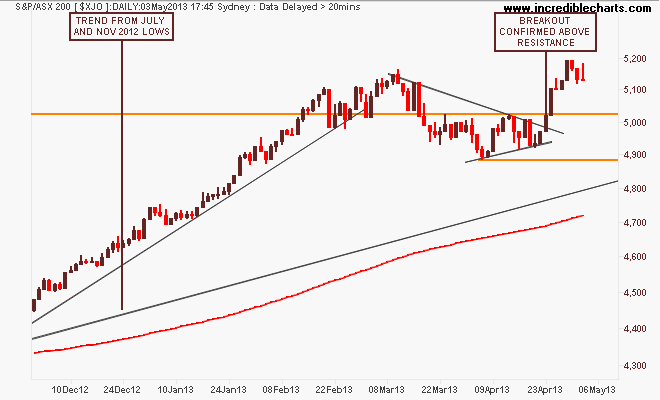

On the daily chart we can see the drawn out dip over March and April at the end of earnings season, but breaking to the upside again above 5000 points as the banks reported and risk turned back on, mainly because it seems more likely – on budgetary weakness reflecting broader economic (including corporate) weakness – that rates will continue to be slashed to keep asset prices high:

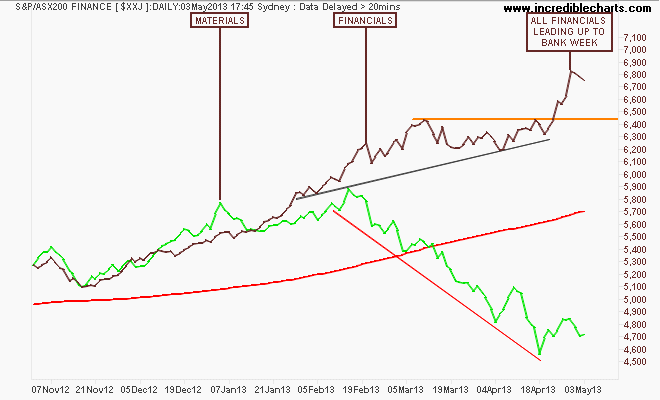

Here’s the financials annd materials (green) sector daily charts to put this bank led rally into perspective:

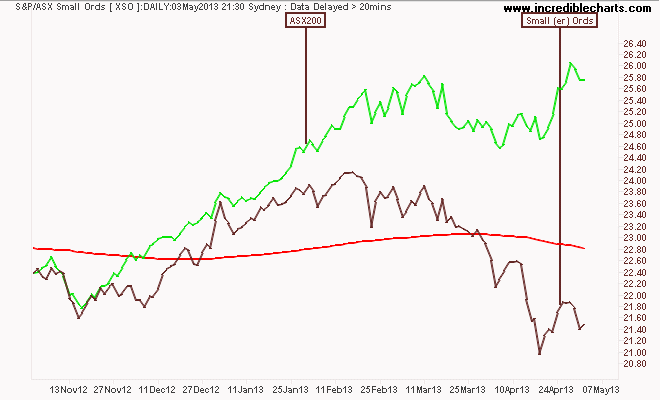

And the Small(er) Ords – the real backbone of the market – getting weaker and weaker:

Go Banks. Yay. Keep hollowing Australia!

That’s all for now, remember to manage your risk first and the returns will come thereafter. See you next week and stay safe.