The USD was whacked Friday night after more Trump jawboning and despite good jobs:

Commodity currencies rebounded:

Gold held on:

Brent fell again:

Base metals lifted:

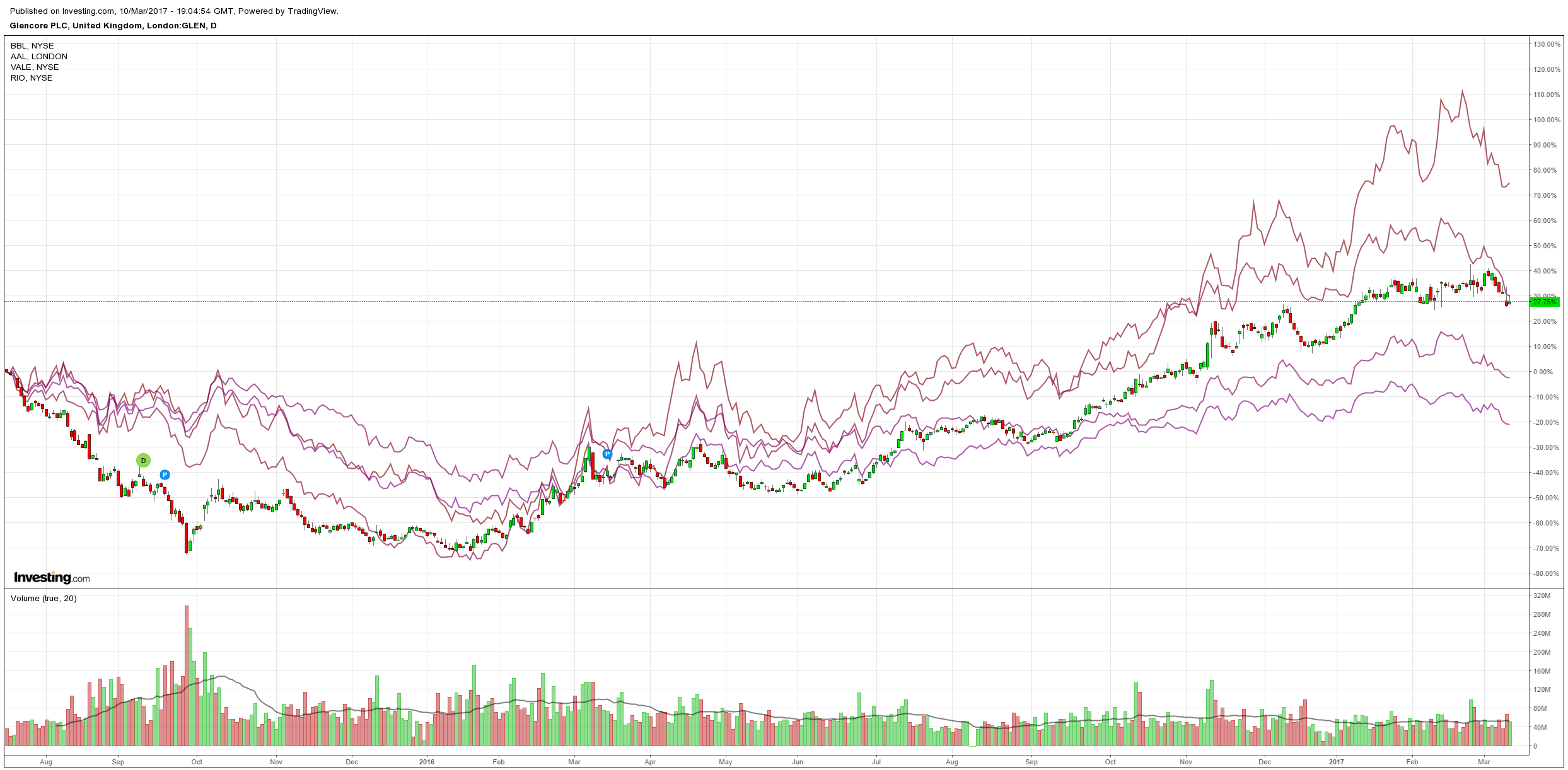

Big miners fell anyway:

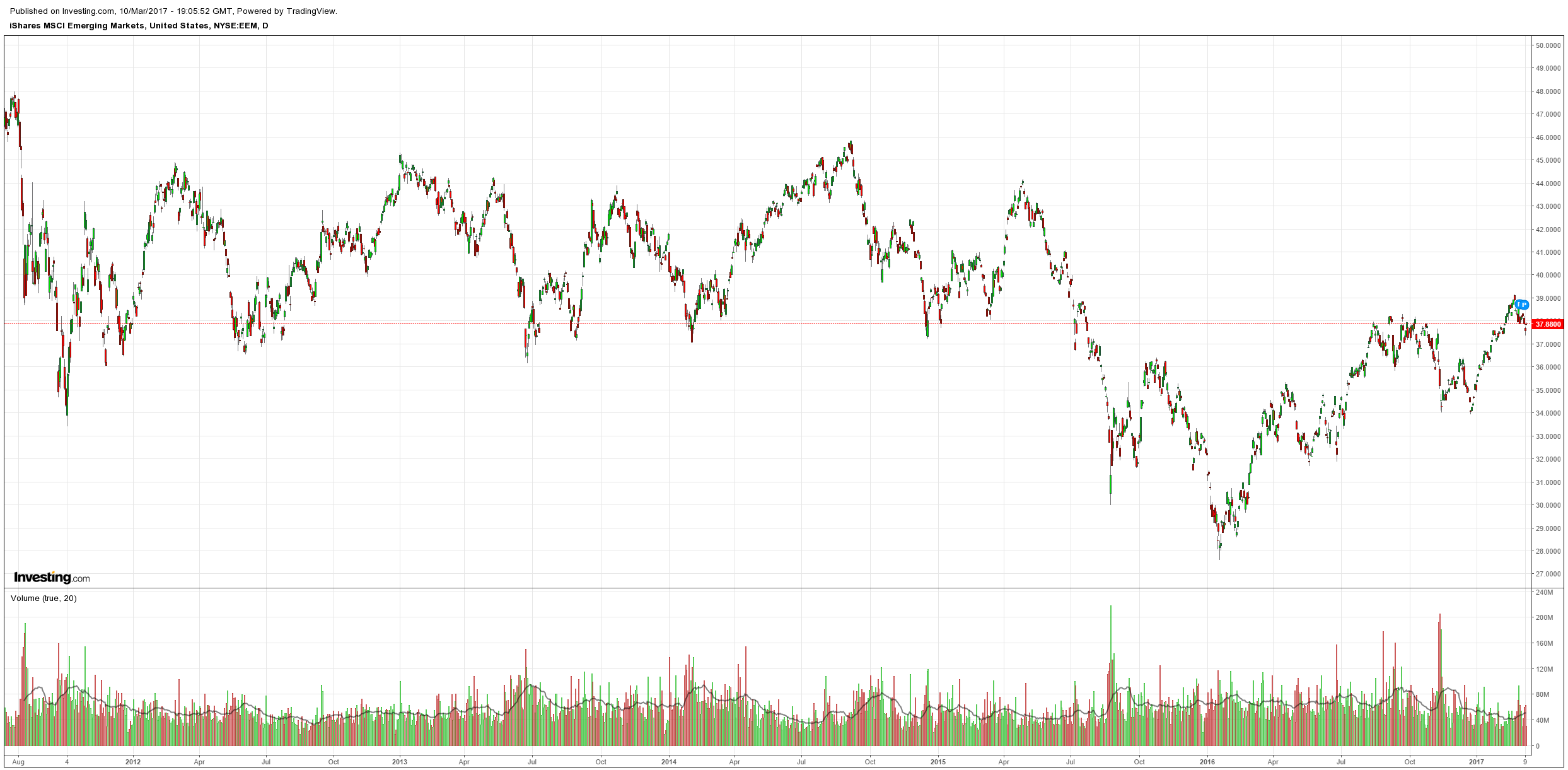

EM stocks rebounded:

High yield didn’t, following oil:

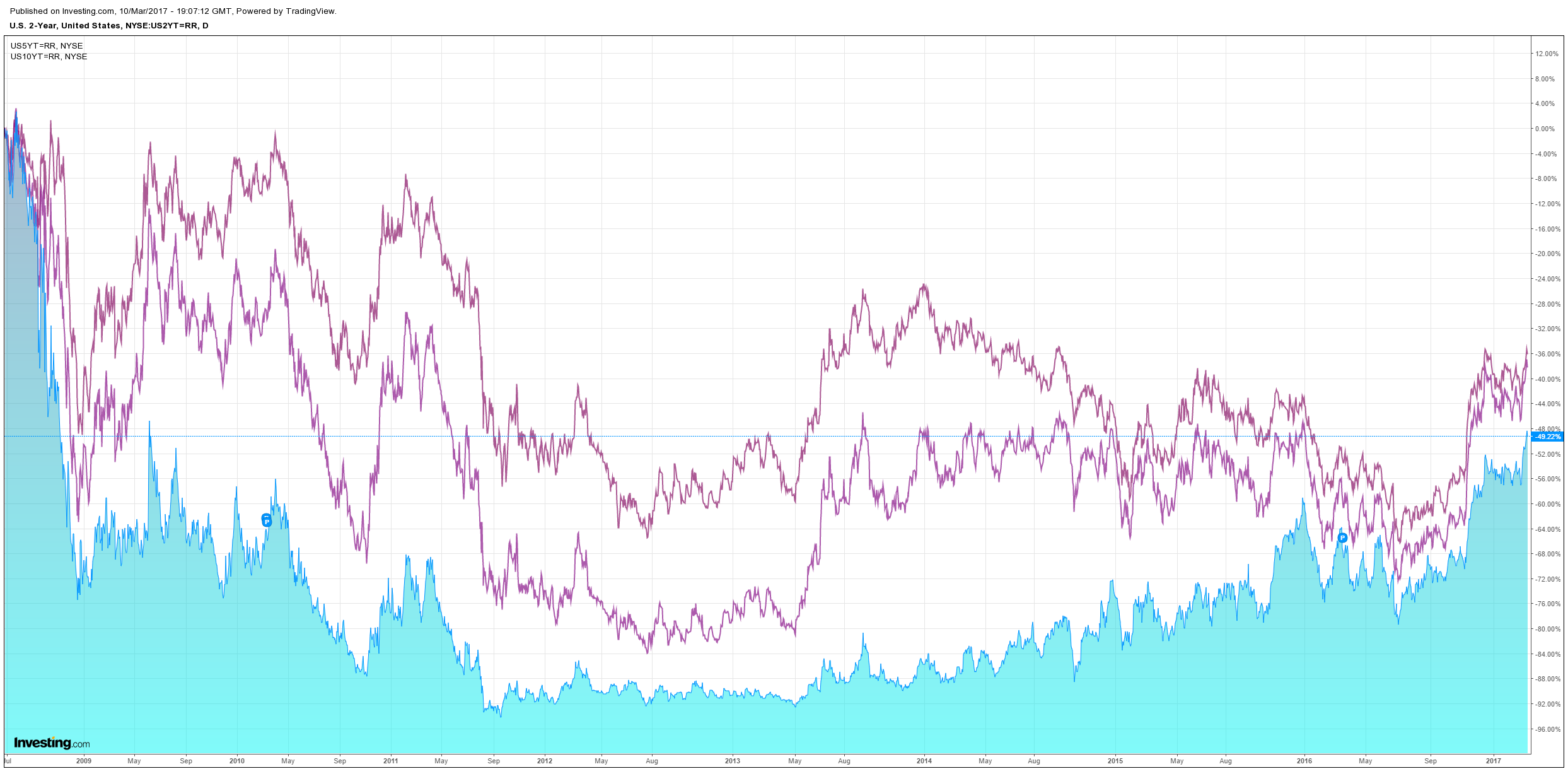

US bonds were bid:

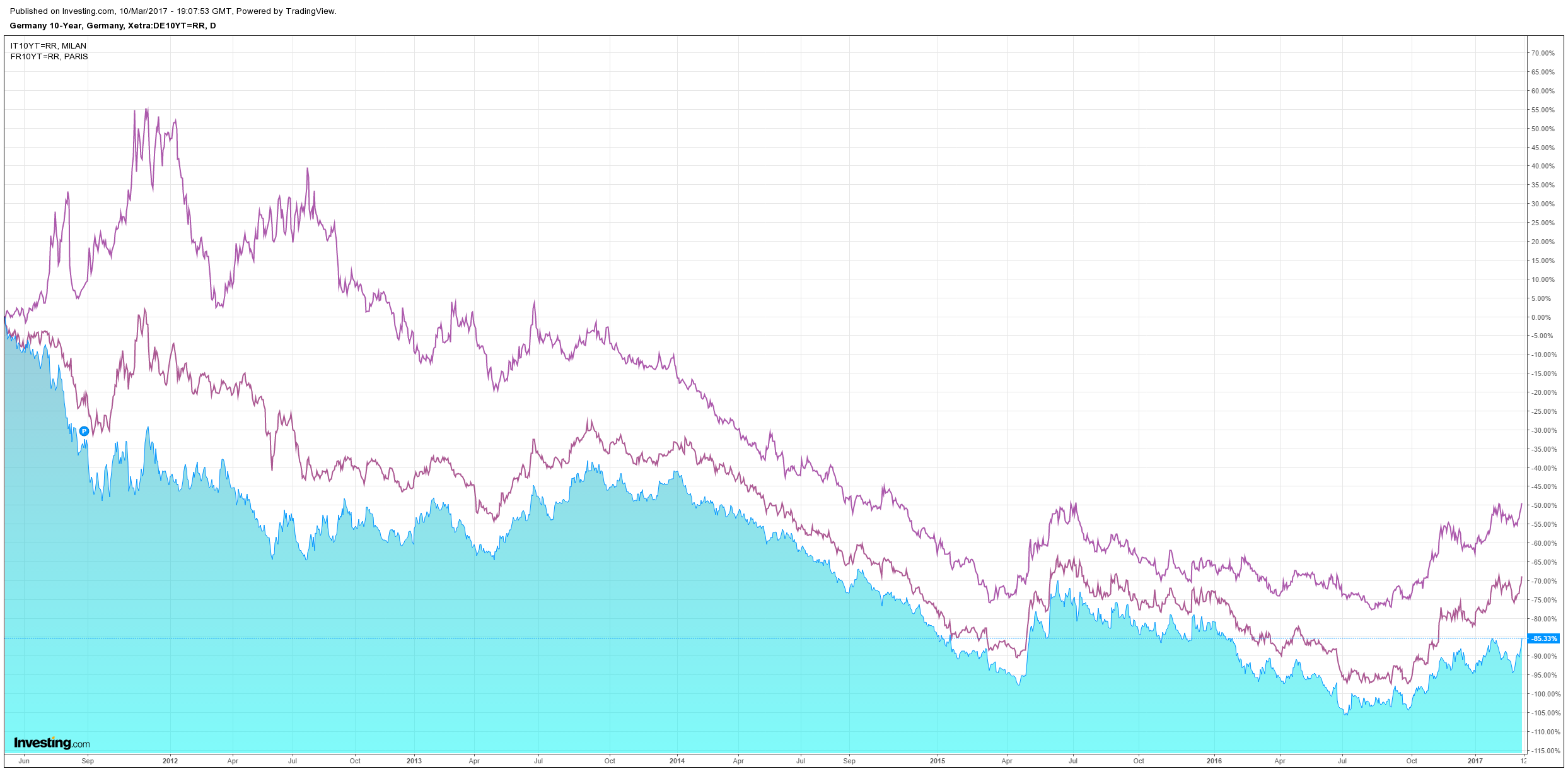

European spreads roared:

And stocks ended flat:

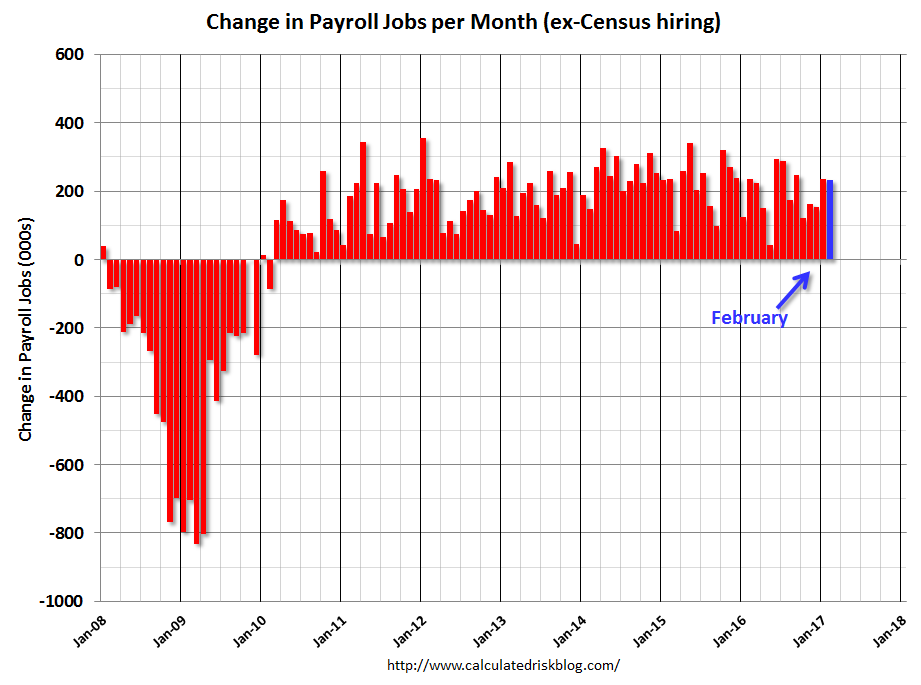

US jobs were good:

Total nonfarm payroll employment increased by 235,000 in February, and the unemployment rate was little changed at 4.7 percent, the U.S. Bureau of Labor Statistics reported today. Employment gains occurred in construction, private educational services, manufacturing, health care, and mining.

…The change in total nonfarm payroll employment for December was revised down from +157,000 to +155,000, and the change for January was revised up from +227,000 to +238,000. With these revisions, employment gains in December and January combined were 9,000 more than previously reported.

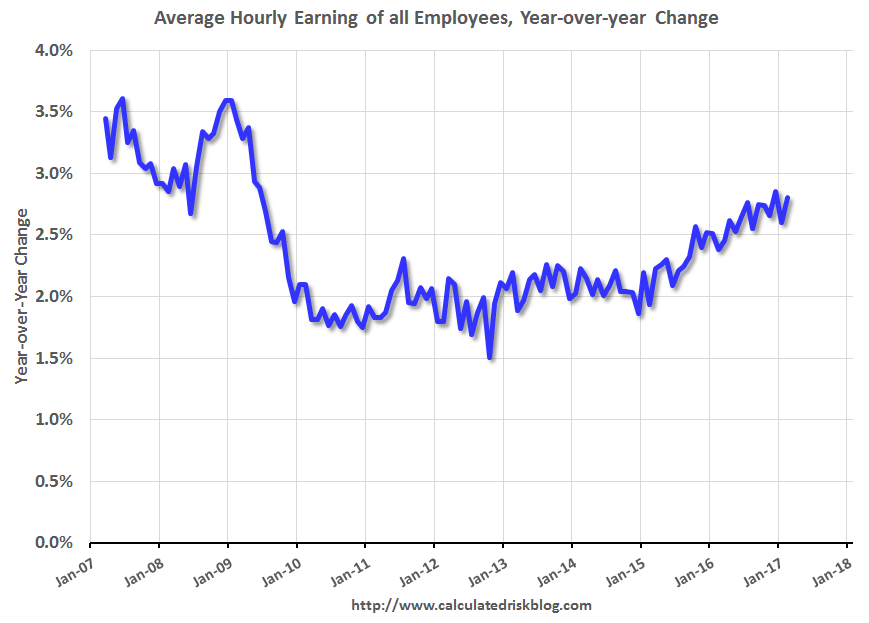

…In February, average hourly earnings for all employees on private nonfarm payrolls increased by 6 cents to $26.09, following a 5-cent increase in January. Over the year, average hourly earnings have risen by 71 cents, or 2.8 percent.

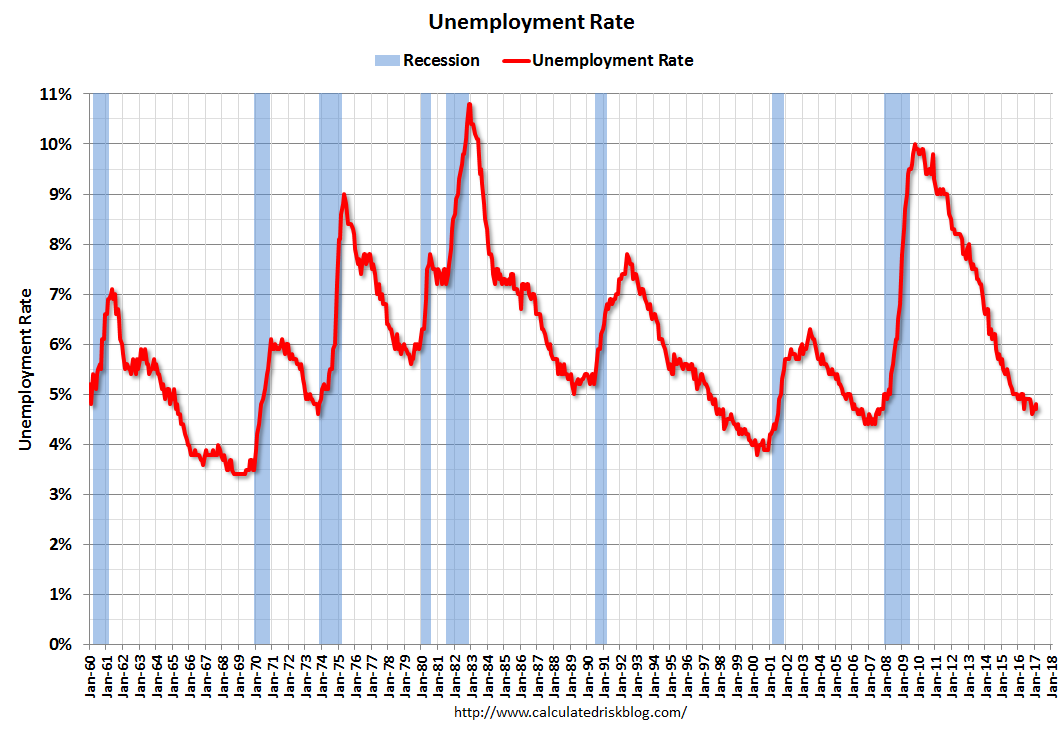

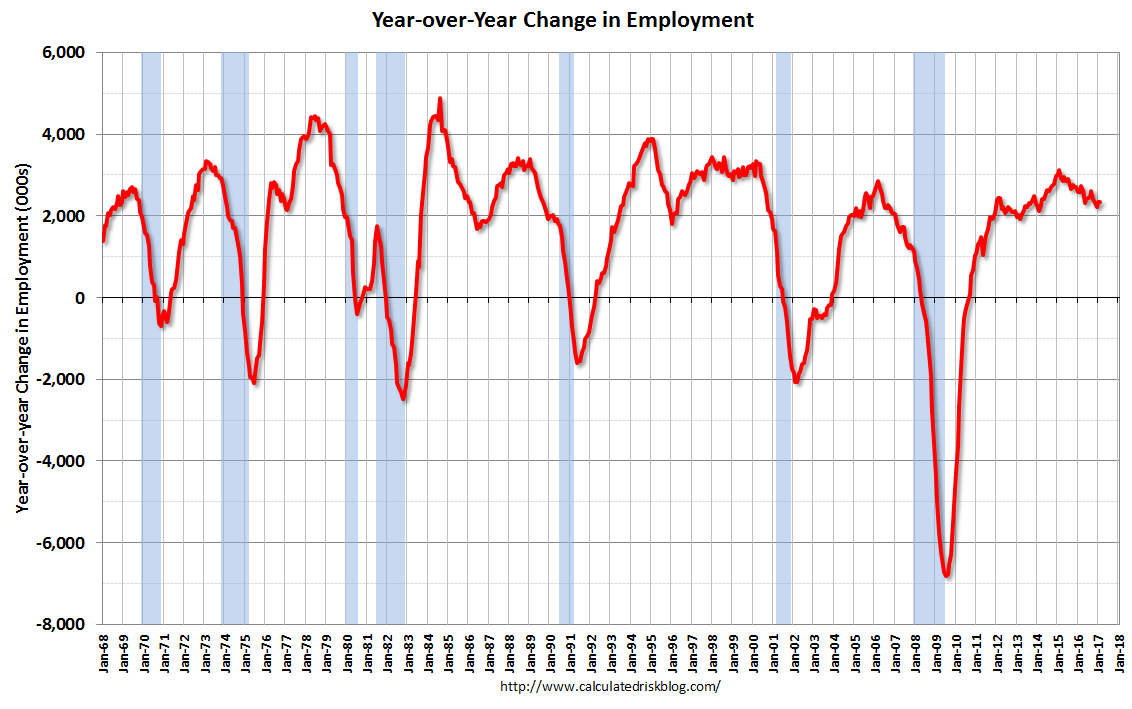

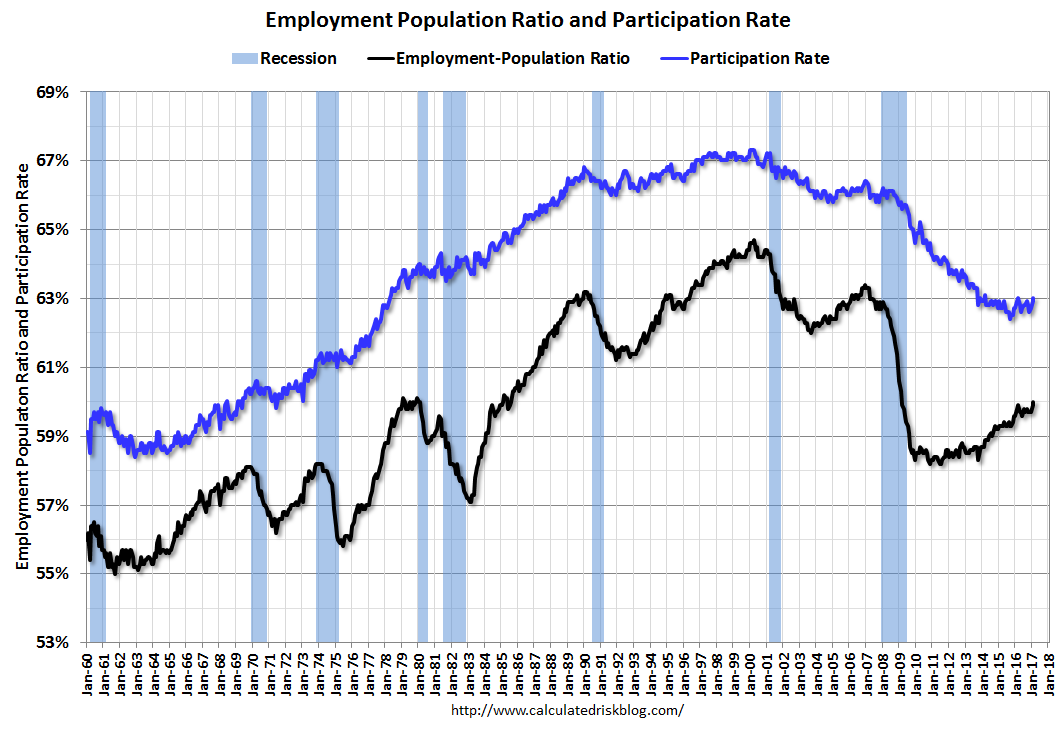

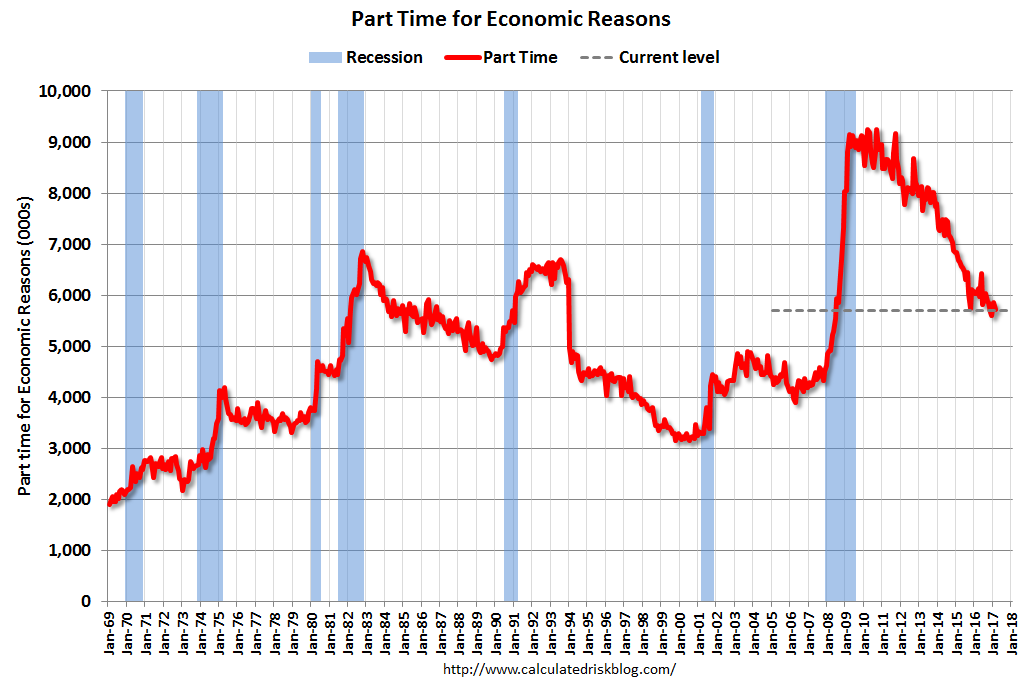

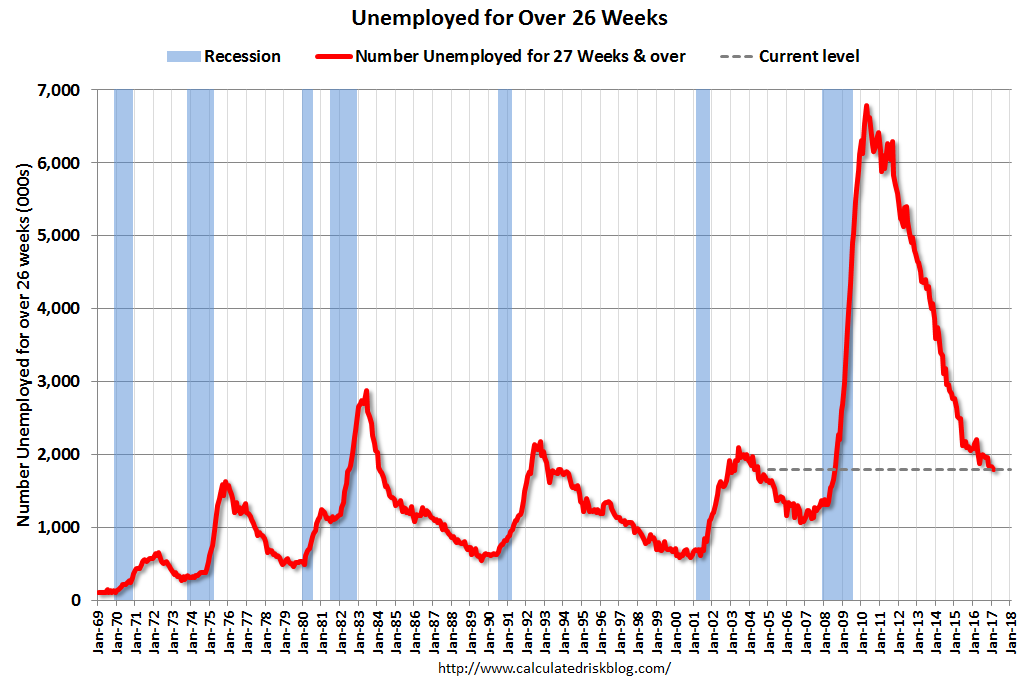

Charts from Calculated Risk:

Unemployment rate fell:

Growth is stabilising:

Analytical series improving:

Plenty of slack still:

Wages slowly improving:

Goldilocks stuff, this. Good jobs and muted inflationary pressures. Goldman brought forward its rate hikes:

BOTTOM LINE: Following the better-than-expected February employment report we have made a few modest changes to our Fed call for 2017. We now look for funds rate increases in March, June, and September (compared to March, September, and December previously), and have pulled forward our forecast for the start of balance sheet normalization to Q4 2017 from mid-2018 previously.

MAIN POINTS:

Nonfarm payroll employment increased by 235k in February, more than expected by consensus forecasts, and the underlying details of the report generally looked solid. As a result of the strong jobs numbers, benign financial conditions, and recent communication from FOMC participants, we are making a few modest changes to our Fed call for this year. Specifically, while we continue to expect three rate increases in 2017, we now look for a March hike to be followed by rate increases in June and September (versus September and December previously). In addition, we have changed our forecast for the start of balance sheet normalization: we now expect the committee to end full portfolio reinvestment in Q4 2017, instead of mid-2018. Under our forecasts for the US economy, we see it as a close call as to whether the FOMC would raise the funds rate four times this year or hike three times and begin balance sheet normalization. But for a variety of reasons—including considerations around the transition to a new Fed Chair in 2018—we see earlier balance sheet normalization as slightly more likely than a fourth funds rate increase.

I’ll stick with two but the report was good so there are upside risks.

The USD would have been strong on this but two Bloomie stories sent it the other way:

Specific language on countering trade barriers that may also be a focus for haggling in Baden-Baden. The G-20’s last communique, from the meeting in Chengdu, China, in July, commits members to resisting “all forms of protectionism,” wording that the U.S. now appears set on removing. The Trump administration’s protectionist stance, plans to renegotiate trade pacts like Nafta, and the possible implementation of a border tax would make it next to impossible for Mnuchin to sign up to that line.

An early draft communique, dated March 1, omitted that pledge, even though the hosts, Germany, and most other members continue to back it. Instead, the U.S. wants the insertion of a reference to “fair and equitable trade,” a reflection of the inward-looking trade policies that Trump backs, two people said.

If Mnuchin advances this argument further in Germany, he’ll find himself at odds with fellow Goldman Sachs alumnus Mario Draghi. The European Central Bank president on Thursday rejected the Trump administration charge that Germany is manipulating its currency — the euro, which is shares with 18 other countries — and defended the G-20 status quo. “It’s quite important that the G-20 reaffirms this commitment,” Draghi said at a press conference in Frankfurt. The consensus against protectionism and in favor of market-based exchange rates “have been pillars of world prosperity for many, many years,” he said.

And:

The euro and European bond yields surged on Friday after Bloomberg reported that the European Central Bank is said to have discussed whether they could raise interest rates before ending their program of monthly asset purchases.

The rise of the euro is certainly interesting and we’re preparing a European equities long to ride it if we get through the French election unscathed. However, it remains miles behind the US in its recovery with inflationary pressures that are purely imported, especially via commodity prices.

One should always remember the impossible trinity in these situations. Policymakers can control only two of the three variables of macro management: exchange rate, free capital movement and independent monetary policy. What that means in effect is that if the US talks down its currency it will raise domestic inflation, as well as interest rates and capital will pile into the currency anyway.

The same works in Europe in reverse. It can talk up interest rates but not without inflation falling from still very low levels. I can’t see the ECB moving in a hurry and when it does its progress will much slower than the Fed.

Policy does its best to cajole and coax but macro is the driver in the end.

And so allocations remain:

- buy the dips in the USD and S&P500;

- sell rallies in the AUD and commodities;

- buy dips in short end Aussie bonds;

- buy dips in gold for portfolio protection;

- sell property!