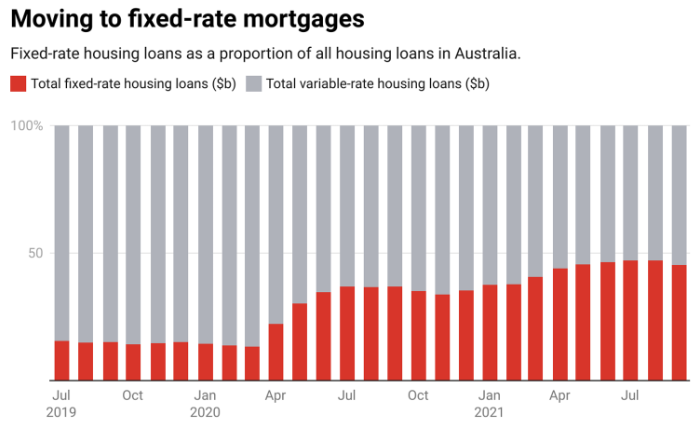

At the height of the pandemic, around 40% of Australian mortgages were originated at fixed rates:

Fixed rate mortgage lending boomed over the pandemic.

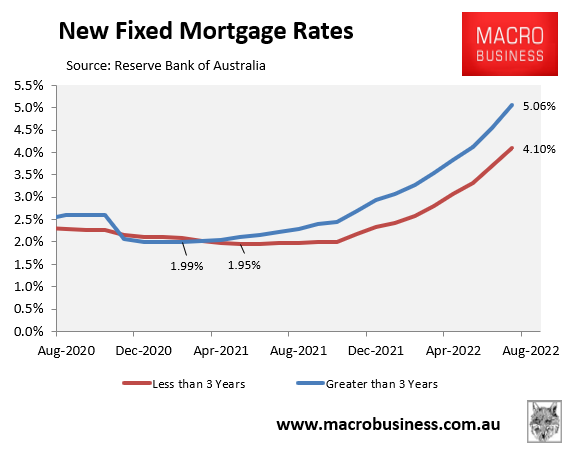

It is easy to see why, given fixed mortgage rates plummeted to below 2%:

Fixed mortgage rates have more than doubled.

Advertisement

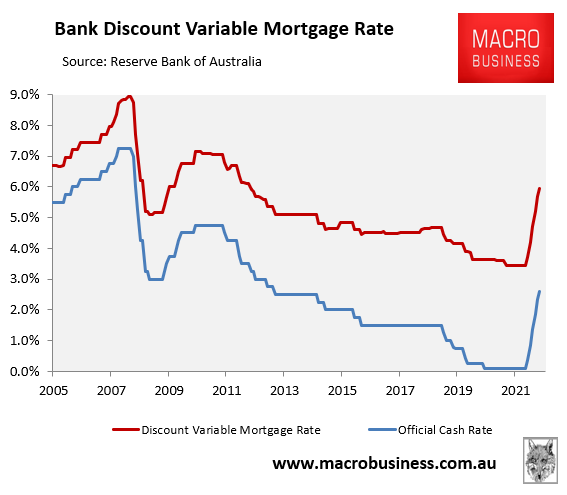

Since then, fixed mortgage rates have more than doubled, whereas the average discount variable mortgage rate has soared to its highest level in a decade at 5.95%:

Discount variable mortgage rate at decade high.

Yesterday, Australian Prudential Regulatory Authority (APRA) chief, Wayne Byres, warned that borrowers who took advantage of ultra-low fixed rates during COVID-19 now face a “significant repayment shock” when rates reset over the coming year:

Advertisement

“There will be people who took advantage of the very low fixed rates on offer in 2020 in the midst of the pandemic – many of those were two- and three-year fixed rate loans that over the next 12 months will need to be refinanced – and for those people, there will be a significant repayment shock as they have to refinance the fixed rates to higher rates,” he told the House of Representatives economics committee.

“The gradual increase in interest rates that variable rates borrowers have experienced will come in one hit to those fixed rate borrowers.”

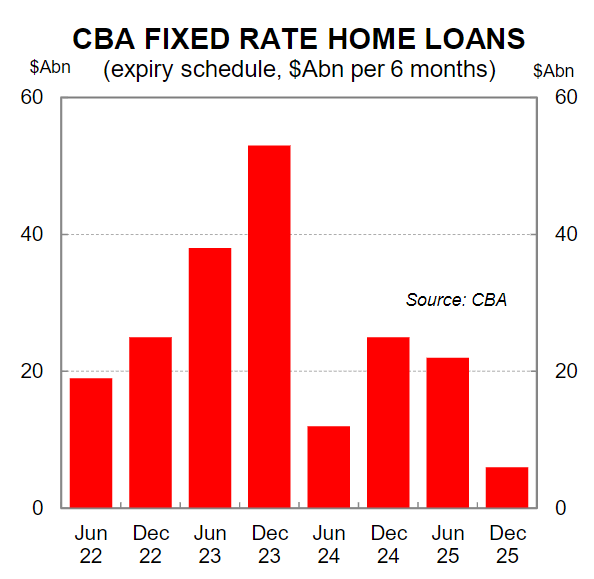

CBA head of Australian economics, Gareth Aird, made similar warnings in February, estimating that $500 billion worth of fixed rate mortgages will refinance at higher rates over the next two years:

The fixed rate home loan expiry schedule means that over the next two years a very significant proportion of home loans will expire (see chart below for the CBA fixed rate loan book expiry profile). Based on CBA’s fixed rate home loan expiry schedule and share of the market there is likely to be around $A500bn of fixed rate mortgage loans expiring in Australia over the next two years.

Advertisement

Steve Mickenbecker from financial comparison site Canstar also estimated that around 500,000 fixed rate mortgages will expire over the next 18 months:

According to Mickenbecker, the collection of borrowers that is smack in the middle of this bubble going through the banking system were those who signed on between April 2020 and November last year: on his estimates, that is at least 500,000 mortgages…

Mickenbecker… says the issue will emerge in an entirely predictably fashion three years after the fixed rate boom took off (in June 2020), which works out at midyear next year. It will reach at peak in August 2024.

So that’s around half a million borrowers facing a doubling or more in loan interest rate overnight as they reach the end of their fixed-rate period. Many will be pushed into severe financial stress, which will weigh heavily on consumption spending.

Advertisement

The fixed rate mortgage reset is also a reason why the RBA needs to tread carefully on raising interest rates. Because monetary conditions will tighten even without further rate hikes from the RBA.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.