Roger Wilkins, a professor at the Melbourne Institute, is the latest to swallow the Kool Aid that Australia’s cities are the prime generators of Australia’s wealth. From The Australian:

By 2050, greater Melbourne will be home to more than eight million people, almost four times the forecast population of the rest of Victoria. “If you were starting from scratch we’d all be in big cities,” says Roger Wilkins, a professor at the Melbourne Institute. Keeping Australia’s regional areas strong is popular: state and federal governments typically have designated “regions ministers”. But the changing population distribution suggests job opportunities lie elsewhere…

“We know cities are productivity machines, small towns are kind of an anachronism,” says Wilkins. “They evolved in an era when the economic structure was very different, it was about servicing agricultural industries”…

Economic contributions have reflected population dynamics… “Population is driving that economic growth, but when you strip out the population you’re still seeing the higher value-add jobs and also the agglomeration effects. There’s density dividend,” [PwC’s Rob] Tyson says.

Like so many others, Wilkins has failed to understand the underlying drivers of Australia’s city-centric economic structure and whether it is desirable. In effect, he has focused on the quantity and distribution of growth in economic activity, rather than the quality and sustainability of that growth.

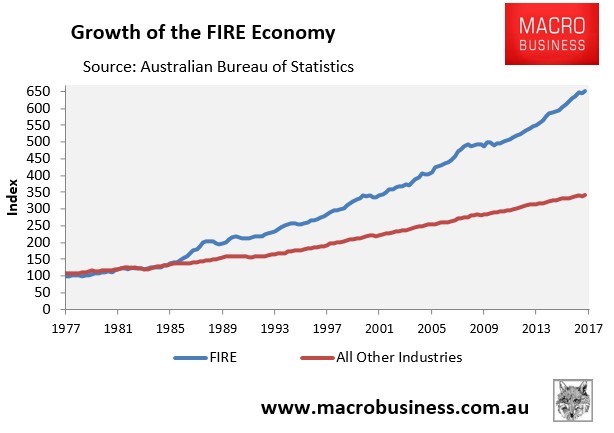

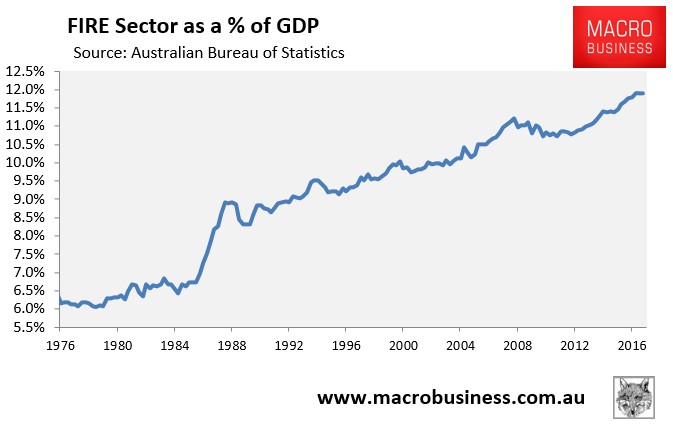

For example, that Australia’s cities – particularly Sydney and Melbourne – contribute the largest shares of economic activity is unsurprising given they are also home to Australia’s finance and insurance industries, whose activity has exploded on the back of Australia’s record high mortgage debt and inflated housing market, as well as compulsory superannuation (see below charts).

The rapid growth in the finance and insurance industries has come about through deliberate government policies, including tax lurks such as negative gearing and capital gains tax concessions, as well as urban consolidation policies combined with mass immigration, which have inflated land/house values and household debt. Compulsory superannuation has also driven resources to the funds management industry primarily operating out of Sydney and Melbourne. In both cases, economic rents have been transfer to the CBD from elsewhere.

But is this outcome desirable, and should it be celebrated, as Wilkins appears to have done? Many, including me, would argue that the financial sector is now far too large and is in fact a parasite that has created structural imbalances and damaged Australia’s longer-run productivity.

Would Australia really be worse-off if the median capital city house price was instead $350,000 rather than $700,000, mortgage debt was 70% of disposable incomes instead of 132%, and the banking sector was smaller and less profitable? In a similar vein, would the nation be worse-off if superannuation concessions had been much smaller and didn’t favour high income earners, and the funds management industry was smaller and less profitable? The answer is obviously no. And yet these types of questions are completely ignored by Wilkins and his ilk.

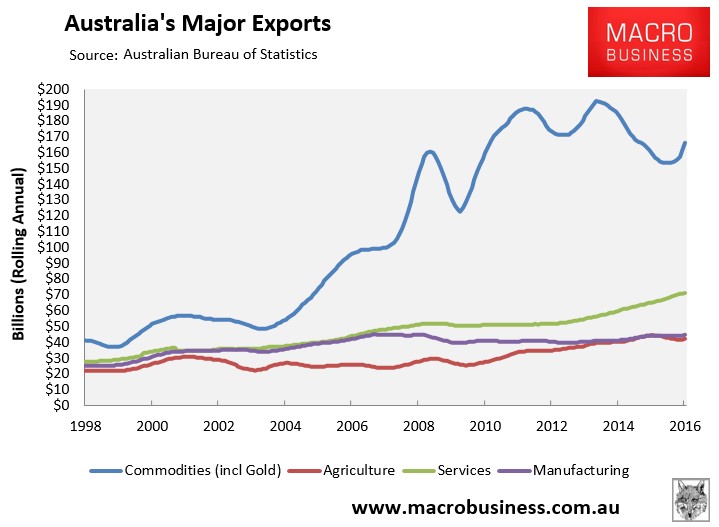

Wilkins has also failed to acknowledge that rural and regional areas provide Australia with not only its food, but also the lion’s share of its export revenue, which is effectively what pays for Australia’s imports (consumed mostly by city dwellers):

That is, Australia’s wealth is primarily derived from the nation’s immense mineral base.

Other things equal, making Australia’s cities grow bigger and bigger via mass immigration necessarily:

- dilutes Australia’s mineral wealth across more people, making incumbent residents poorer; and

- exacerbates existing infrastructure and housing bottlenecks in our major cities, leading to worsening congestion, reduced housing affordability, and overall reduced livability.

Australia would improve its trade balance and current account deficit if it simply cut the immigration rate and stopped Australia’s cities from growing too big. Again, Australia mostly pays its way in the world by selling-off its fixed mineral endowment. Increasing the number of people does not materially boost exports but does increase imports. Moreover, it requires us to sell-off Australia’s fixed mineral assets quicker to maintain a constant standard of living (other things equal).

Put another way, Australia would ship roughly the same amount of hard commodities and agriculture regardless of how many people are coming in as all the productive capacity has been set up and it doesn’t require more labour. So basically we are wrecking the trade balance by more people coming in each year (mostly to Sydney and Melbourne) because of all the additional imports.

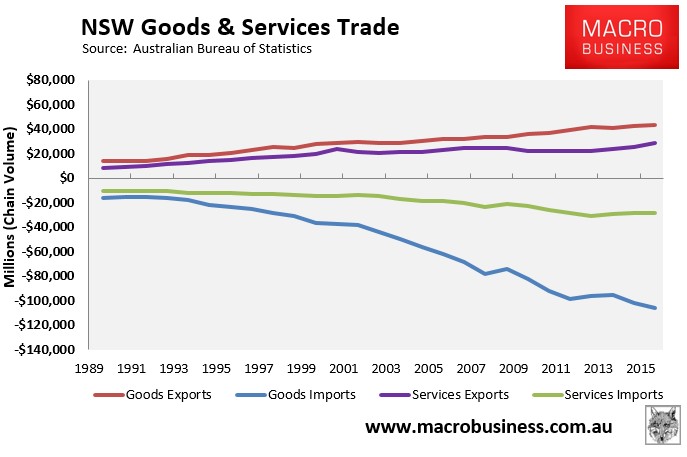

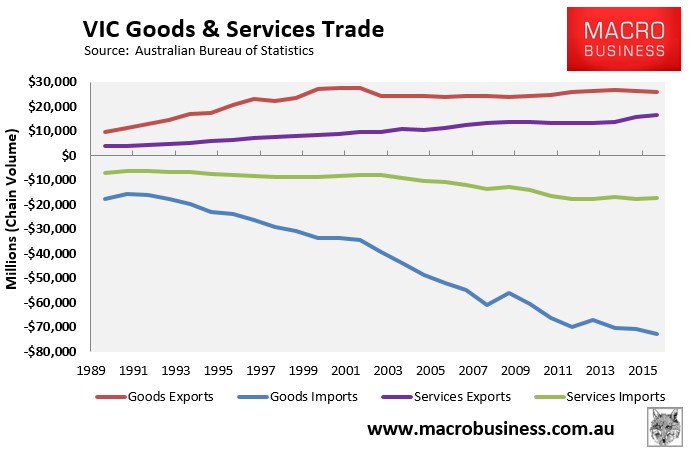

Anyone disputing this view only needs to view the below charts showing the stalling of export growth amid the sharply deteriorating trade balances in NSW and VIC, which of course have been the primary destinations of migrants:

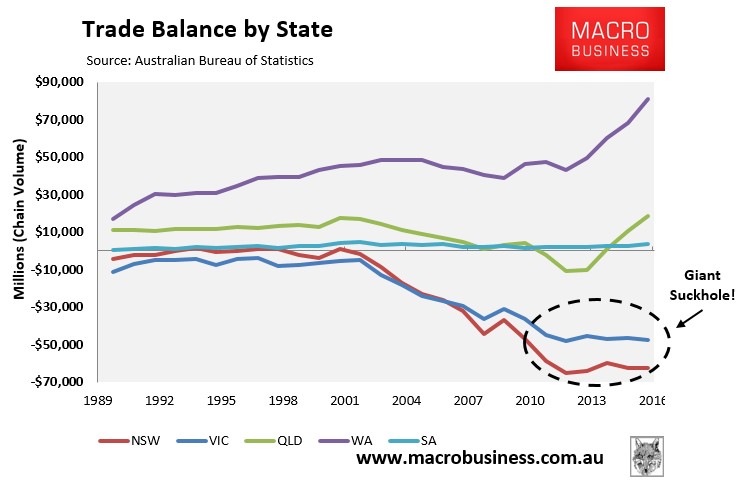

Which has driven gigantic trade deficits in Australia’s two biggest states:

Meanwhile, the infrastructure deficits in both Sydney and Melbourne, along with congestion, housing affordability and overall liveability worsens each year as more and more people flood into each city and push against bottlenecks amid woeful planning.

In sort, having bigger cities means a less competitive Australian economy and a wider current account – hardly a desirable situation. And yet people like Wilkins claim this represents economic progress!

Australia needs a well-diversified, balanced, economy with a wide range of industries located across the nation. Not an economy increasingly based on ticket-clipping and rent-seeking, whereby the spoils flow to a small group of CBD elites at the expense of everyone else.