For many years, the Australian Treasury spruiked its Three P’s framework for rising living standards.

Under this framework, we were told that Australia must: 1) boost productivity; 2) raise workforce participation; and 3) increase the population via skilled migration, if the nation was to continue to enjoy rising living standards.

Personally, I never subscribed to the three P’s framework and preferred that it was pared back to the “Two Ps” of productivity and participation.

Of the three P’s, boosting productivity is by far the most important driver of rising living standards over the long-term, since it allows more goods/services to be produced (consumed) from less effort.

Raising labour force participation can also raise living standards. However, working more hours (increasing participation) can mean that less time is available for other pursuits, such as relaxing or meeting-up with friends. So while working more will, other things equal, raise incomes and GDP, it can also take away from the other pleasures in life.

By contrast, population growth’s impact on living standards is highly questionable. While it certainly does raise headline GDP (more inputs equals more outputs), there are grave doubts over whether it raises per capita living standards, while also placing greater pressure on the environment, infrastructure and housing, and Australia’s fixed endowment of mineral resources.

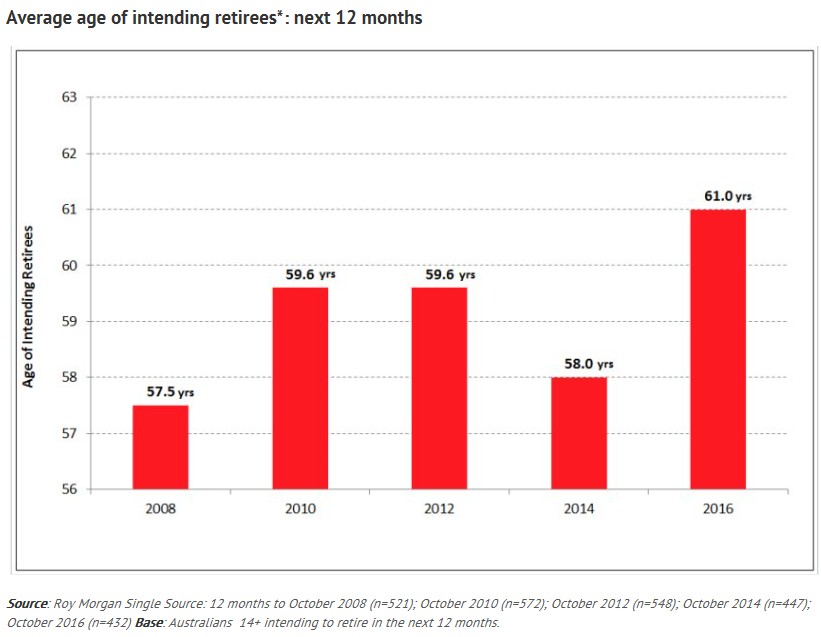

Nevertheless, Roy Morgan Research (RMR) has published results from its latest survey on retirement intentions, which was carried out in the year to October 2016. The survey found that the average age of Australians intending to retire in the next 12 months is 61 years, up significantly from an average of 58 years in the 12 months to October 2014, and 57.5 years in the 12 months to October 2008.

RMR believes that announced changes to pension eligibility and superannuation rules has influenced people’s decision the delay retirement:

As we have seen, recent changes to superannuation rules and pension eligibility appear to be impacting on retirement age, with the result that people will retire later. This is a positive for government retirement funding but could have negative ramifications for unemployment levels.

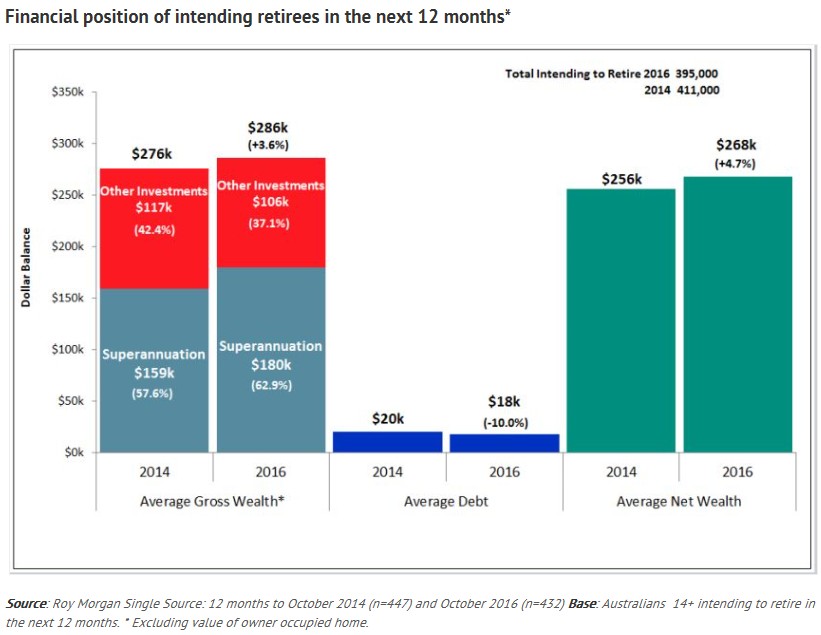

The survey also shows that the average gross wealth (excluding owner-occupied homes) of intending retirees is $286,000, up from $276,000 in 2014. Superannuation is also playing an increasing role in retirement funding, accounting for 62.9% of the gross wealth of intending retirees, up from 57.6% in 2014:

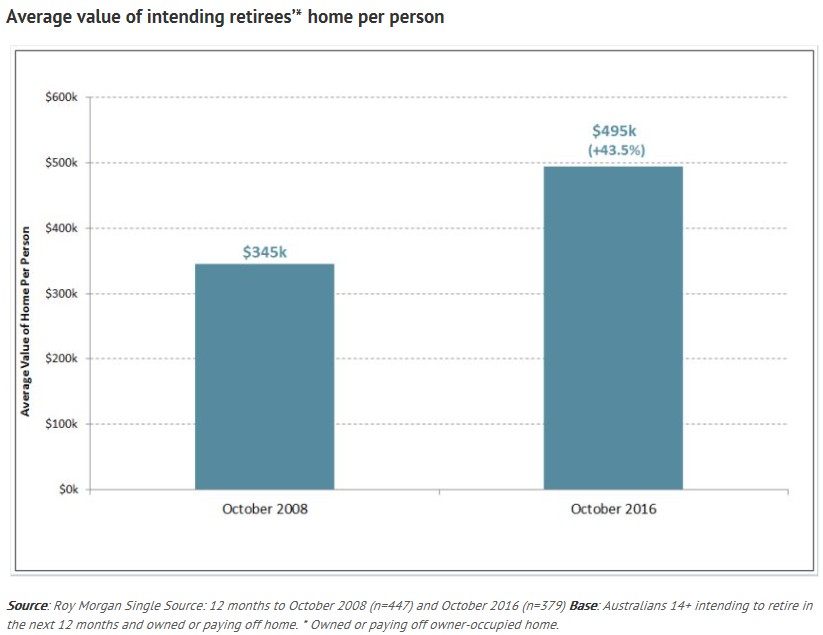

Meanwhile, 85% of intending retirees either own or are paying off their home, with an average value per person of $495,000, or 73% higher than the average ($286,000) in all other retirement funds:

According to RMR:

Although owner-occupied homes are generally not considered to be part of retirement funding, their potential is very significant given their high value compared to retirement savings. Furthermore, they do not impact the age pension asset test…

Not only have owner occupiers got a large potential source of retirement funding but at 43% per person over the last eight years, the growth in the average value of their homes has outstripped that of other investments (23%). Those intending retirees who rent obviously do not have this large potential retirement funding resource but are allowed higher levels of assets for pension eligibility, although the increased limit does not compensate for the higher concessions given to homeowners.

Clearly, the Government’s tighter eligibility for the Aged Pension and reduction of superannuation concessions is a winner from a policy perspective. Not only will they help to raise much-needed Budget revenue and improve fairness, but they have also encouraged greater labour force participation at the margin by delaying retirement.

Further budget/economic/equity gains could be made by bringing one’s principle place of residence into the assets test for the Aged Pension, in combination with associated reforms, as articulated on this site ad nauseum (most recently here).