DXY fell again last night:

Commodity currencies did too:

Gold roared:

Ominously, Brent fell:

Base metals were mixed:

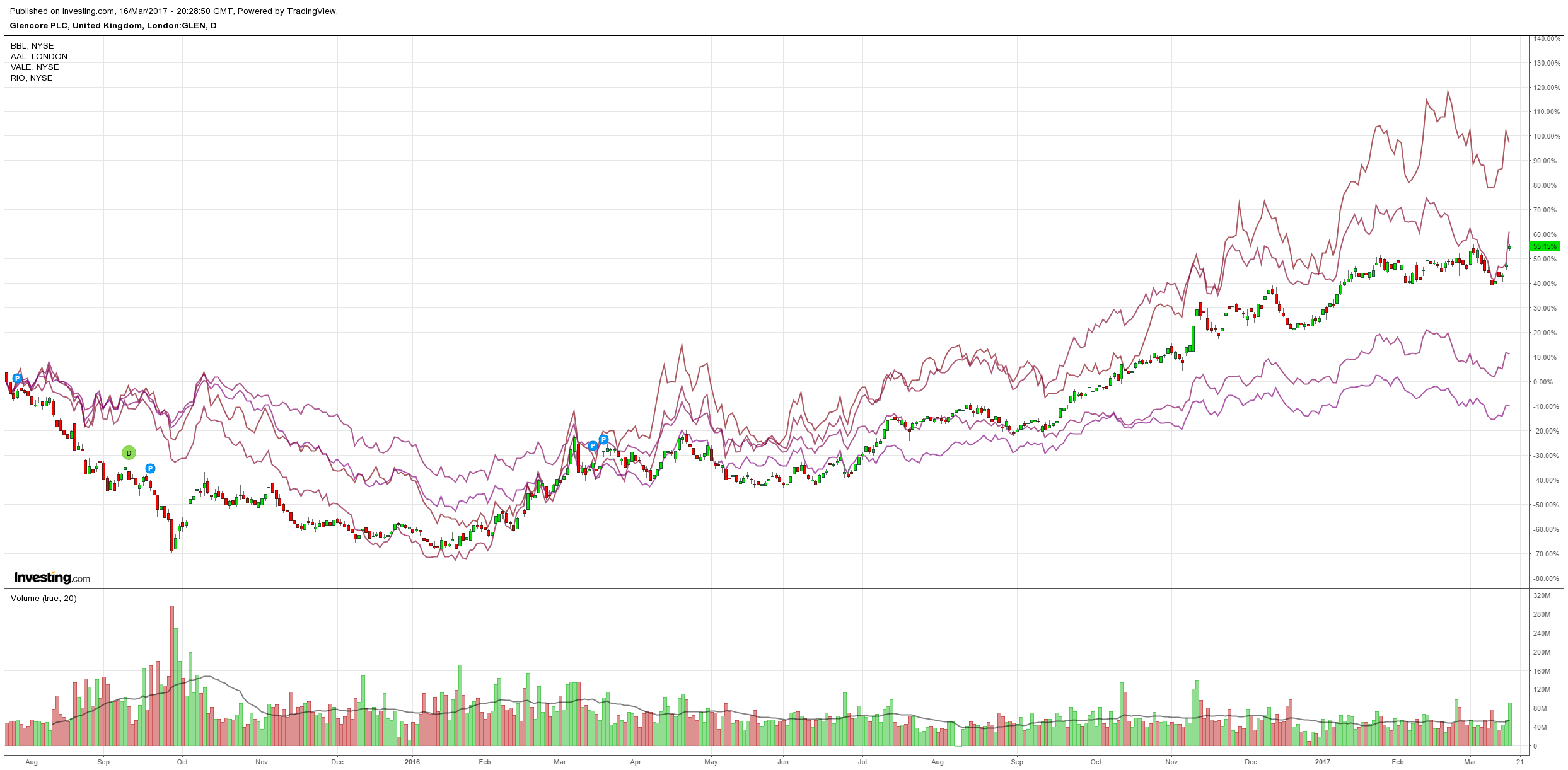

Big miners too:

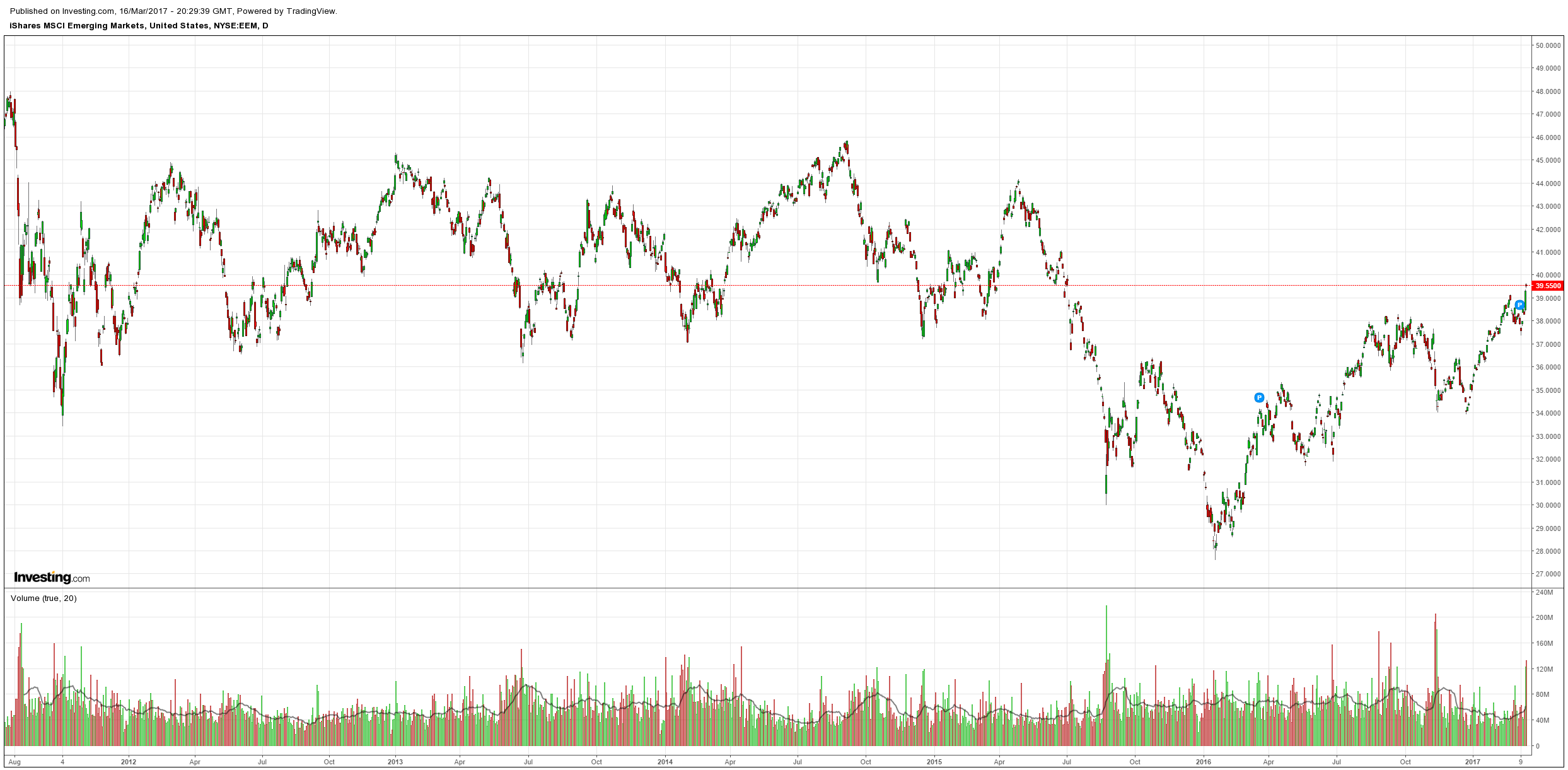

EM stocks roared:

But high yield is not impressed:

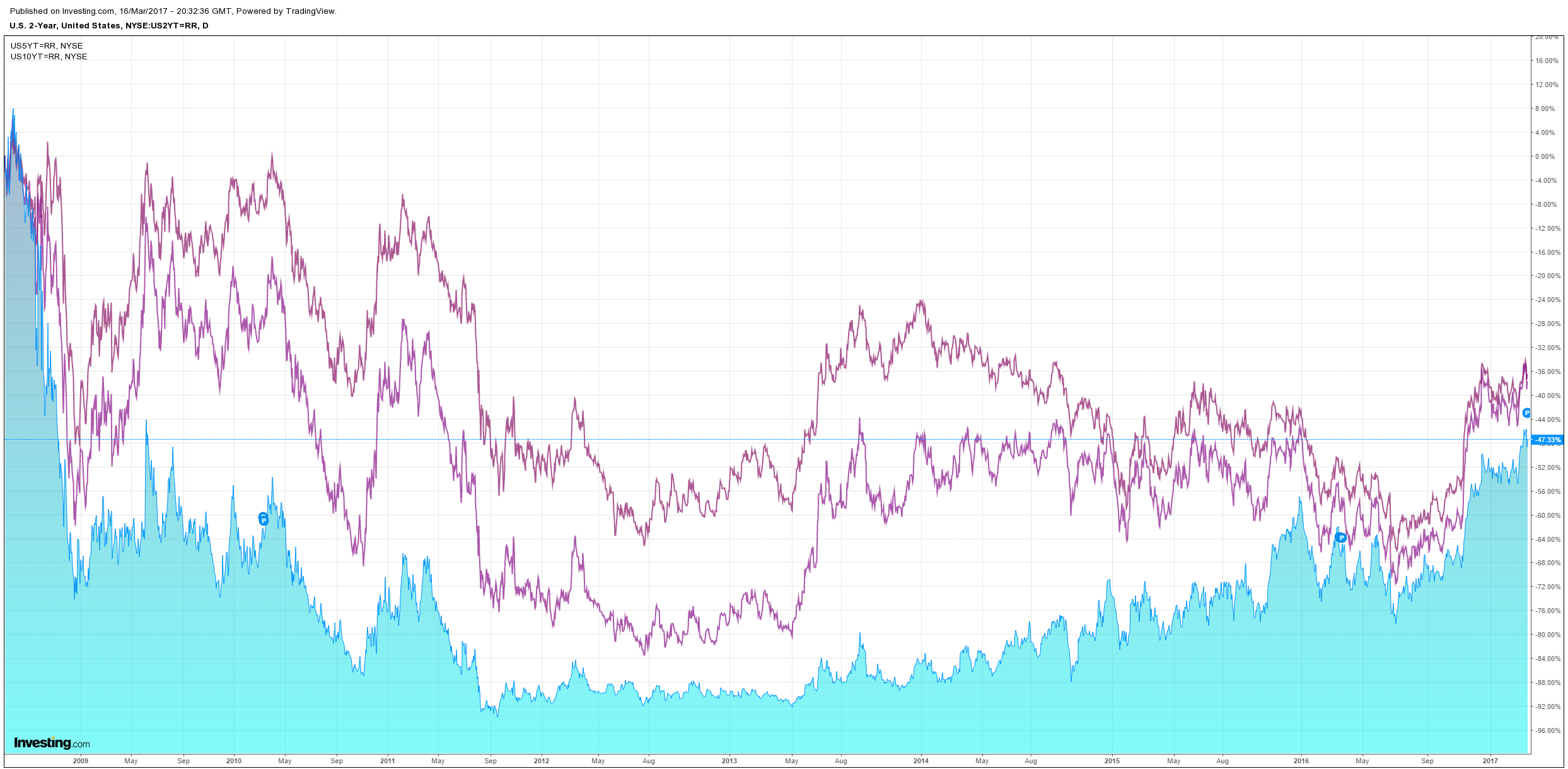

US bonds were sold a little:

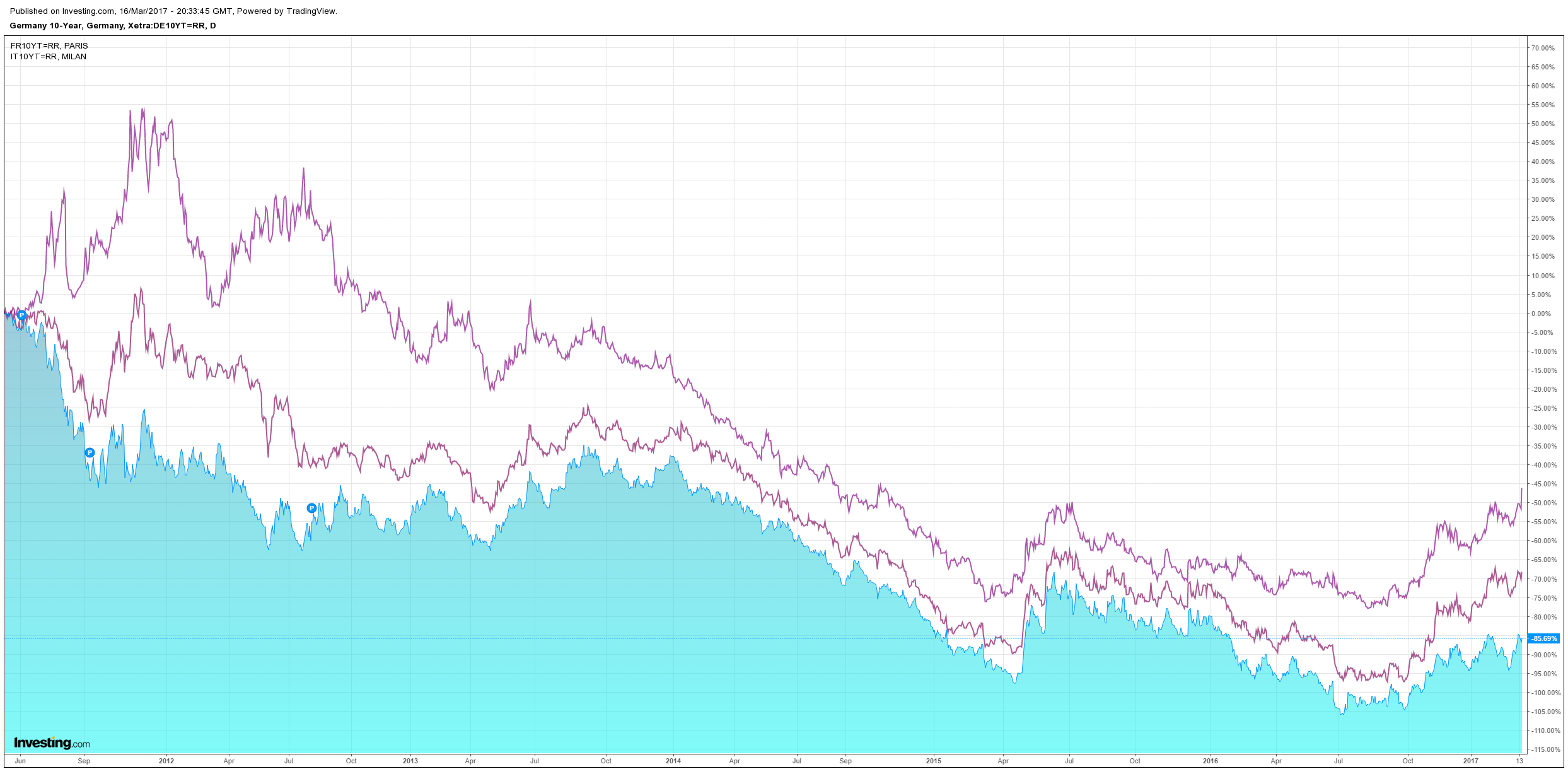

Most European spreads fell though Italy rocketed (I’m a bit suspicious that this accurate):

The S&P held on:

So, big news all around. Goldman says the Fed will tighten more quickly than ever owing to the market reaction:

Q: What surprised you at today’s FOMC meeting?

A: There were certainly a few dovish surprises, relative to both our expectations and our read of the consensus. First, none of the FOMC participants who projected three hikes or less for 2017 in December seems to have moved to four hikes or more; we expected two participants to move up, and some forecasters had even projected an increase in the median to four hikes. Second, the Fed’s estimate of the structural unemployment rate declined by a tenth to 4.7%; this coincides with our own estimate, but we didn’t expect the committee to make this move today. Third, we did not expect Minneapolis Fed President Kashkari to dissent in favor of unchanged rates, and we don’t think others did either. Fourth, the explicit statement that the inflation target is symmetric also came as a surprise, to us and likely others. And fifth, the statement was modified to say that the committee looks for a “sustained” return to 2% inflation.

Q: So was it a big dovish surprise overall?

A: It didn’t seem like it to us. First, the surprise in the dots, while real, seemed fairly small compared with past SEP meetings, with no changes in the median number of hikes in 2017 and 2018 or the median long-term funds rate. Second, the structural unemployment estimate moved only 0.1 point, has been trending down for several years, and is still above the committee’s forecast for the actual rate. Third, the predictive power of dissents from regional Fed presidents—especially dissents against a move that the committee is making, as opposed to dissents in favor of a move the committee has not yet made—is limited. Fourth, Fed officials have often noted that their inflation target is symmetric; moreover, the move seemed to be “defensive” in nature, as Chair Yellen noted in the press conference that it was designed to take the sting out of the recognition that there is no longer a sizable “current shortfall” in inflation. And fifth, the word “sustained” may have been equally defensive in nature, clarifying that a temporary rise in (headline) inflation to 2% or more is not, on its own, sufficient to meet the committee’s goal.

Moreover, there were also a few slight hawkish surprises. First, in the press conference, Chair Yellen declined the invitation to give much meaning to the word “gradual”; in fact, she noted that “…rates were raised at every meeting starting in mid-2004, and I think people thought that was a gradual pace, measured pace…” although she hastened to add that the committee is not envisaging “anything like that.” Second, the median pace of hikes in 2019 rose to 3½ from 3. These are minor, but they illustrate that not all the news was dovish.

Q: So what do you make of today’s market response?

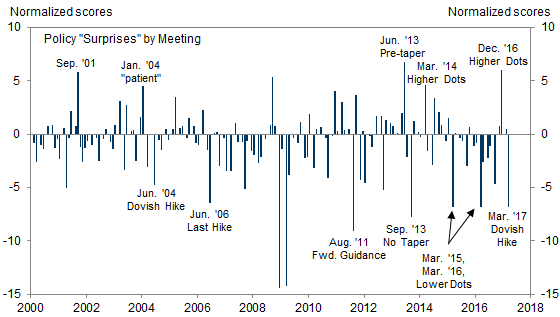

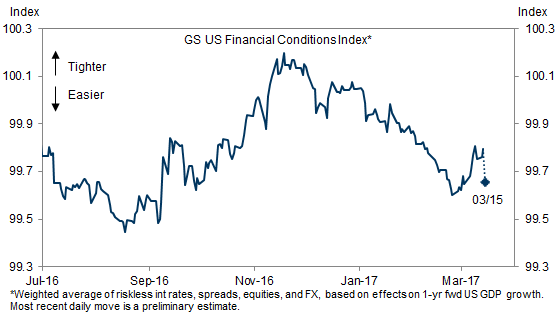

A: The direction makes sense, but the magnitude greatly surprised us. As shown in Exhibit 1, our factor model for discerning monetary policy surprises from the co-movement of different asset prices scored today’s price action as the third-biggest dovish surprise at an FOMC meeting since 2000, at least outside the financial crisis. (The only two non-crisis meetings that were clearly bigger were the August 2011 move to calendar guidance and the September 2013 decision not to taper QE; the March 2015 and March 2016 cuts in the dots were similar to today’s move.) And as shown in Exhibit 2, our FCI eased by an estimated 14bp on the day—about 2.3 standard deviations and the equivalent of almost one full cut in the funds rate—and is now considerably easier than in early December, despite two funds rate hikes in the meantime. Our interpretation is that markets must have been positioned for much more hawkish news than we had thought.

Exhibit 1: According to Our Factor Model, This Was a Large Dovish Surprise

Exhibit 2: Our FCI Has Reversed Most of the Recent Tightening

Q: Do you think the FOMC was aiming for this outcome?

A: No, almost certainly not. The committee may have worried that a rate hike—especially a rate hike that was not priced in the markets or predicted by most forecasters as recently as three weeks ago—might lead to a large adverse reaction on the day, and wanted to avoid such an outcome by erring slightly on the dovish side. But we feel quite confident that they were not aiming for a large easing in financial conditions. After all, the primary point of hiking rates is to tighten financial conditions, perhaps not suddenly but at least gradually over time. And even before today’s meeting, at least our own FCI was already fairly close to the easiest levels of the past two years and this was likely one reason why the committee decided to go for another hike just three months after the last one.

Q: How will the committee respond to this potentially undesired move?

A: At the margin, it will likely make them more inclined to tighten policy. Using today’s estimated close, our FCI impulse model now implies a boost of about ½pp to real GDP growth in 2017, from a starting point of roughly full employment and inflation close to the target. So further FCI easing implies at least some risk of economic overheating—which in turn would increase the risk of recession further down the road. We expect the committee to lean against such an easing over time.

Q: So what do you expect from the Fed for the rest of 2017?

A: Our modal forecast remains for a total of three hikes this year, with remaining moves at the meetings in June and September, followed by four hikes each in 2018 and 2019. We see a 60% subjective probability that the next hike occurs at the June 2017 meeting, 10% for July, and 20% for September. We also expect an announcement of gradual balance sheet rundown in December; if this does not occur, the likelihood of a fourth 2017 hike would increase. At the margin, today’s FCI move has increased our conviction that the committee will need to deliver more tightening than priced in the markets at this point.

I remain of the view that oil will head it off at the pass. The other big news was, of course, the Dutch election, via FT:

Prime Minister Mark Rutte looks certain to form the next Dutch government, with his party securing a clear general election victory over the far-right populist challenger Geert Wilders. Mr Rutte’s win was welcomed by moderates and pro-EU politicians across Europe and helped to calm fears that the continent was poised to fall under the sway of nationalists following the UK’s Brexit vote and the election of Donald Trump in the US. Angela Merkel, German chancellor, called the result “a good day for democracy” and added that she “was very happy that a high turnout led to a very pro-European result, a clear signal”. The result sent the euro to a five-week high of $1.0707, after the currency surged 1.2 per cent overnight, though by midday it had pared most of its gains.

…While Mr Wilders’ PVV has had a comfortable lead in polls for much of the past year, voters blanched at the prospect of backing the party at the ballot box. Although 20 seats was a small improvement on its performance in 2012, it would be four fewer than it gained in 2010.

That seems a fair assessment. French polls remain very solidly biased towards a similar rejection of anti-European sentiment. Thanks Donald!

We have begun a previously mooted rotation from US stocks to European. There are four reasons for it:

- US valuations are extreme, European are relatively much cheaper;

- the euro will get relief as these elections pass and none now threatens an existential spill. That will weigh on the USD at the margin;

- the AUD is still very high versus EUR.

- we are stock picking in Europe rather than aiming for a particular bourse. We do not expect anything much more than an ongoing modest economic recovery.

Don’t get me wrong, we remain long US stocks and bullish USD as well but the trade has been so profitable, so fast that all our valuation metrics are howling “take profits”. So we will act accordingly and begin a rotation to Europe with the proceeds.

So, allocations have changed today:

- buy the dips in S&P500 and the USD;

- buy the dips in selected European stocks;

- sell rallies in AUD and commodities;

- buy the dips in short end Aussie bonds;

- buy the dips in gold;

- sell property!