DXY eased overnight:

Commodity currencies firmed:

Gold was impressive:

Brent not so much:

Base metals was strong for no obvious reason:

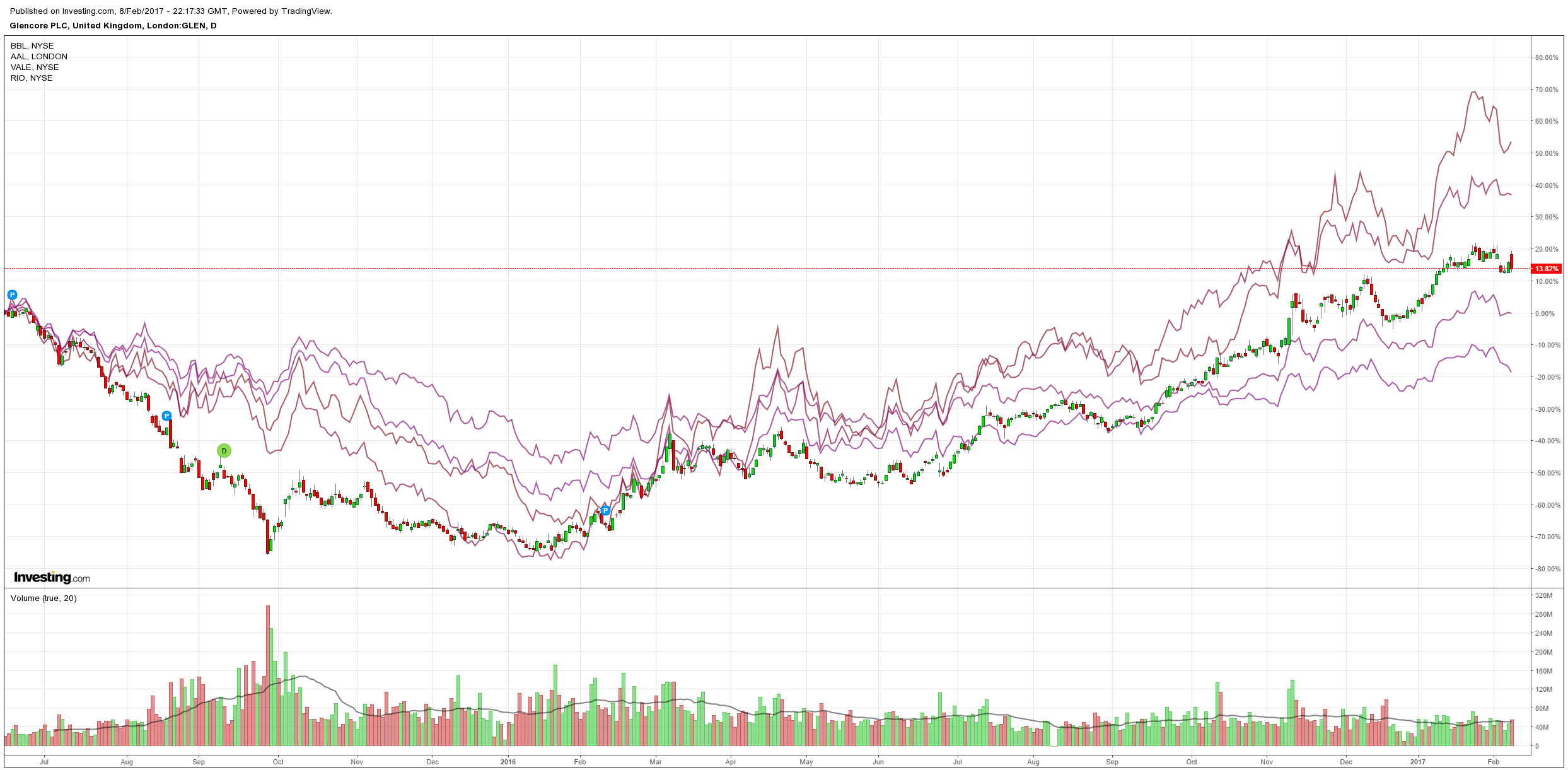

Big miners were not:

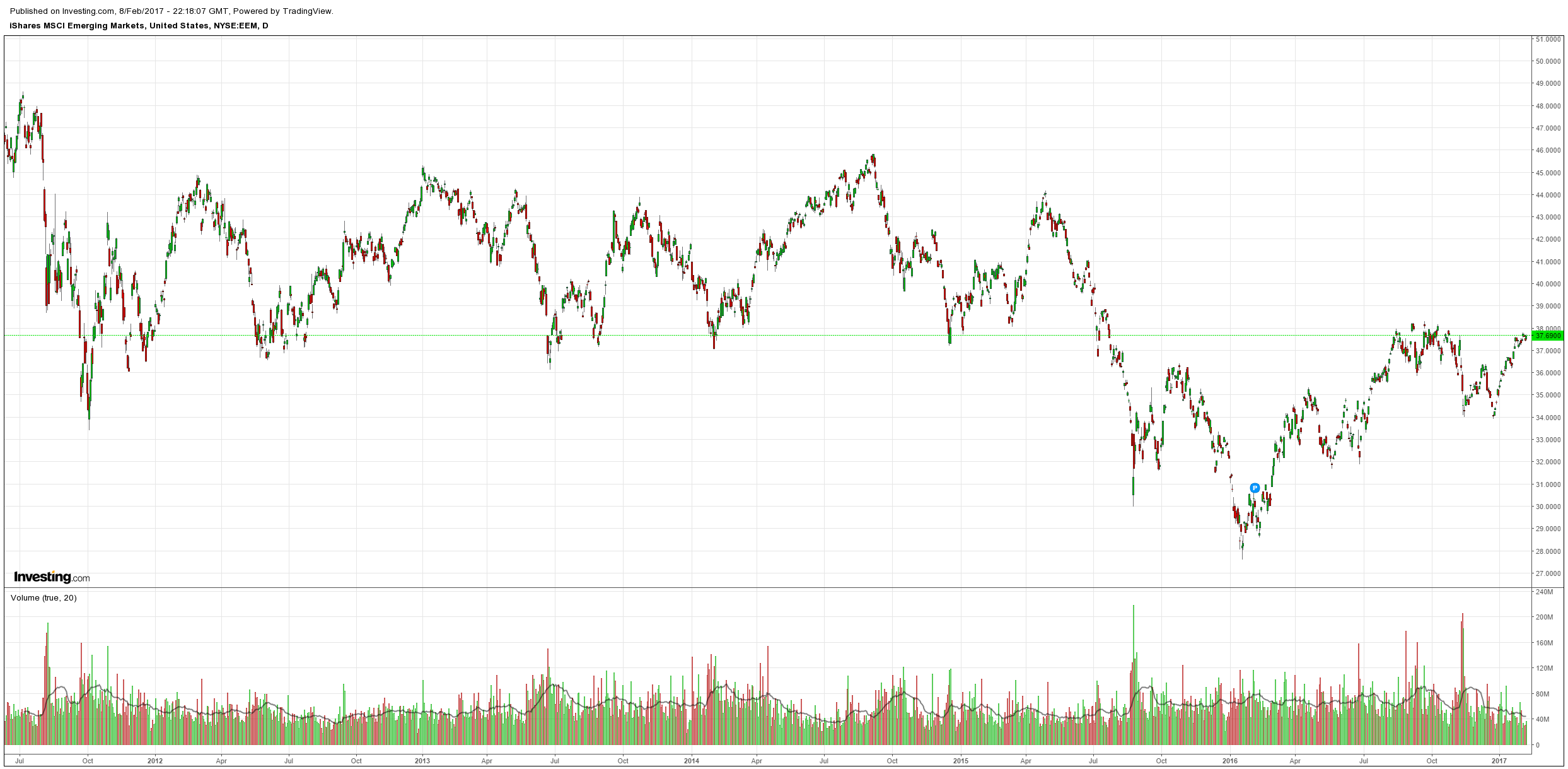

EM stocks firmed:

EM high yield too:

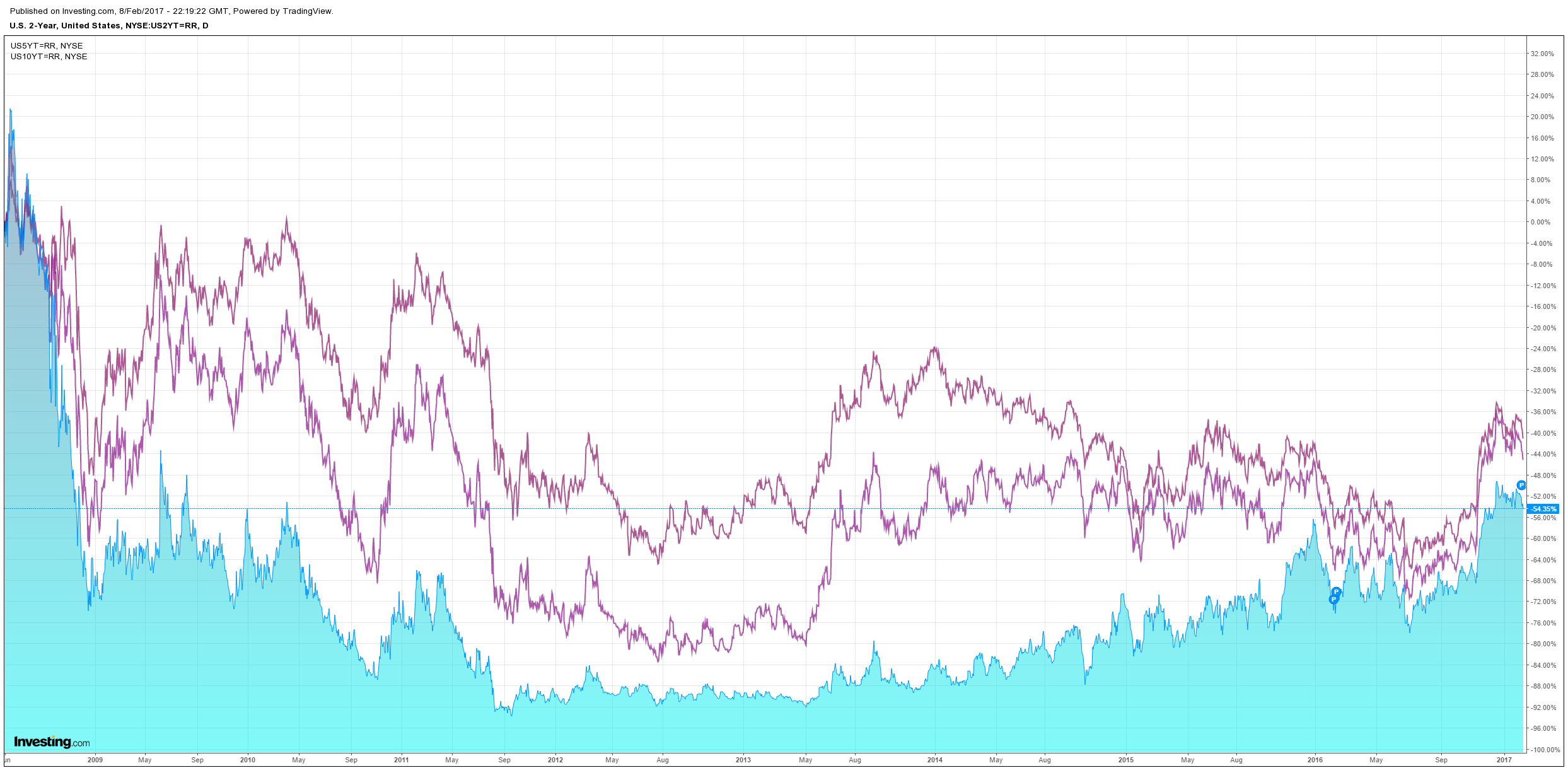

US bonds were bought big:

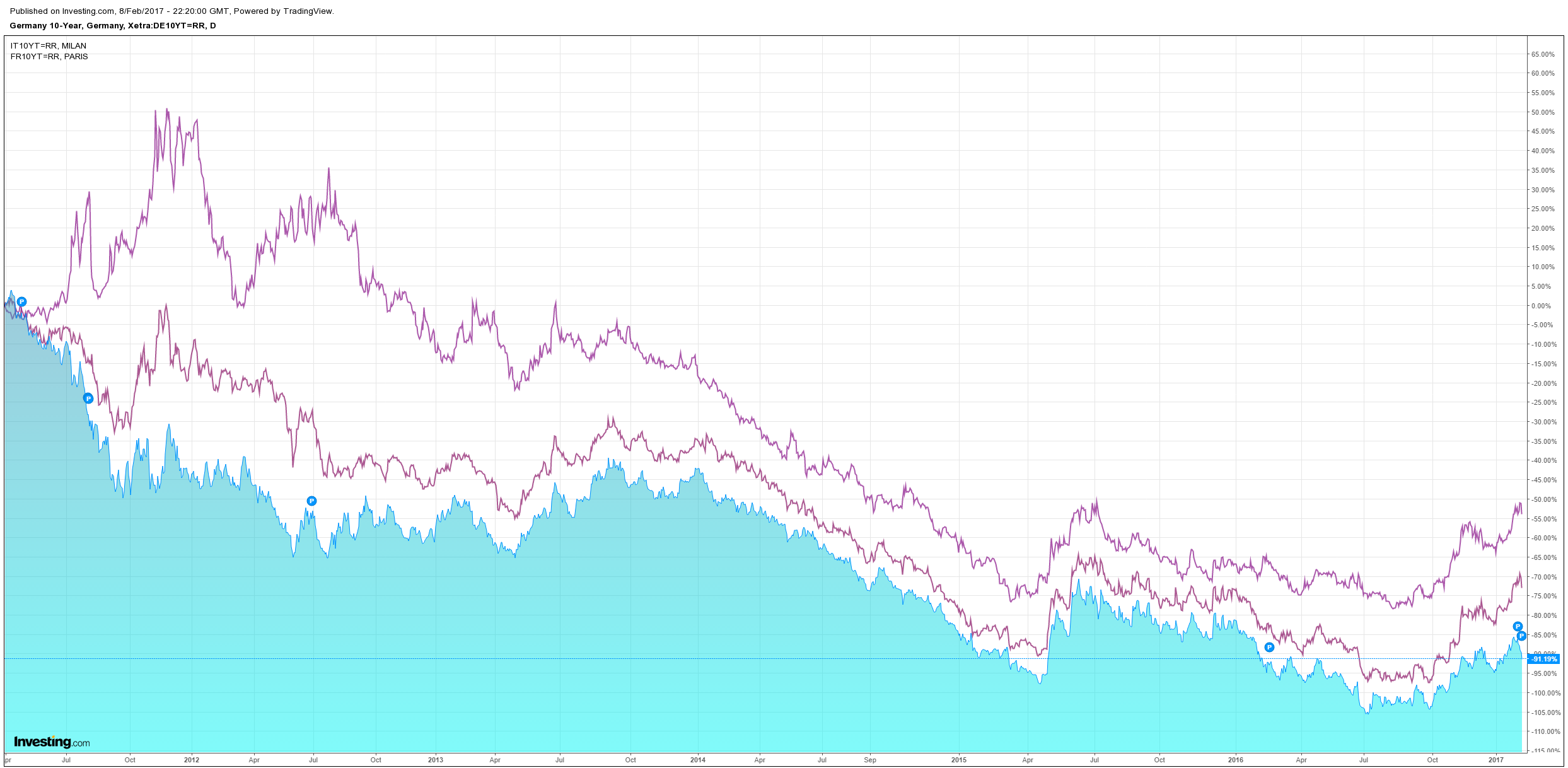

European spreads widened:

Aussie bond yields look ready to tighten further:

Stocks are at the peak but struggling to push on:

So much for the “bondcano”. With oil losing traction (and in my view likely to correct here as US shale storms back) plus European elections in the pipe, Chinese slowing coming and Trump risks plaguing minds, the bondcano is no such thing. Don’t get me wrong, I expect a resumption of selling in US Treasuries as Trump policies are enacted but Europe is still weak with an inflation pulse completely hanging on oil and China is going to slow so the Fed will have some breathing space from commodities through the year. I still see two hikes in H2.

Aussie bonds remain a “buy the dip” allocation as our easing cycle is not yet done.