Bill Gross seems to think so, from his January outlook:

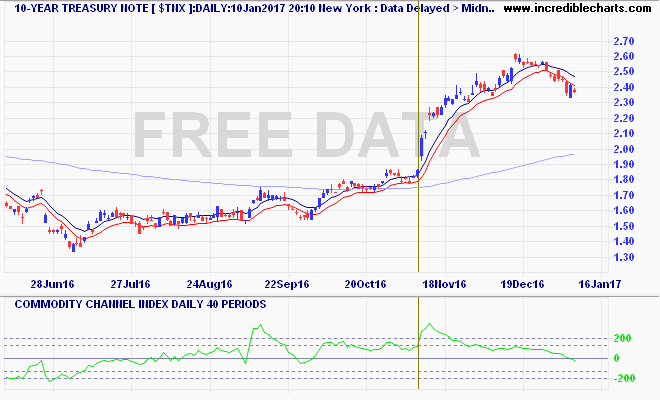

Happiness has dominated risk markets since early November and despair has characterized global bond markets. Hope for stronger growth via Republican fiscal progress/reduced regulation/and tax reform have encouraged risk. The potential for higher inflation and a more hawkish Federal Reserve lie behind the 100 basis point move in the 10-year Treasury from 1.40% to 2.40% over the same time period.

President-elect Trump tweets and markets listen for now, but ultimately their value is dependent on a jump step move from the 2% real GDP growth rate of the past 10 years to a 3%-plus annual advance. 3% growth rates historically have propelled corporate profits to a somewhat higher clip because of financial and operating leverage dependent on higher growth. 2% or less typically has smothered corporate profits.The 1% difference between 2 and 3 is therefore critical. We shall see whether Republican/Trumpian orthodoxy can stimulate an economy that in some ways is at full capacity already. To do so would require a significant advance in investment spending which up until now has taken a backseat to corporate stock buybacks and merger/acquisition related uses of cash flow.

Gross is right to point out that the macro picture is confused and uncertain, whereas the technical picture provides more clarity.

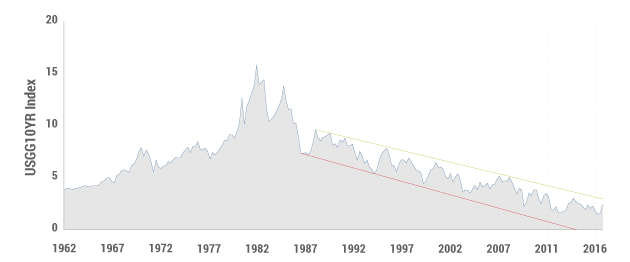

Shown in the chart below, it’s obvious to most observers that 10-year yields have been moving downward since their secular peak in the early 1980s, and at a rather linear rate.30 basis point declines on average for the past 30 years have lowered the 10-year from 10% in 1987 to the current 2.40%.

Now, however this super strong, frequently tested downward trend line is at risk of being broken. 2.55% to 2.60% is the current “top” of this trend line, and over the past few weeks it has held and reversed lower by 15 basis points or so.

If 2.60% is broken on the upside – if yields move higher than 2.60% – a secular bear bond market has begun. Watch the 2.6% level. Much more important than Dow 20,000. Much more important than $60-a-barrel oil. Much more important that the Dollar/Euro parity at 1.00. It is the key to interest rate levels and perhaps stock price levels in 2017.

As does Jeffrey Gundlach – from Bloomberg:

“Almost for sure we’re going to take a look at 3 percent on the 10-year during 2017,” Gundlach, the chief executive officer of DoubleLine Capital, said Tuesday during his annual “Just Markets” webcast from New York. “And if we take out 3 percent in 2017, it’s bye-bye bond bull market. Rest in peace.”

“The last line in the sand is 3 percent on the 10-year,” Gundlach said. “That will define the end of the bond bull market from a classic-chart perspective, not 2.60.”

Trump’s election and his tax-reform policies have fueled rising confidence among corporate executives, small-business owners and consumers, raising the prospect that economic growth can reach 3 percent, compared with the steady rate of about 2 percent in recent years, Gundlach said.

The technical levels to choose from are probably more about where Gross and Gundlach differ on their own risk timeframes, as 3% equates to the five year cycle and the 2.6% rate to the one to two year cycle, or the Presidential honeymoon (or golden shower) period.

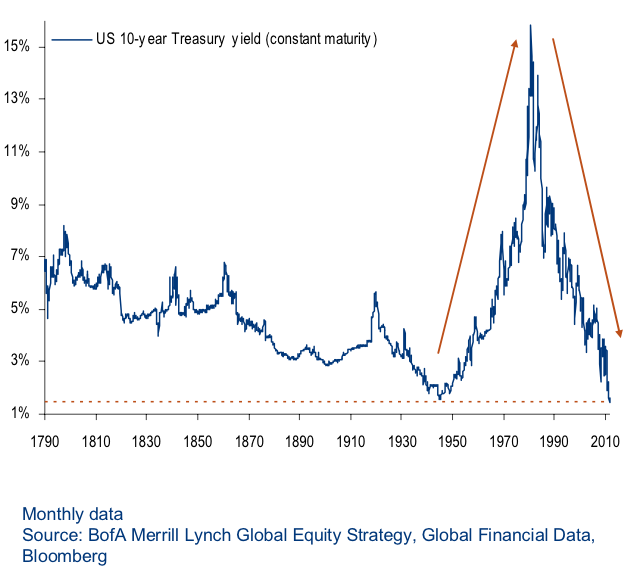

Whatever the case, when risk managers are dumping bonds and inflation is on the cards, stocks are the automatic go-to as the inflation “hedge”. The last time this happened was the post WW2 bond bear market where yields soared from 2% to over 15%:

The missing part of this puzzle is that bond bear market was presaged by a huge change in the global currency system, and for now with the currency war in Europe and Japan bypassed, and the battle over China not yet over, there’s no change to King Dollar on the horizon.