A number of trends are converging here: doubts about the timing of the US fiscal hand-off; policy convergence throwing up doubts about the USD rally; oil breaking down casting doubts on EM reflation and very overbought everything needing a technical pullback. From RBC:

THE CASE / DRIVERS BEHIND THIS DEVELOPING ‘USD SHORT’ TRADE:

The ‘USD short’ case is now tactically ‘en vogue’ as per the sudden-death of the central bank “policy divergence” story last week–which had been the primary Dollar bull-case driver over the past year. With central banks synchronizing their tightening messages (recall Fed hike, PBoC increasing 7-, 14- and 28- day rev repo rates and ECB hawkish commentary all in the same 24 hr period last week) the Dollar’s unilateral ascent has at the very least been paused, if not reset. There are a multitude of inputs here with the Dollar, seven of which I’ll highlight below:

–Overnight we saw a EU fixed-income selloff gaining-steam ‘real-time’ with Gilts to BOBL’s weaker across boards following 1) a stellar UK inflation print, in turn crushing the crowded Pound ‘short’ (SONIA curve pricing in 22bps of hikes by May ’18, up from 17bps prior to data—h/t RBC David Brickell).

–2) Now too that the Brexit “official announcement date” has been set, we also saw Pound shorts being covered driving further Dollar weakness.

–At the same time specifically with EU, 3) a strong showing by Macron in the French Presidential debate too helped drive OATs weaker and squeeze Euro notably-higher against the USD as well, with sentiment again higher as Le Pen political risk continues to be priced lower.

–4) Sprinkle-in the “smoke / fire” trial-balloon from ECB’s Nowotny last week on ‘hiking before tapering’ into a market overvalued on QE and ‘geopol uncertainty’ and things get combustible.

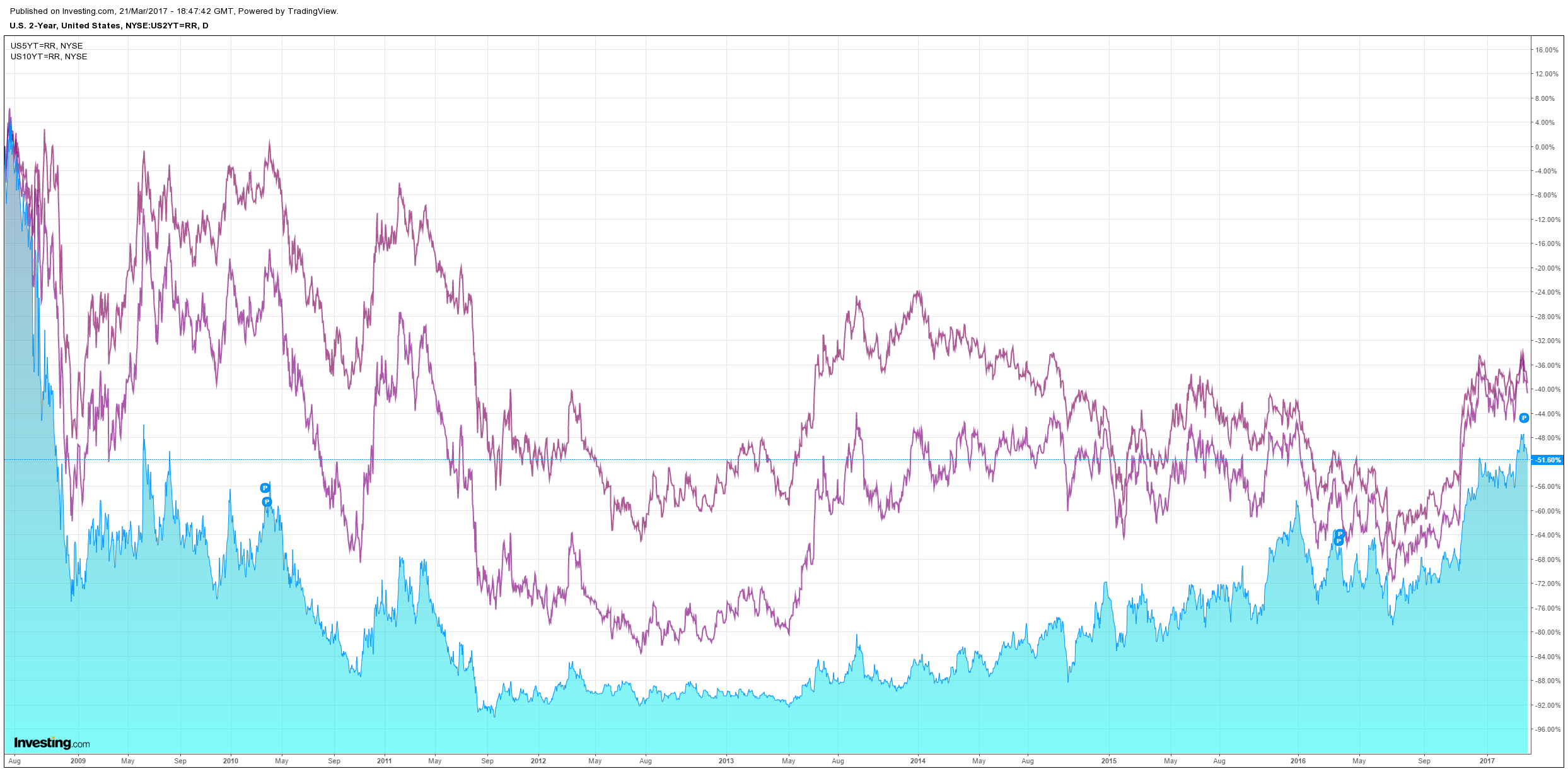

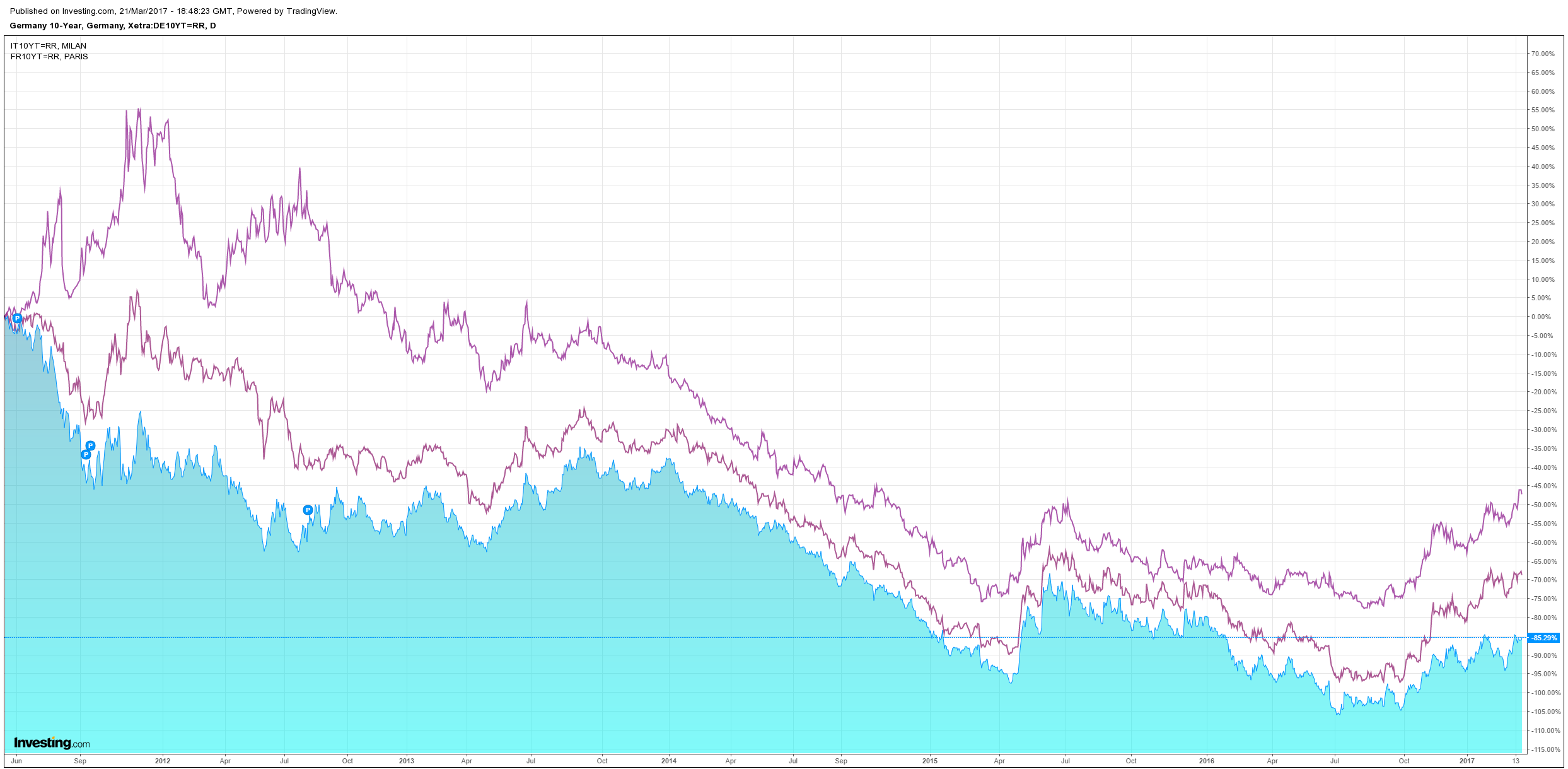

–As such, 5) US / EU rates differentials are reversing course and compressing from record wides made in late Dec ’16, with +++ EU data trajectory being the largest factor behind the move– in turn is leaning heavily on USD:

US / EU RATES DIFFERENTIAL COMPRESSION DRIVING US DOLLAR WEAKNESS:

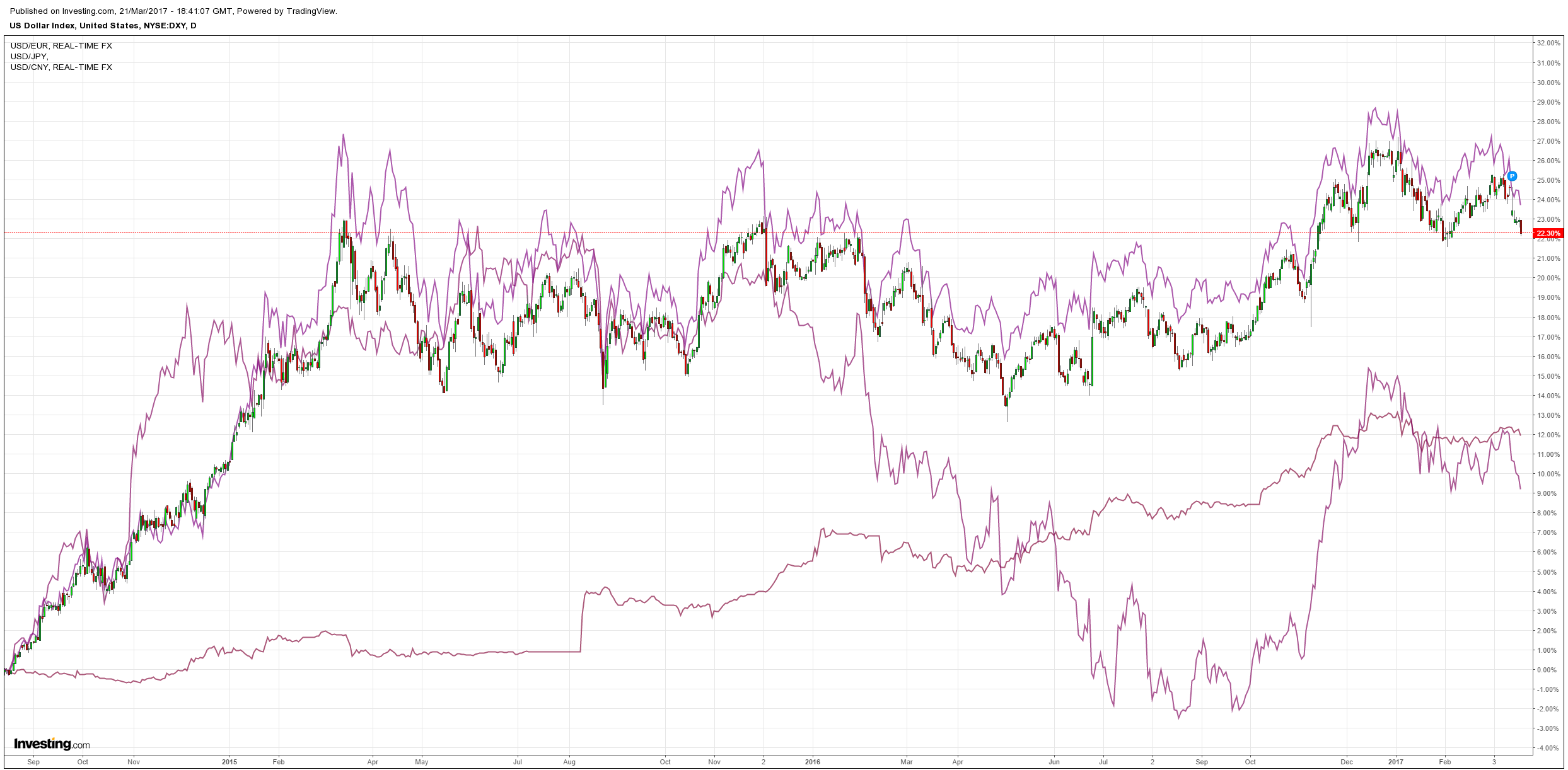

–We are also seeing a 6) breakout in the ‘long EM’ trade as the USD bull-case catalysts disappear, with now EM being an exceedingly popular ‘long’ in short-order (now with long-term valuation vs DM, carry and momentum all behind this EM +++ shift). Look at the moves seen over the past five-sessions alone against the Dollar:

–Finally, 7) a temporary stabilization in the crude selloff (off the back of the CFTC data showing us that short positions DOUBLED WoW, with OPEC jawboning on production-cut extensions yday to set-off a squeeze) is also supporting higher global developed market bond yields.

So what is the punchline here? Mark Orsley and I spent a lot of time on Friday looking at this ‘USD short’ near-to-medium-term contrarian trade, and as he showed in his “Macro Scan” piece yesterday, it’s an exceedingly interesting trade in light of the above “policy convergence” trend (mitigating rates differentials as prior USD ‘bull-driver’) and the consensual-positioning dynamic with Dollar as a ‘kicker’ (the newest BAML FMS out today shows that ‘long USD’ remains the ‘most crowded trade’ at 39% of respondents). This USD-downside trade should too look VERY interesting for the crowded “short rates” universe as a hedge that could actually contribute some near-term alpha if you get a week full of hawkish Fed speak (as noted last week we anticipate to keep ‘3 hikes’ on the table in 2017) or a larger decoupling btwn US rates and USD as the ECB may be forced to take-action ‘ahead of schedule’ (longer term).

RISK-ASSET BACKDROP = TOO CALM FOR COMFORT INTO ANY ‘VOL RIPPLES’:

The risk-asset backdrop is optically so bullish going into today’s session:

The Nasdaq is back nearing all-time highs (high-quality / secular-growth ‘FANG’ now +16% YTD)

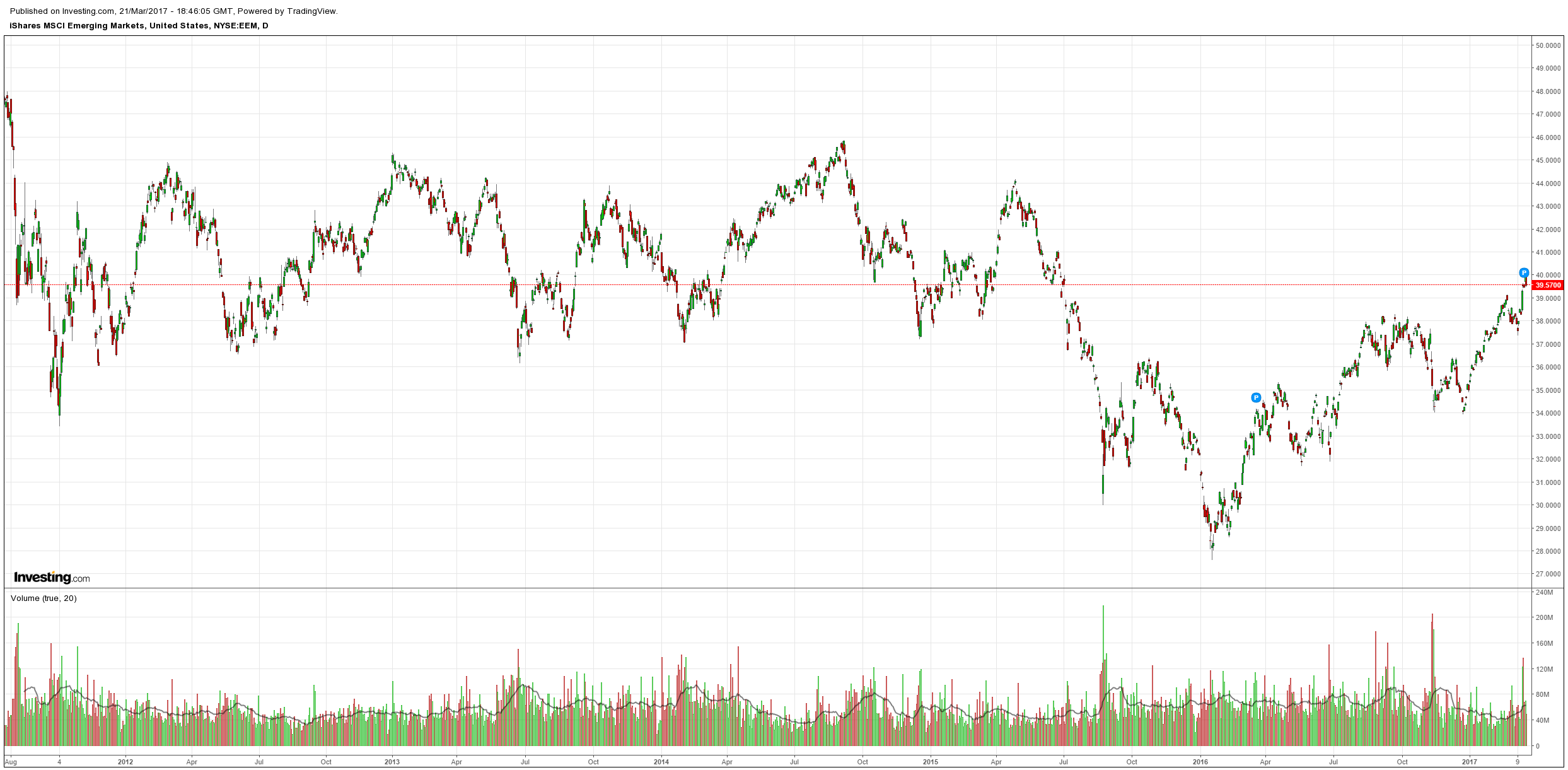

EEM is back at two year highs

FTSE All World Cyclicals Index is at 2 year highs

Shanghai Property Index is making YTD highs

Eurostoxx Banks Index at one year highs

Bloomberg US Financial Conditions at two year highs

Bloomberg US Economic Surprise Index at six year highs

5Y TIPS yields (as a proxy for ‘real rates’) have again turned negative rather abruptly–i.e. “looser” / “easier” financial conditions–following last week’s ‘dovish hike.’ This has reduced concerns of a scenario where a Fed that is “behind the curve” induces a policy-error with their hiking-trajectory.

Amazingly, all of this with no signs of a pulse from US fiscal policy progress.

This background has contributed to an annualized SPX Sharpe Ratio (admittedly early in year) over 5 (!), with vols beaten into submission as traditional ‘buyers’ step-aside (the refrain: “Why hedge if it only eats my alpha?”). Conversely, outright ‘short vol’ continues to drive huge alpha–as a very simple proxy, ‘short VIX’ ETF SVXY is +197.5% over the past year.

This is the largest contributor to ongoing concerns around the ‘short convexity’ in the system, as the ‘momentum’ generated in both ‘winning’ and ‘losing’ vol strategies above forces more $ and / or leverage (risk-parity, target vol strats) into the trade…and asymmetry grows, with ever-narrower historic / realized vols driving even-greater sizing:

SPX 60 DAY REALIZED VOL AT 10 YEAR LOW: Which of course is inversely correlated to ‘size’ of the leverage deployed on the ‘SPX long.’ It is important to note that 3m model could be considered ‘benchmark’ within the short-term vol target community.

It’s still ‘debatable to doubtful’ whether today’s nascent risk sell-off will see a sustained spike in volatility without further VaR-induced derisking…because per the above worldview, ‘vol spikes’ have repeatedly been used as opportunities to lay out more vol shorts (“do it until it stops working,” similar to “buy the dip”). For example, it might require some of the very popular ‘rate short’ to see a further destabilizing move into 2.30s as the ‘squeeze’ would drive cross-asset PNL distress (spilling-over into further stock drawdown or popular ‘long Dollar’ expressions like ‘short euro / pound / yen’).

Remember though, it was just last week where based-upon the complete breakdown in the Quant Insight macro factor PCA model that I was noting the recent ‘volatility signal’(as per the R^2 breakdown through 65% ‘predictability’ level within the SPX macro regime, which basically told us that the inputs of the past year could no longer rationalize the price action in the stock index).

What does that mean in English? The macro factor models are losing their ability to ‘explain’ the index moves. Currently both models’ R^2’s are now at 43% and 57%, respectively, from highs near 90%. Although the historical data set is not deep, you can see in the charts above (specifically featuring the long-term model) that the prior two instances where the R^2 dropped through the 65% “trigger” in the long-term 250d rolling model, we have seen a concurrent DOUBLING + in VIX through the trough and return through 65% “confidence” period, as the macro regime evolves and ultimately “firms.”

Advertisement

So, where does that leave us? Here’s my take:

the US economy is fine, markets simply got ahead of the curve on the Fed and fiscal hand-off;

the latter will come eventually and in the meantime animal spirits have materially lifted US growth prospects (see the capex rebound);

policy convergence is mild at best. Europe is miles behind the US in its recovery and tightening. This is being clouded by the lifting gloom around European elections;

oil is selling owing to its own technical factors as US shale destroys the OPEC cut and will have to go lower yet to cap shale. That’s upsetting the EM reflation trade despite the softening USD. But when we discover the price at which shale is stopped then we’ll stabilise and it will mostly benefit the US given everywhere else will see inflation fall further on the oil pullback while the shale recovery boosts the US.

Markets could definitely go lower here but we’re going to BTFD:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.