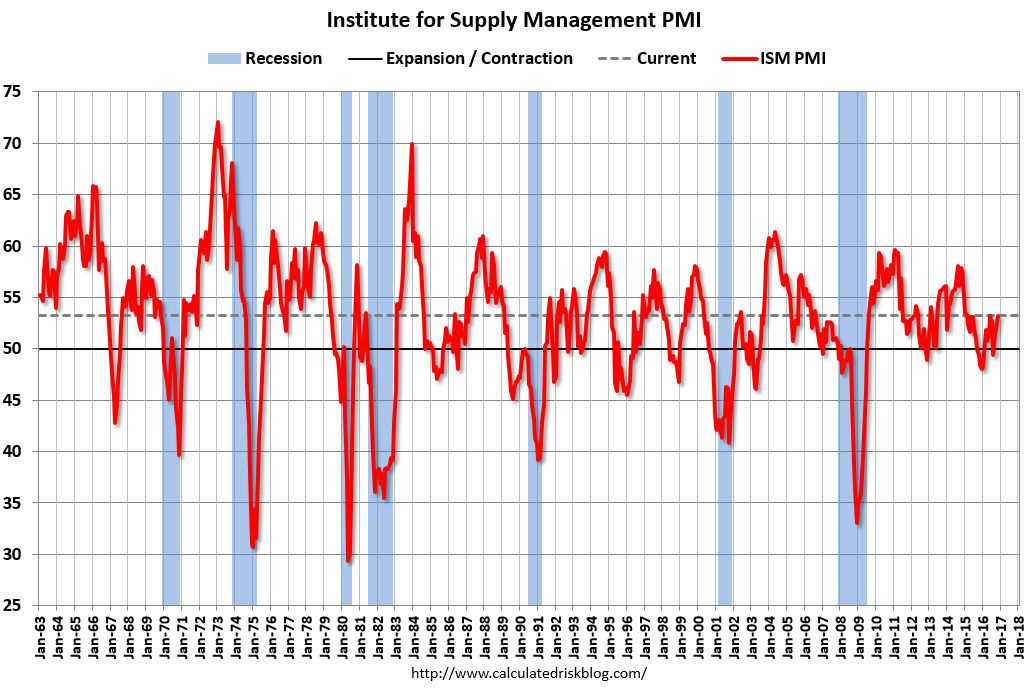

The report was issued today by Bradley J. Holcomb, CPSM, CPSD, chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee. “The November PMI® registered 53.2 percent, an increase of 1.3 percentage points from the October reading of 51.9 percent. The New Orders Index registered 53 percent, an increase of 0.9 percentage point from the October reading of 52.1 percent. The Production Index registered 56 percent, 1.4 percentage points higher than the October reading of 54.6 percent. The Employment Index registered 52.3 percent, a decrease of 0.6 percentage point from the October reading of 52.9 percent. Inventories of raw materials registered 49 percent, an increase of 1.5 percentage points from the October reading of 47.5 percent. The Prices Index registered 54.5 percent in November, the same reading as in October, indicating higher raw materials prices for the ninth consecutive month. Comments from the panel cite increasing demand, some tightness in the labor market and plans to reduce inventory by the end of the year.”

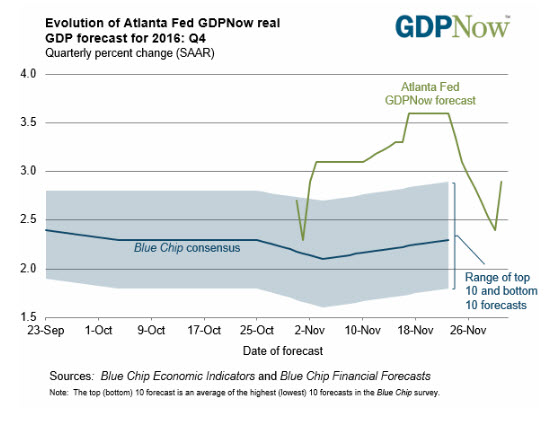

GDPNow jumped:

Advertisement

“The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2016 is 2.9 percent on December 1, up from 2.4 percent on November 30. After this morning’s construction spending report from the U.S. Census Bureau, the forecasts of fourth-quarter real residential investment growth and real government spending growth increased from 7.1 percent to 12.4 percent and 0.1 to 0.6 percent, respectively. The forecast of real nonresidential structures investment growth fell from 1.4 percent to -3.4 percent after the same report. The forecasts of real consumer spending growth and real nonresidential equipment investment growth increased from 2.2 percent to 2.5 percent and 4.6 to 6.6 percent, respectively, after this morning’s Manufacturing ISM Report on Business from the Institute of Supply Management and the incorporation of earlier released November data in the model’s estimate of its dynamic economic activity factor. The factor is used to forecast yet-to-be released monthly source data for GDP.”

The strong U.S. stock market rally, surge in Treasury yields and strength in the U.S. dollar since Trump’s surprising presidential victory more than three weeks ago look to be “losing steam,” Gundlach, who oversees more than $106 billion at Los Angeles-based DoubleLine, said in a telephone interview.

“The bar was so low on Trump to the point people were expecting markets will go down 80 percent and global depression — and now this guy is the Wizard of Oz and so expectations are high,” Gundlach said. “There’s no magic here.”

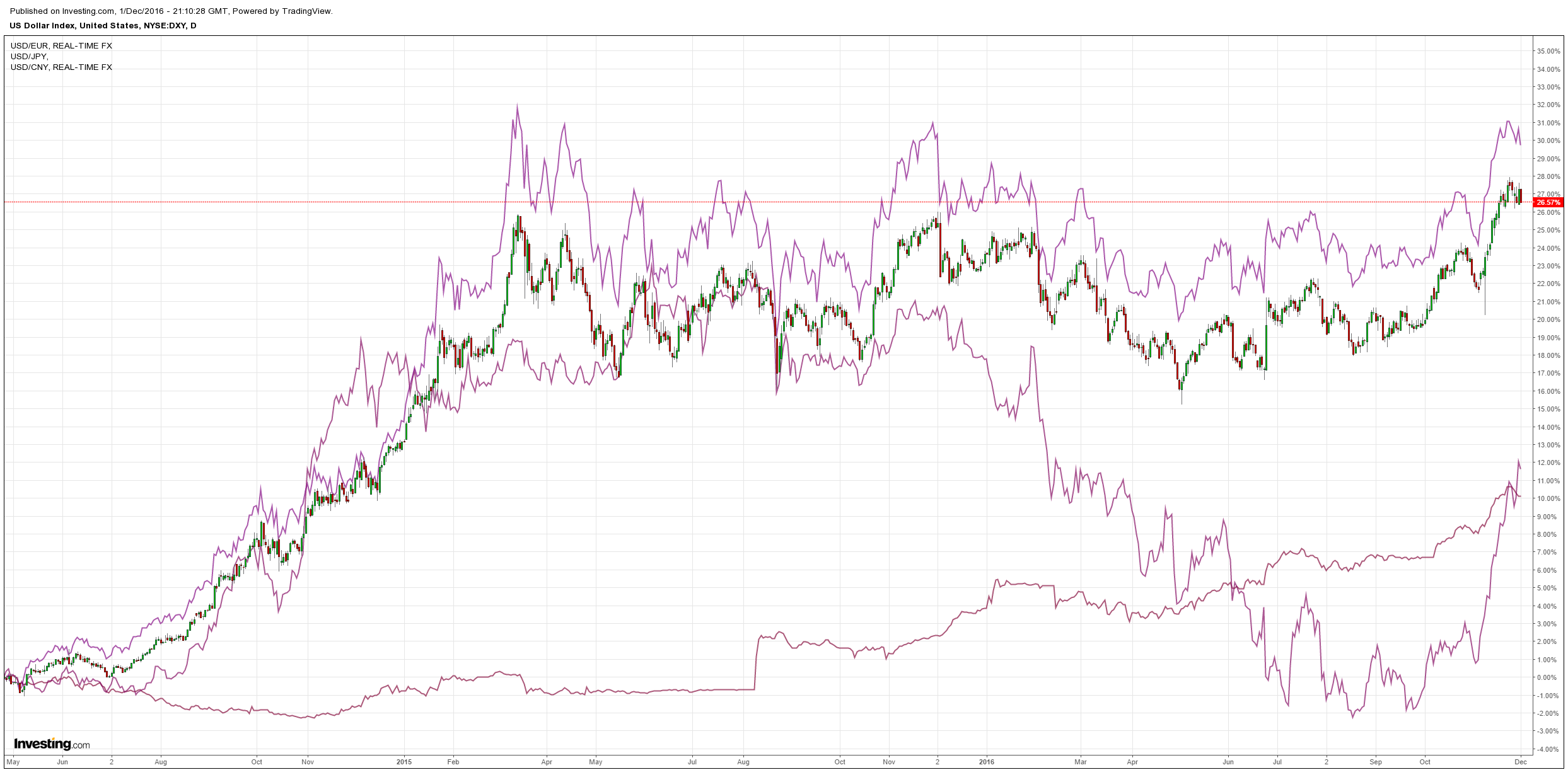

Everything inflation is massively overbought so maybe so. The ECB gave a snap a kick along as well:

Advertisement

The ECB will extend its bond purchases beyond March and consider sending a formal signal after its policy meeting next Thursday that the program will eventually end, senior sources with direct knowledge of discussions said.

Even some skeptics of more stimulus on the bank’s Governing Council have accepted that an extension beyond the current expiry date of March is inevitable given weak underlying inflation and heightened political risk, they said.

They are still wrestling with the question of how to structure that extension, however, according to multiple senior sources at the European Central Bank and national central banks.

That gave the euro a lift and hammered bunds. Far too premature for me. It is as much a political question as economic one. ECB tapering amid Italian political chaos and the National Front governing France is hilarious. We’ll be back to 2012 in a snap.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.