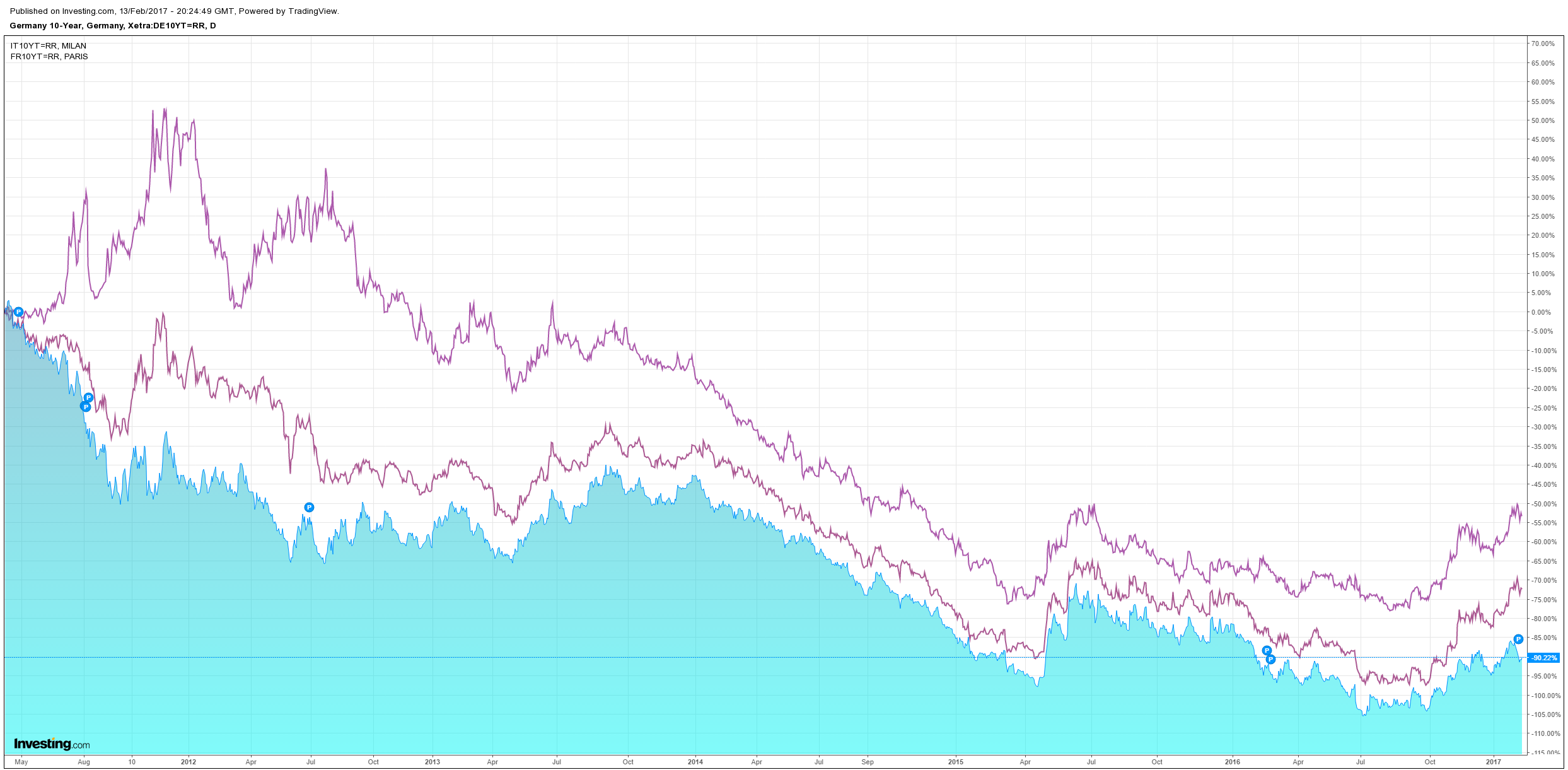

Trumpflation is powering again. BofAML looks at stocks today:

Advertisement

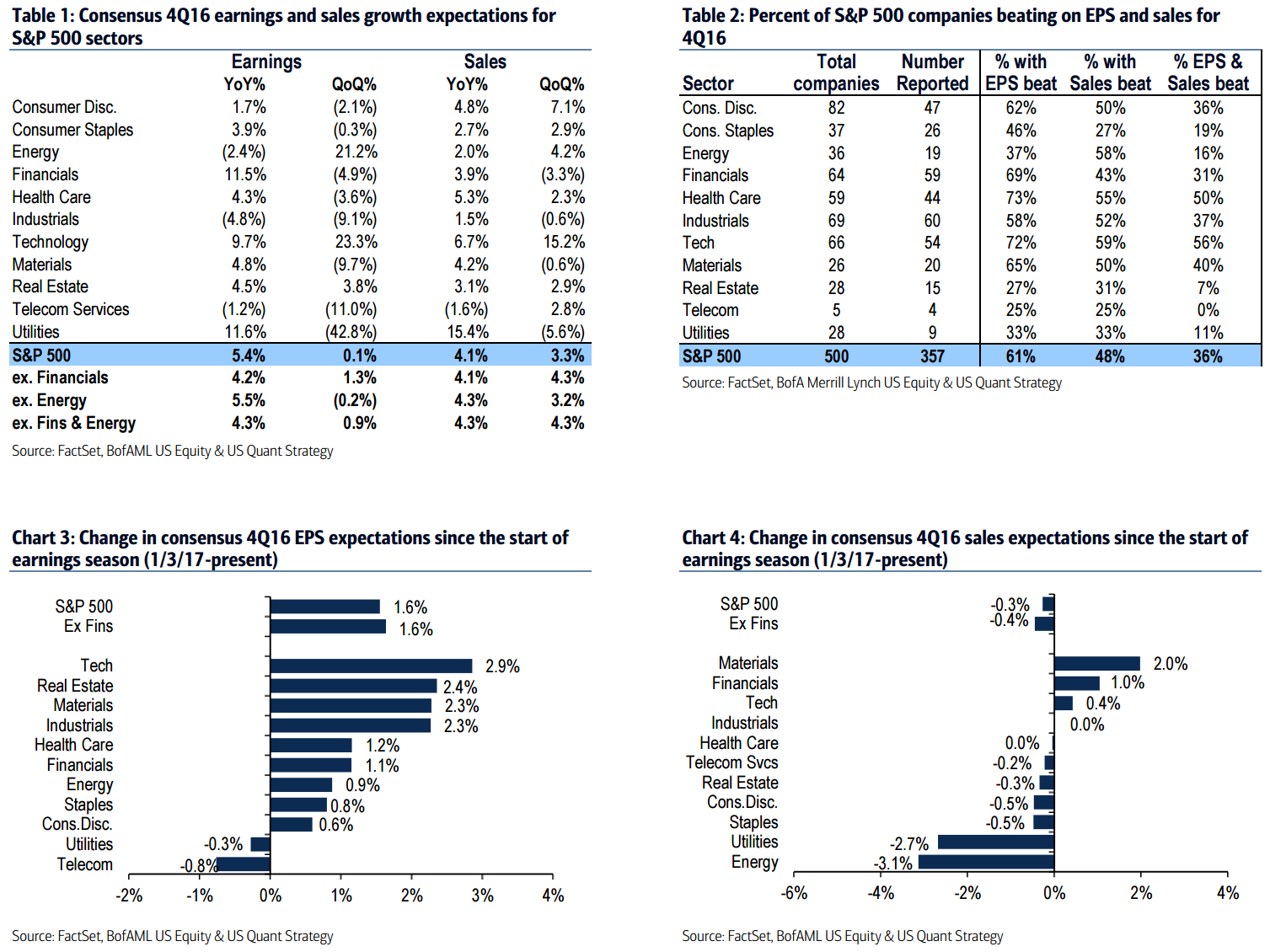

4Q EPS still above our forecast w/ 85% of earnings reported

After Week 5, 357 companies (~85% of S&P 500 earnings) have reported. Bottom-up EPS climbed to $31.56 from $31.46 a week ago, as strong Media results offset downward revisions in Insurance and misses in Utilities and IT Services. EPS has come in 2% above analysts’ expectations at the start of January and above our $31.25 forecast. While a 2% beat is smaller than average, 4Q estimates had been cut much less than average heading into earnings season. 4Q earnings growth is tracking +5% YoY on sales growth of +4% YoY (both better than in 3Q). This puts full-year EPS at $119 (+1% YoY) on sales growth of +2% YoY. 4Q earnings across all sectors except Utilities and Telecom have beaten expectations, with the biggest drivers of the beat in Banks, Tech Hardware, Capital Markets and Software. The remainder of results (dominated by the Retailers) will be spread out over coming weeks; we’ll issue a final 4Q recap in mid-March.

Proportion of beats in-line with history; Tech & HC lead

61% of companies have beaten on EPS, 48% have beaten on sales and 36% have beaten on both, in-line with the post-2000 average of 35% for top- and bottom-line beats (but with sales beats alone still below their 56% avg, and EPS beats alone above their 53% avg). Health Care and Tech have seen the most positive surprises, which has been true in most recent quarters. Staples, Telecom and Utilities have seen the most misses. While surprises had generated alpha earlier in the quarter, spreads have since narrowed to below historical levels. But one area where surprises have generated alpha is in Consumer Discretionary, where misses have underperformed beats by 9ppt on avg. the following day.

Sales miss narrows as growth continues to improve

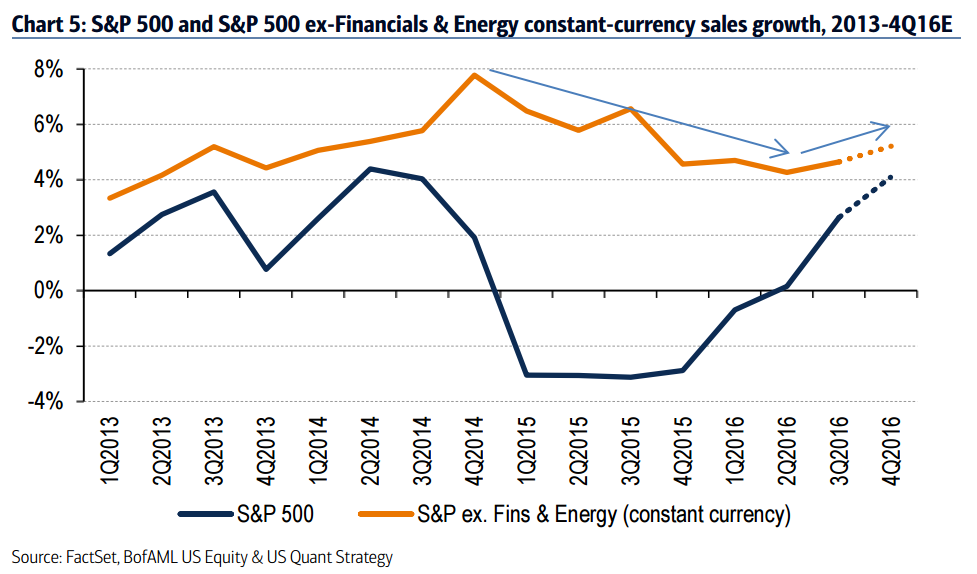

The magnitude of the aggregate sales miss narrowed last week, with sales coming in just 0.3% below analysts’ expectations. While most sectors have in-line sales, misses within Energy and the two Consumer sectors have led overall sales to miss, offset by beats in Financials, Materials and Tech. Constant-currency sales growth for the S&P ex-Fins. & Energy has accelerated by 0.6ppt in 4Q to +5.2% YoY, suggesting demand has finally begun to recover. Sales growth has accelerated in six of the eleven sectors this quarter, in contrast to the earnings pick-up that was chiefly driven by Energy and Financials.

Better results up the cap spectrum

Small cap earnings season is in full swing, but results for this size segment have been weaker than for large caps. Earnings are coming in just 1% better than expected (vs. 2% in large caps), with just 32% of companies beating on the top and bottom line (vs. 36% in large caps). Earnings growth is tracking -1% YoY on sales growth of +2% YoY, both lower than in large caps. Results for the mid caps have generally fallen in between the other two size segments on growth and surprises.

Guidance tepid, but a different read suggests record optimism

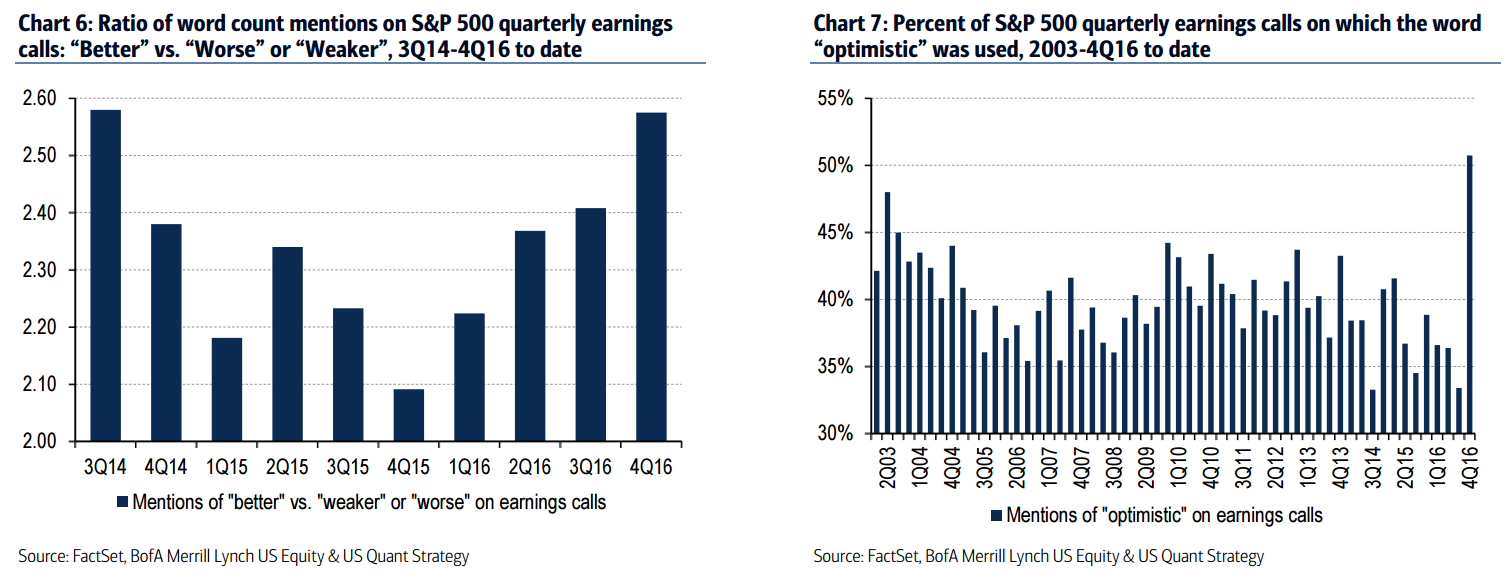

As we’ve noted in prior weeks, guidance during 4Q earnings season is typically less positive than in other quarters as management sets a low bar for the year. While the ratio of above- vs. below consensus guidance has remained weak so far this month at 0.55, it is up from 0.44 in January and slightly above the post-2000 average of 0.48 for both months. While managements’ official outlooks may be nothing to write home about, commentary on earnings calls has been notably optimistic. A simple count of mentions of the word “better” relative to mentions of “worse” or “weaker” on earnings calls is tracking its highest in over two years. And the word “optimistic” has been used on a record 51% of the calls this quarter, the highest ever in our data history (since 2003). See Chart 6 and Chart 7. This optimism could translate into future earnings revisions.

Dare I call that an optimism bubble? The market will need to see earnings deliver for these valuations at some point but MB continues to believe that Trump will do enough.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.