DXY resumed its climb last night:

Even so, commodity currencies romped:

Gold held up but DXY is bringing the heat:

Brent was stable:

Base metals fell back:

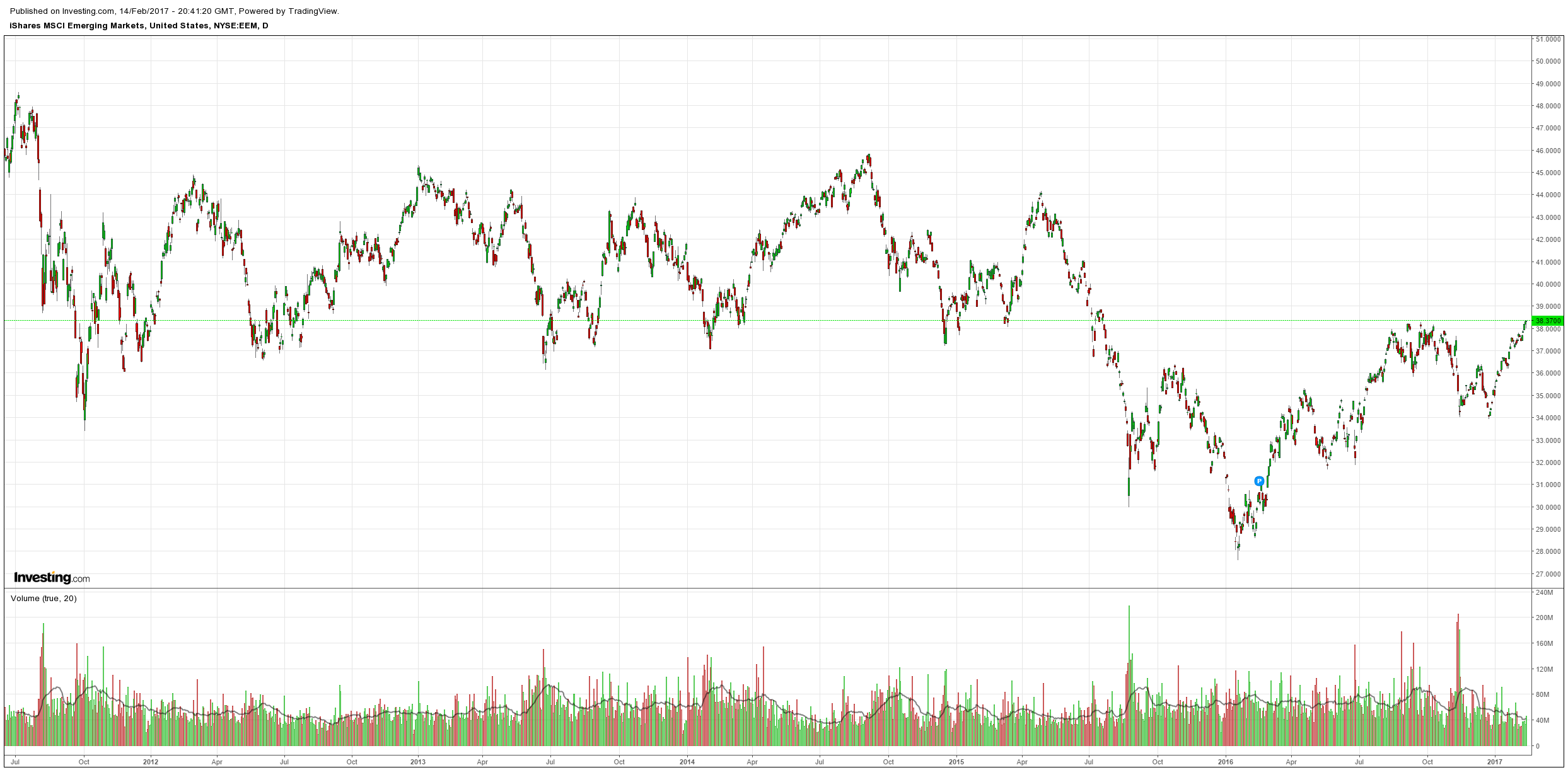

EM stocks were bid and are breaking out:

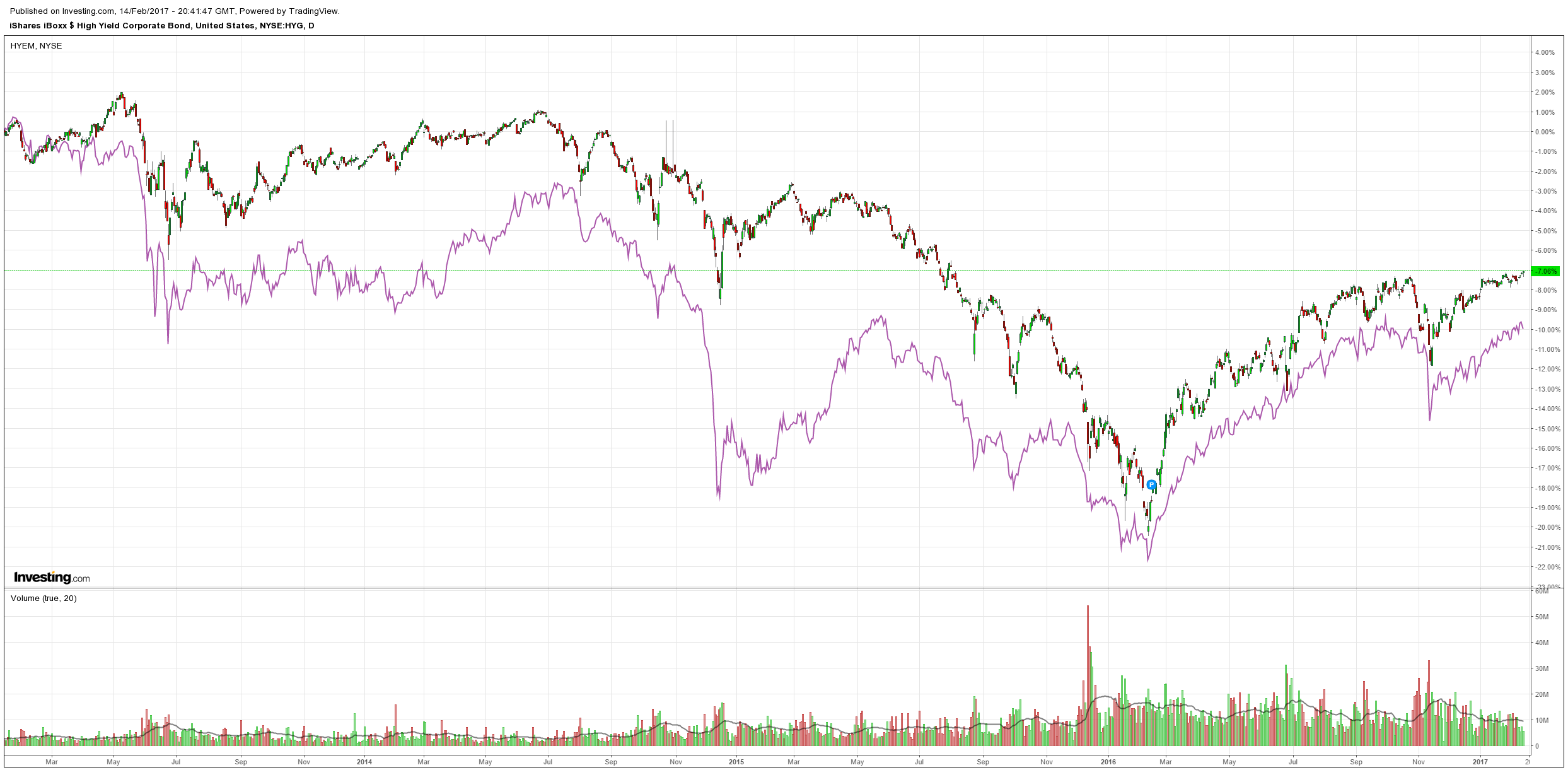

High yield fell back:

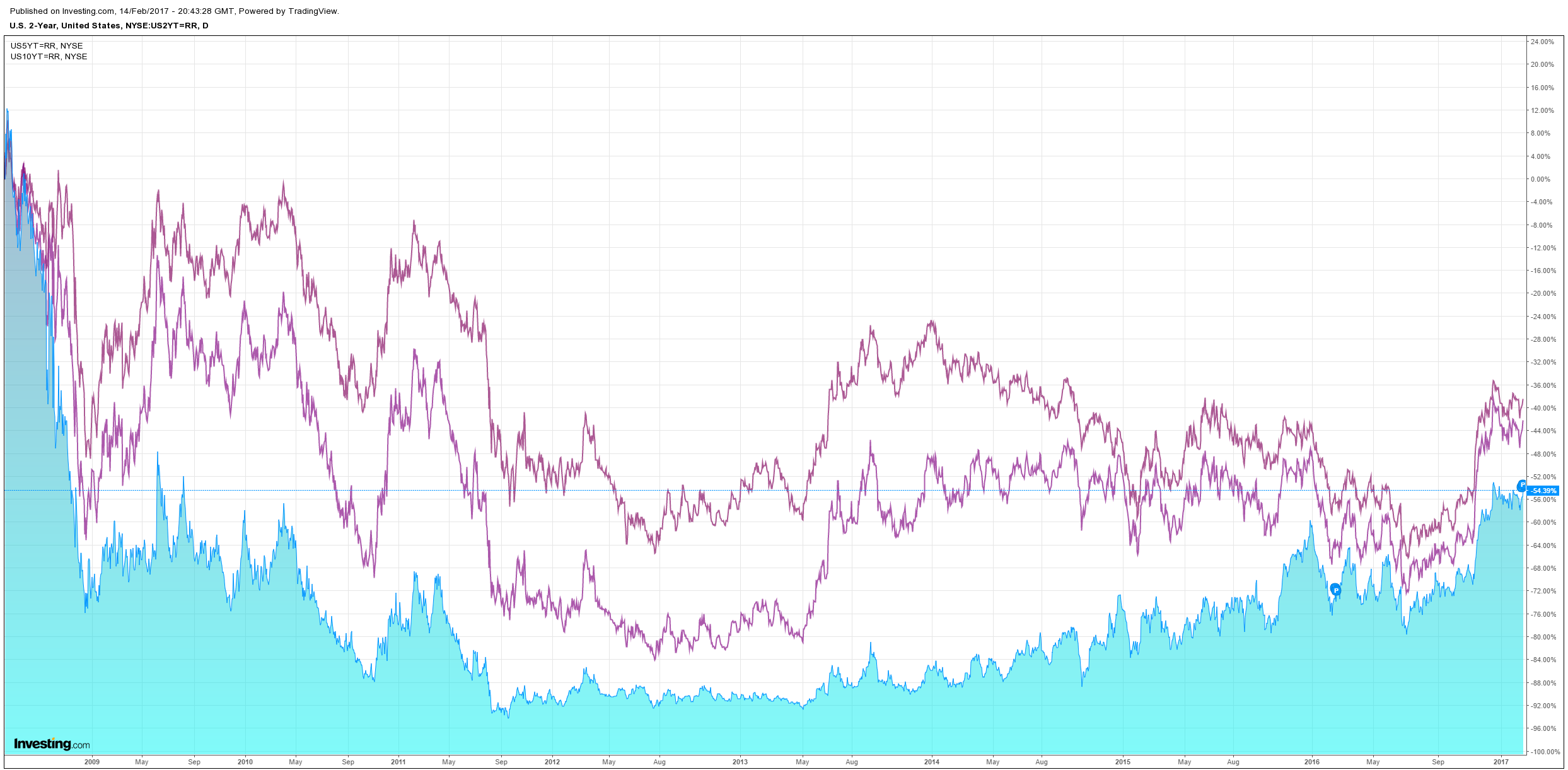

US bonds were flogged:

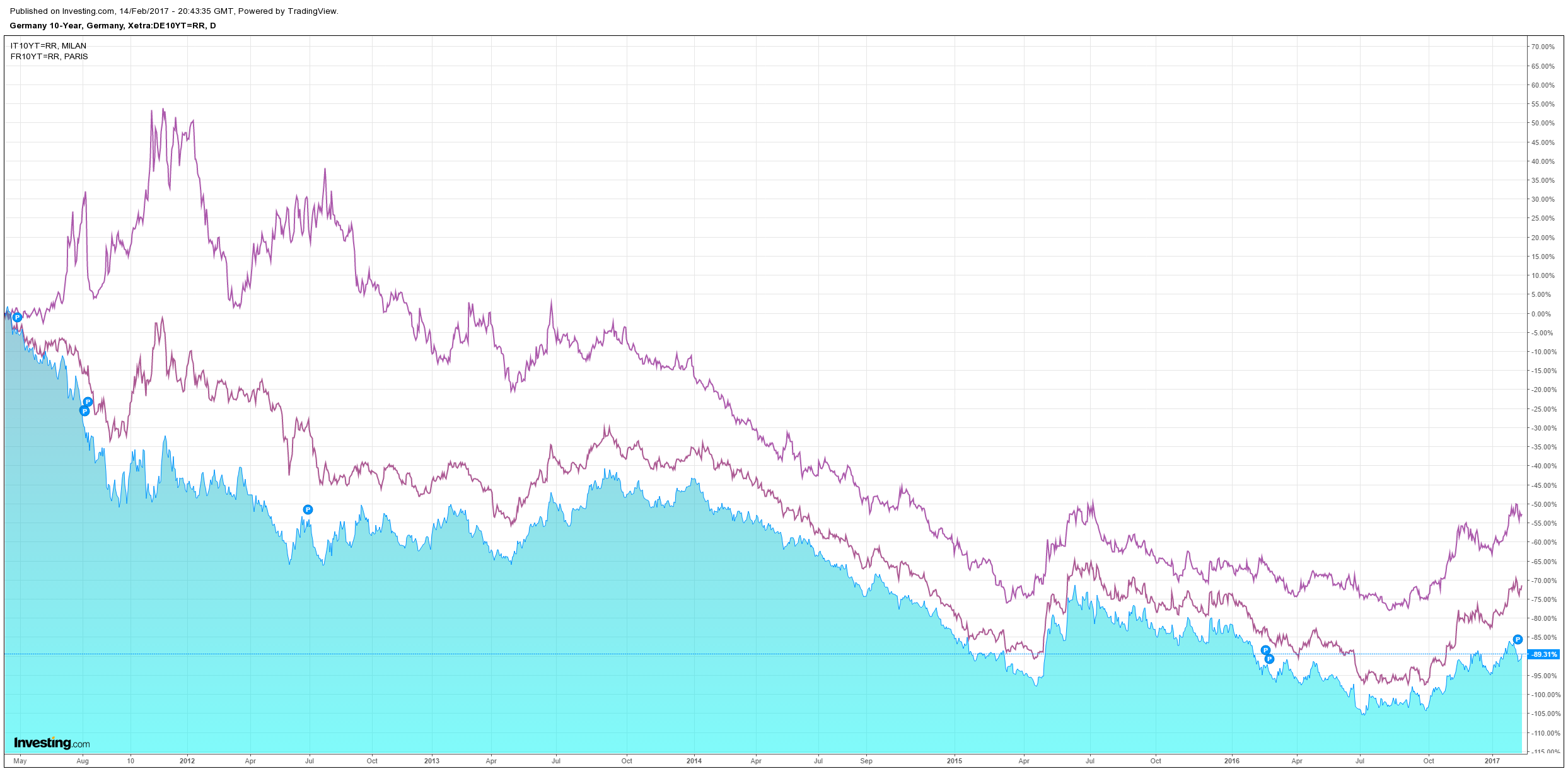

European spreads contracted:

And stock pushed to new highs:

Two events on the night. First, the Fed remained hawkish. Janet Yellen:

Since my appearance before this Committee last June, the economy has continued to make progress toward our dual-mandate objectives of maximum employment and price stability. In the labor market, job gains averaged 190,000 per month over the second half of 2016, and the number of jobs rose an additional 227,000 in January. Those gains bring the total increase in employment since its trough in early 2010 to nearly 16 million. In addition, the unemployment rate, which stood at 4.8 percent in January, is more than 5 percentage points lower than where it stood at its peak in 2010 and is now in line with the median of the Federal Open Market Committee (FOMC) participants’ estimates of its longer-run normal level. A broader measure of labor underutilization, which includes those marginally attached to the labor force and people who are working part time but would like a full-time job, has also continued to improve over the past year. In addition, the pace of wage growth has picked up relative to its pace of a few years ago, a further indication that the job market is tightening. Importantly, improvements in the labor market in recent years have been widespread, with large declines in the unemployment rates for all major demographic groups, including African Americans and Hispanics. Even so, it is discouraging that jobless rates for those minorities remain significantly higher than the rate for the nation overall.

Ongoing gains in the labor market have been accompanied by a further moderate expansion in economic activity. U.S. real gross domestic product is estimated to have risen 1.9 percent last year, the same as in 2015. Consumer spending has continued to rise at a healthy pace, supported by steady income gains, increases in the value of households’ financial assets and homes, favorable levels of consumer sentiment, and low interest rates. Last year’s sales of automobiles and light trucks were the highest annual total on record. In contrast, business investment was relatively soft for much of last year, though it posted some larger gains toward the end of the year in part reflecting an apparent end to the sharp declines in spending on drilling and mining structures; moreover, business sentiment has noticeably improved in the past few months. In addition, weak foreign growth and the appreciation of the dollar over the past two years have restrained manufacturing output. Meanwhile, housing construction has continued to trend up at only a modest pace in recent quarters. And, while the lean stock of homes for sale and ongoing labor market gains should provide some support to housing construction going forward, the recent increases in mortgage rates may impart some restraint.

Inflation moved up over the past year, mainly because of the diminishing effects of the earlier declines in energy prices and import prices. Total consumer prices as measured by the personal consumption expenditures (PCE) index rose 1.6 percent in the 12 months ending in December, still below the FOMC’s 2 percent objective but up 1 percentage point from its pace in 2015. Core PCE inflation, which excludes the volatile energy and food prices, moved up to about 1-3/4 percent.

My colleagues on the FOMC and I expect the economy to continue to expand at a moderate pace, with the job market strengthening somewhat further and inflation gradually rising to 2 percent.

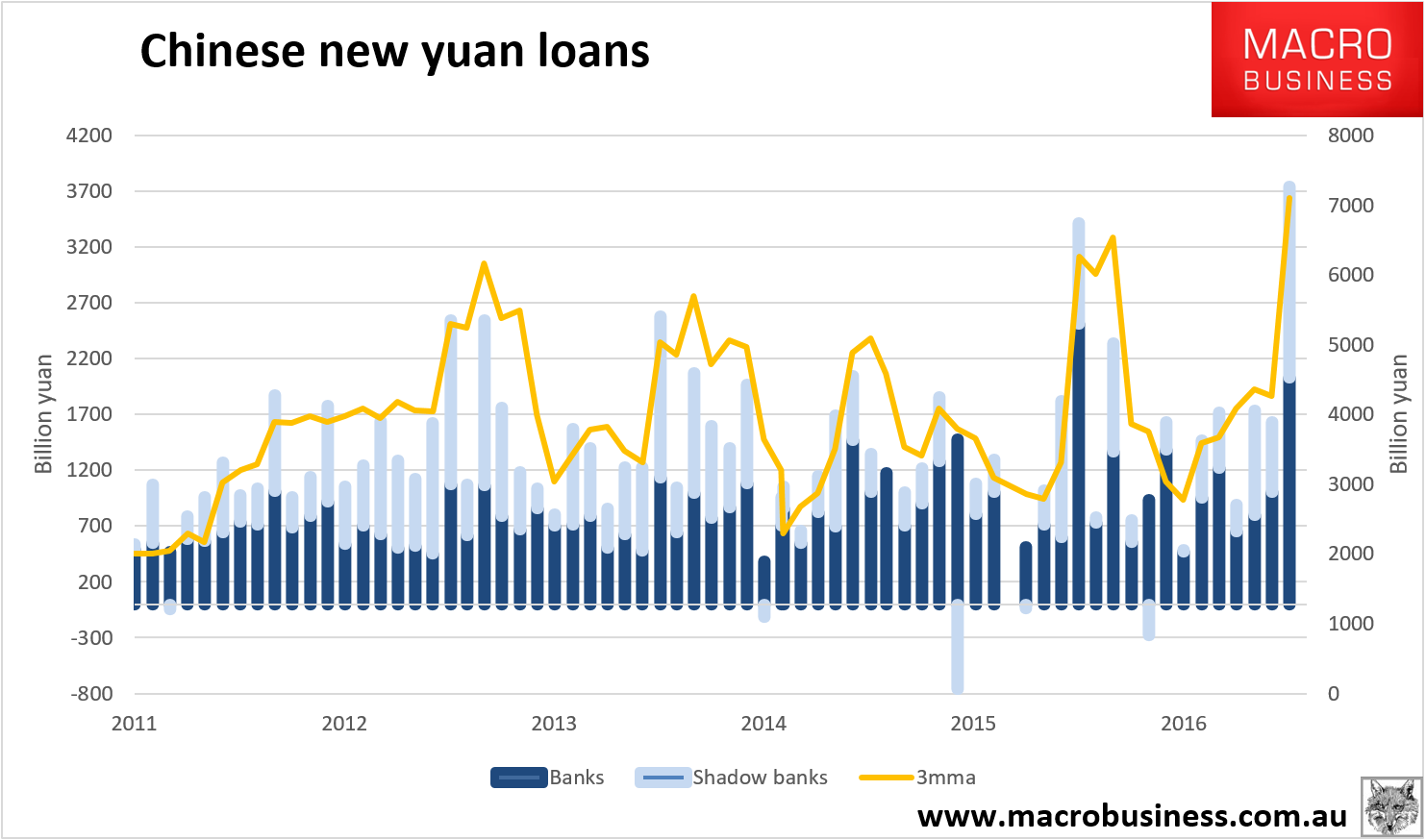

And second, Chinese credit was off the hook:

It has been my contention for the past six months that China was going to slow at the margin as the US powered on. The latter is intact, the former looks less convincing (we need to see all Q1 data to be sure). That means we’ll see more global reflation along with Trumpflation.

The main implication if this plays out is that global inflation will be higher, emerging markets will do better, commodity prices remain firmer, the Aussie dollar will remain higher for longer as local interest rates are not cut again this year. And all of that will also be offset by faster Fed rate hikes and a rising USD.

It actually doesn’t change MB allocations but shifts the relative benefits within them.