Big users need to keep fighting, Via The Australian:

Big energy users including Rio Tinto have accused electricity generators of flexing their market might to push up prices and called for new powers for the regulator to curb abuses, as some of Australia’s leading companies lashed the lack of energy and climate policy certainty for worsening the security and affordability of power.

…The criticism came as BHP Billiton — another major user and miner of energy coal — called for climate and energy policy to be integrated to address uncertainty about where energy companies should invest.

…BHP said stabilising SA’s energy supply should be the top priority for the government following a series of blackouts that cost the company $US135m.

…Rio Tinto, which last month sacked workers at its Boyne Island smelter because of soaring electricity prices, said the concentration of market power among a handful of generators had caused a breakdown in competition.

“The current regulatory framework of the NEM appears unable to curb the clear exercises of market power which have become increasingly apparent with the shifts in ownership, asset closure and in some cases consolidation of generators whose behaviour is unconstrained by considerations of affordability of electricity,’’ Rio said in its submission. It wants changes in the regulatory framework, and especially the powers of the Australian Energy Regulator, to intervene in cases where confidence in the system is being undermined by dramatic price spikes.

US industrial giant GE — whose local operations span wind and aircraft turbines as well as mining services — said Australia needed a “national energy blueprint” to guide decision-making “well beyond election cycles”.

Good advice. BHP is not losing money. It is one of those doing the gouging via its Gippsland JV with Exxon.

The ABC tries its hand at it:

It’s the great gas robbery. And it’s right before us in our utility bills.

When you next look in horror at your gas bill, think this: you are the unwitting victim of a gigantic game of risk shifting by the multinationals.

These companies have played the domestic customer on a break, because they saw something we didn’t see two years ago.

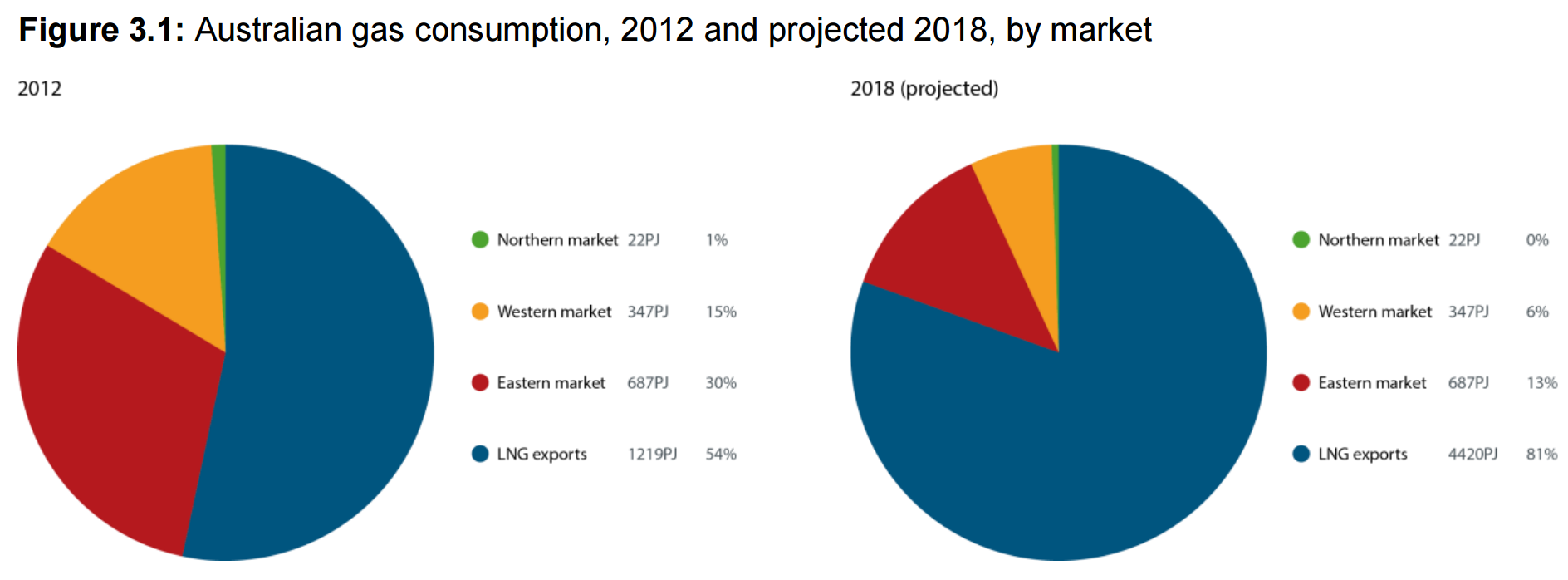

And it’s resulted in gas that was once destined for our heaters, cookers and manufacturing plants being sucked north to Gladstone where it is liquefied and sent to Japan, South Korea and China.

Those ginormous LNG projects in Queensland were pursued by their proponents on the industry-wide assumption that the price of oil would never dip below $US65 a barrel.

In fact, $US65 a barrel was the worst-case scenario when some of these projects were sanctioned.

Oil is now well south of that price and has been for some time. There’s expectation the price of oil will remain relatively low for some time yet.

This sounds awfully illogical, but stick with me.

The state and federal governments, which also assumed a certain oil price trajectory, gave approval for LNG projects on the expectation that the proponents would develop their large reserves.

But investing in coal seam gas isn’t as attractive as it once was. The cost of drill rigs, compressor stations, pipelines and other associated infrastructure have made new CSG wells more expensive than the gas we have been using on our stove tops and in our factories.

The LNG companies saw this coming two years ago and set about buying up the cheapest gas possible to fulfil their international contractual obligations.

It’s meant that Gladstone’s massive LNG trains are now sucking gas from as far as Victoria and South Australia.

…But sovereign risk means it’s probably too late to impose any reservation policy on existing LNG projects in Queensland or elsewhere.

However, if the companies do not accelerate the exploitation of their gas reserves, there is another tactic that will likely be used against them.

It’s a policy successfully deployed against oil and gas companies sitting on rich, undeveloped resource tenements off the coast of WA: use it or lose it.

So, the firms mis-allocated their capital owing to a price bubble but to take gas away now is sovereign risk? “It’s a robbery” but the firms must be protected? What kind of captured mindset is this?

The major problem revolves around one business in particular. Santos and GLNG, a risk is spelled out very plainly by a new report, via The Australian:

According to a report compiled by Energy Edge, the $US18.5 billion ($24.1bn) Gladstone LNG project, run by Santos, has at times been buying the equivalent of up to half of the whole east coast’s energy demand to meet a shortfall of gas to put through its two LNG production trains.

…“QCLNG and APLNG are currently either net long or balanced to the market, whereas GLNG is significantly short on equity supplies and must rely on third-party contracts,” Energy Edge said.

That was known by most observers.

But, using a range of public sources, Energy Edge says GLNG has sometimes bought a staggering 500-600 terajoules a day of gas on top of its own production.

Illustrating how substantial that volume is, the combined domestic demand from the pipeline-connected eastern states of Queensland, NSW, Victoria and Tasmania is about 1250 terajoules a day.

GLNG appears to already be averaging the use of about 300-400 terajoules a day of third-party gas — that is, gas outside the coal-seam gasfields it has developed specifically to feed its LNG project — for its LNG export.

As we know, Credit Suisse has provided the obvious answer:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31

■ If these contracts were then all diverted domestically, at US$65/bbl oil, they should deliver gas at Wallumbilla at $7.50 gj. This is highly competitive gas in the current environment we think and should certainly not be considered unreasonable by domestic buyers

So, if we end the gouge it will cost GLNG roughly $600m per annum.

Now, what will it cost us to not fix it?

We need to hold back a tiny 160Pj of gas to balance the domestic market. That amounts to a fantastically paltry 2.9% of total national demand or 3.6% of total export volumes. 80% of Australian gas production would still go to Asia.

At current rates of consumption, east coast gas of 1100PJs will cost $13.2bn at $12GJ. If we held back the 160Pj we could halve that. Electricity prices have also doubled to $100mWh on the gas price and we currently pay out roughly $5bn for our two terrawatts of electricity consumption. So that’s another $2.5bn saving if we can halve it. It is the effective equivalent of a $9bn tax (before we consider the knock-on effects of further capital mis-allocation) levied on east coast households and industry by the foreign shareholders and governments that own Curtis Island LNG. Pure economic rents siphoned off just because they can be.

But that’s not the end of it. These same firms and governments that have “stolen” the gas, lose money on every tonne that they ship offshore. They buggered up their investment metrics so horribly that when you include the cost of capital for building the plants, they are losing money hand over fist. This even includes the west coast LNG plants. As a result they can claim huge depreciation and write-offs on massively inflated investments and they pay no tax.

Are we so captured, colonised, in the thrall of mining, and dumb that we can’t be bothered saving ourselves $9bn plus per annum, the last of our manufacturing sector and the decarbonisation process, by reserving for ourselves a lousy 2.9% of our own gas, at the price of $600m to one failed LNG operation? Are we really happy to let foreign interests charge us for the privilege of hauling away our own high value gas as if it’s garbage?

By contrast, we let an entire car industry collapse because it was costing us $500m. But then you don’t dig cars out of the ground!

Barnaby Joyce wants a different answer:

Deputy Prime Minister Barnaby Joyce has started dismantling Australia’s sweeping ban on coal seam gas drilling, arguing a new scheme to divert a share of government royalties to farmers will overcome furious opposition in the bush.

Mr Joyce on Friday embraced a South Australian government plan to pay farmers 10 per cent of royalties in exchange for allowing gas wells on their land, saying the scheme should be rolled out nationally, with an exclusion of prime agricultural land.

In a bizarre and at times awkward press conference, the Energy Minister and SA Premier trade blows on energy policy. (Vision courtesy ABC News 24)

The Agriculture Minister said lifting moratoriums and giving landholders a fair price in exchange for access would equate to “a substantial turnaround in attitude and that is a very good outcome”.

“I can’t see people who start making hundreds of thousands or possibly millions of dollars a year having a backlash,” Mr Joyce told Fairfax Media.

Fine, bring it on. But it is too long term to fix the crisis and won’t help unless domestic reservation keeps the gas here anyway.

The gas market has outright failed Australia. All vital functions derived from energy are being plundered. It’s not sovereign risk, it is risk to the sovereign.

Nothing short of new rules for the market will do. Ban third party exports. Install domestic reservation and “use it or lose it” laws.