The Reserve Bank of Australia’s (RBA) appears increasingly isolated in its rejection of the role of profits in driving inflation and obsession with wage costs.

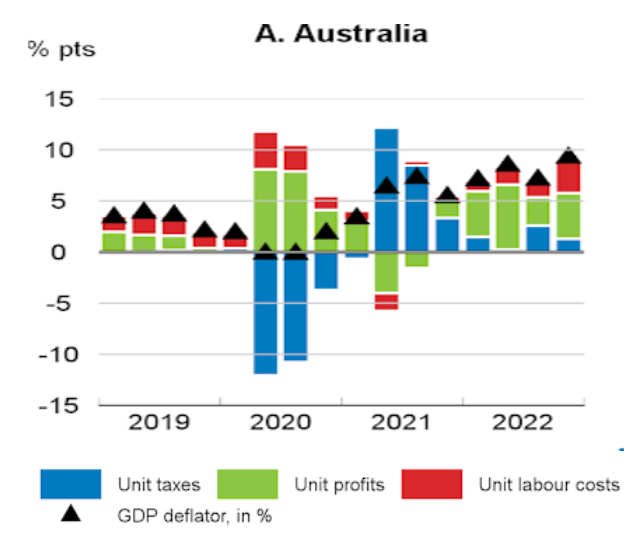

Earlier this month, the OECD released research showing that profits have played more than twice the role that wages have played in driving up Australian inflation over recent quarters:

“A significant part of the unit profits contribution has stemmed from profits in the energy and agriculture sectors, well above their share of the overall economy, but there have also been increases in profit contributions in manufacturing and services”, the OECD stated.

Source: OECD

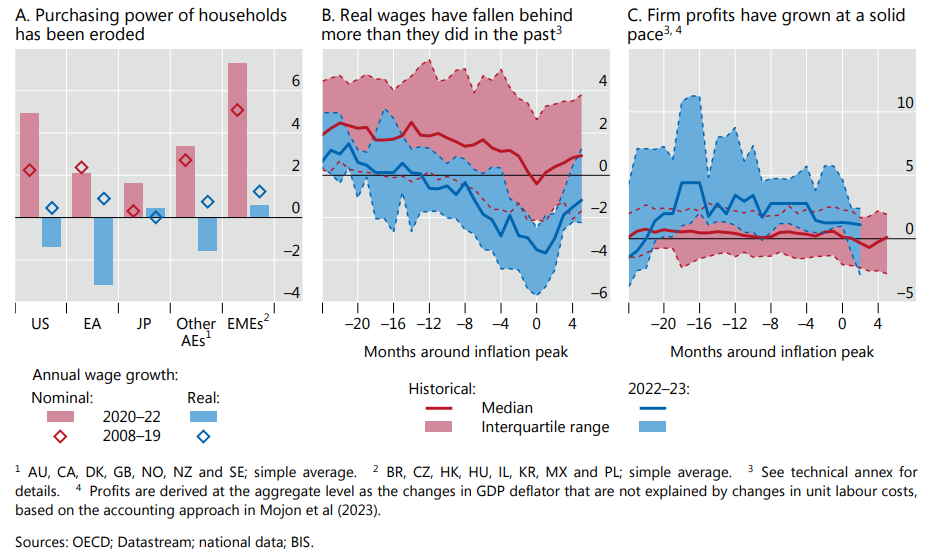

Now, the Bank for International Settlements (BIS) – the “central banks’ central bank” – has likewise found in its annual economic report that corporations have been using the cover of inflation to raise prices and boost profits.

The BIS also explicitly linked this behaviour by corporations to the absence of real wage growth experienced over the past decade:

“The inflation surge has severely eroded the purchasing power of households (Graph 14.A), even more than in past disinflation episodes (Graph 14.B)…”

“In parallel, there are signs that price-setting behaviour is changing. Firms are adjusting prices more frequently than when inflation was low and stable”.

“In addition, corporate profits, which were already on the rise before the inflation surge, have held up remarkably well so far (Graph 14.C). This is a departure from the historical pattern: in past episodes, profit growth tended to fluctuate within a comparatively narrow range around zero”.

“One concern is that, having been able to raise prices more easily than in the low-inflation regime, firms are now more reluctant to accept profit squeezes and will pass on cost pressures to prices more readily”.

BIS also explains how real wages could catch-up without fueling inflation, but only if corporations accepted a shrinkage of profit margins:

“A stylised exercise based on a decomposition of changes in the GDP deflator during disinflations shows that some catch-up in wages would be compatible with inflation returning to target, but only as long as firms accept a reduction in profits”.

“Back-of-the-envelope calculations suggest that, for inflation to go back to a target of 2%, profits on average would need to decline by about 2.5% per year in 2023–24, should real wages rise fast enough to make up for the loss in purchasing power and return to the pre-inflation surge level by end-2025.

“For comparison, the cross-country pre-pandemic median for profit growth has been slightly more than 1.5% between 2014 and 2019”.

So basically, it is price gouging by corporations that is driving inflation, not the wage claims by workers.

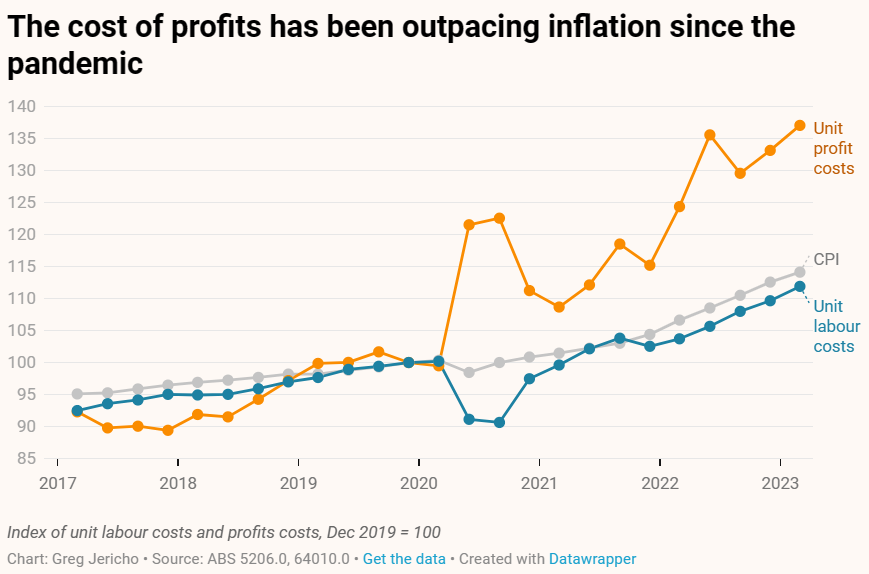

The below chart from Greg Jericho highlights the point with respect to Australia:

It is time for the RBA, Treasury, and business media to be honest about the issue, to stop blaming workers, and to direct their rage at the corporations that are fueling Australia’s inflation.