Friday night saw markets pile into reflation trades. The USD powered back:

Commodity currencies roared, the Aussie too:

Gold sagged:

Brent recovered:

Base metals launched, though copper was helped by the Escondida closure:

And big miners:

And EM stocks:

High yield was also firm:

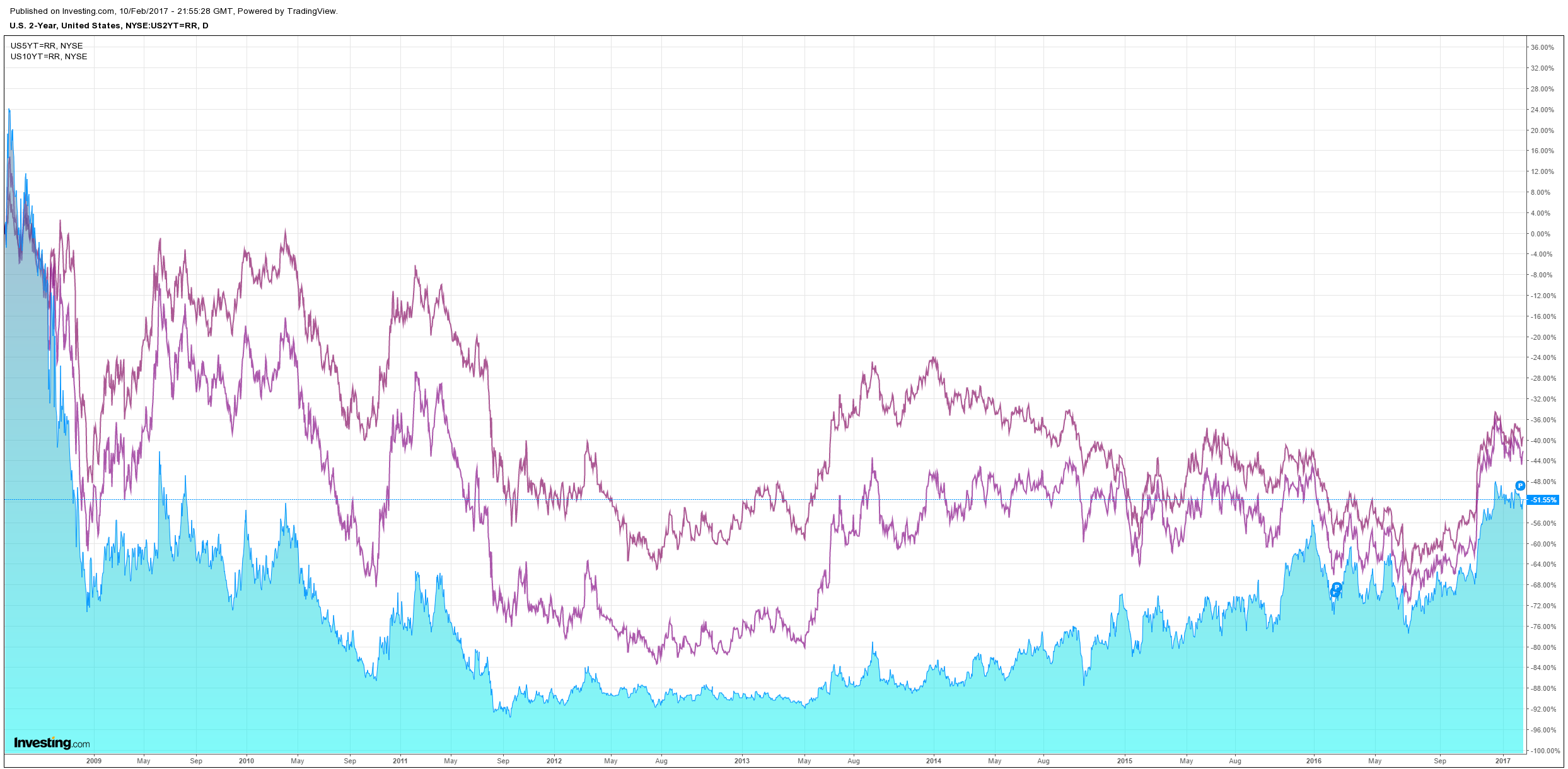

Treasuries sold:

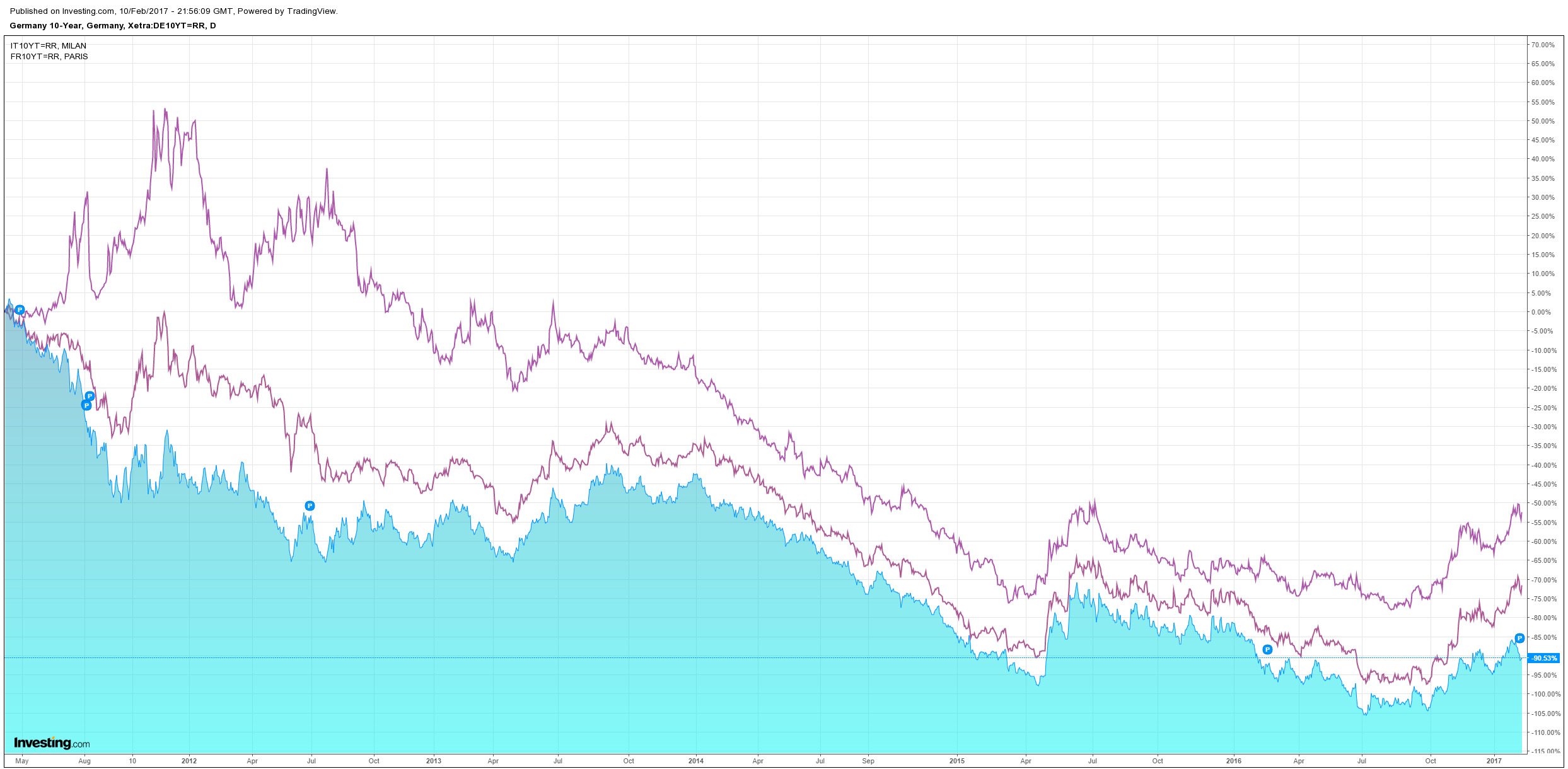

European spreads widened:

And US stocks hit record highs:

Somebody appears to have gotten a hold of Donald Trump and shaken some sense into him. Via the FT:

Donald Trump sought to defuse Asian tensions created in the early weeks of his presidency by warmly welcoming Japan’s prime minister to the White House just hours after calling his Chinese counterpart to reaffirm US support for the “One China” policy.

Mr Trump has unsettled both allies and foes in the region by withdrawing from a Japanese-backed 12-nation Pacific Rim trade pact on his first day in the White House and phoning the president of Taiwan, the island Beijing regards as a renegade province.

While Mr Trump often bashed Japan during the presidential race, he has offered Shinzo Abe, the Japanese premier, a lavish two-day summit that will see the leaders dine together four times, fly together on Air Force One, and play a round of golf at the president’s resort in South Florida, which has been dubbed the “Winter White House”.

“The bonds between our two nations and the friendship between our two peoples is very, very deep. This administration is committed to bringing these ties even closer,” Mr Trump said at a White House news conference with Mr Abe. “The US-Japanese alliance is the cornerstone of peace and stability in the Pacific region.”

Tokyo has been eager to re-establish close relations with Washington, its main security guarantor, after Mr Trump’s unnerving campaign. Ahead of the White House meeting, Mr Abe said he wanted to show the world that the US and Japan had an “unwavering alliance”.

The push by both sides to bolster ties is partly designed to provide a bulwark against China, as tensions remain high in the South China Sea and East China Sea. While China will be nervous about a closening US-Japan relationship, Mr Trump on Thursday told Chinese President Xi Jinping he would honour the “One China” policy under which the US recognises Beijing — not Taipei — as the sole legal government of China.

The Japanese have played this perfectly, full of flattery and bearing “America first” gifts, which can be juxtaposed with Australia’s worst in show effort of dumping refugees and publicly embarrassing the narcissist, for which Trunbull (and we) will pay a price later you can be certain. The Japanese are helping put some meat on the potential infrastructure spend as well.

The unfortunate Trump travel ban is still making waves, via Reuters:

U.S. President Donald Trump promised on Friday to introduce additional national security steps, a day after an appeals court refused to reinstate his travel ban on refugees and citizens from seven Muslim-majority countries, and he expressed confidence his order would ultimately be upheld by the courts.

The White House is not ruling out the possibility of rewriting Trump’s Jan. 27 order in light of the actions by a federal judge in Seattle and an appeals court in San Francisco that put the directive on hold, an administration official said.

Trump’s order, which he has called a national security measure to head off attacks by Islamist militants, barred people from Iran, Iraq, Libya, Somalia, Sudan, Syria and Yemen from entering for 90 days and all refugees for 120 days, except refugees from Syria, who are banned indefinitely.

“We are going to do whatever’s necessary to keep our country safe,” Trump said during a White House news conference with visiting Japanese Prime Minister Shinzo Abe.

But there is more going on that smooths out the Trump edges. The tax reform agenda may not be all bad, via Bloomberg:

Former Goldman Sachs Group Inc. president Gary Cohn is leading the effort to craft President Donald Trump’s plan to overhaul taxes that will be released within weeks, a White House official said.

Unnamed congressional leaders have been consulted on the blueprint, the official said. It’s separate from Trump’s proposed budget, the official said, requesting anonymity because the plan is still under development.

During a meeting at the White House with U.S. airline executives Thursday, Trump said he had a “phenomenal” plan to revamp business taxes that would be revealed within the next two or three weeks, without offering details. White House Press Secretary Sean Spicer told reporters later that day that specifics would emerge only in the coming weeks. Still, he said the White House is at work on an outline of the most comprehensive business and individual tax overhaul since 1986.

…Cohn said last week that he has been meeting with members of Congress and working on two key goals: cutting corporate income taxes and individual income taxes. He emphasized during a Feb. 3 interview with Fox Business News that he has been focused on tax cuts for low earners.

“We’re not spending a lot of time with the high earners,” Cohn said during that interview.

A combined working class and corporate tax cut would be an excellent combination if it were structured well, stimulating both demand and investment, as well as helping to begin the rebalancing of years of “trickle down” rorting by the wealthy. The devil will be in the detail of course. If it is funded by the border adjustment tax then it’s not going to do much good for anyone given the currency will wipe out gains fast and it will be more like tax system vandalism. If I were Trump I’d be opting for less aggressive corporate tax cuts and more aggressive lower income tax cuts (and I’d hike taxes on the rich to pay for them which we won’t see).

Anyway, the smoothing of Trumpsatan is already paying dividends in markets as Trumpflation resumes. Citi has some thoughts on the wider implications for the global economy.

We offer some thoughts on the state of the EM corporate debt market three months after the US election. Our initial views, as expressed in our 2017 outlook, were primarily negative for spreads albeit positive for commodities. Since then, the possibility of Border Tax Adjustment (BTA) has loomed over the market as a negative for EMFX and manufacturers, yet a possible Infrastructure Spending boom has buoyed commodities. In the conflict between potential weaker EMFX (bad for EM credit) and stronger commodities (good for EM credit), the good appears to be winning. This is in part because EMFX has not really sold off outside of Mexico, which has also begun to rally. It seems the market may be backing off some of its more inflationary expectations, at least until proven otherwise. In this note, we explore this theme a bit further and offer a scenario analysis of potential “reflationary” policy implementation odds and outcomes. On balance, a “Muddle Through” scenario favors EM corporate debt. NAFTA remains a wildcard, as do spikes in market volatility.

Donald Trump’s election was generally seen to be negative for EM credit. The idea that a US centric trade policy, with or without BTA driven tax reform, would pull marginal investment away from certain EMs to the US had, and has, a degree of credibility, in our view. In addition, deregulation and a US fiscal stimulus via infrastructure spending was seen as positive for US employment and growth, and commodity demand, all of which would drive equity markets, commodity prices and the USD higher. These policies, combined with import substitution, were expected to result in the “Trump reflation” scenario of the US economy, which means US rates need to move higher. On the basis of these outcomes, we based our 2017 outlook on the expectations of weaker EMFX, lower EM capital inflows, and higher US rates. Our modeling showed that EM corporate spreads should widen 30bps from the spreads prevailing at the end of November.

What a difference a few months makes. The expectant Trump reflation has actually resulted in EM spreads tightening as investors flocked to higher overall yields and a commodity rally driven by expectations of greater US growth. EM corporate spreads have tightened 30bps since the election, and are 50bps tighter than their immediate post-election wides. Investor flows, as measured by EPFR, have turned back to positive after suffering outflows in November and December, indicating little broad retrenchment in investor appetite. Our 2017 outlook implied a total return of 2.4% for the year for corporates, assuming a 20bps rise in UST and 30bps widening of spreads. Total returns YTD are 1.7%. Under these metrics, investors could be forgiven the temptation to just put everything in neutral and call it a year.

Clearly something is amiss. Either the market is correctly seeing the Trump reflation as positive for global growth (and commodities), even if its timing and strength are somewhat inexact, or it is wagering that much of what has been promised will not be implemented, and the negative fallout on EM is misplaced. We offer four scenarios regarding the Administration’s ability to achieve real progress on repealing/replacing Obamacare, Tax Reform with BTA, Trade Protectionism, Infrastructure Spending and Deregulation concurrently for the 2017 legislative year. Deregulation and to some degree Trade Protectionism can be achieved via decree, but the other measures require legislative approval, and the opposition has promised to be obstructionist regarding most Trump initiatives, and so far an inexperienced Administration seems destined to get a late start on its calendar. We take this to mean that Trump reflation is likely to be a smaller than expected.

We assume the President achieves a repeal/replacement of Obamacare in all our scenarios, which we label Peak Trump, Failed Trump, and Muddle Through Trump A, B and C. In each scenario, we make assumptions on how 10 year UST 2 yields, S&P 500, VIX, EMFX and commodities (ie, oil) react. Peak Trump is where the administration gets most everything it wants passed, and in 2017 no less. This is actually the most bullish scenario for EM spreads, as it is the most bullish for commodities. However, dramatically higher UST erodes the total return. We assign this a 20% probability. Failed Trump (15% probability) is where the administration cannot get anything other than a change to Obamacare, and pulls out of NAFTA to show it is doing something on trade. This is the most negative scenario for EM spreads as EMFX and commodities both likely decline, but lower UST yields soften the blow and total returns for the balance of 2017 remain positive. Finally, we offer three versions of a Muddle Through Trump scenario (65% combined probability). Version A (20%) is Tax Reform is passed, NAFTA modernized, but no Infrastructure Plan. Version B (15%) has an Infrastructure Plan, no Tax Reform, and US exits NAFTA. Version C (30%) has an Infrastructure Plan, no Tax Reform, and NAFTA is modernized. We see this as the single most likely scenario, as well as the most positive outcome for EM corporates.

This is confusing two things. The Trump reflation is not driving commodities, the Chinese reflation is doing that. US consumption of all commodities but oil is tiny compared with China. As well, the rising USD remains a bearish headwind for dirt. China is tightening fast so commodities will come off eventually (this year) regardless of Trump’s success.

On the other hand, the US remains a conspicuous bull market even if Trump only succeeds moderately. Moreover, it’s reflation will be aided by the coming fade in the great Chinese bear market rally as it takes heat off inflation and holds back the Fed. Europe remains an untouchable time bomb.

MB allocations are unchanged:

- buy the dips in the S&P500 and USD;

- sell the rallies in commodities and AUD;

- buy the dips in Aussie bonds;

- buy the dips in gold miners for portfolio insurance.