The USD roared to new highs last night:

Commodity currencies were whacked:

Gold broke:

Brent was hit:

Base metals are still stalled:

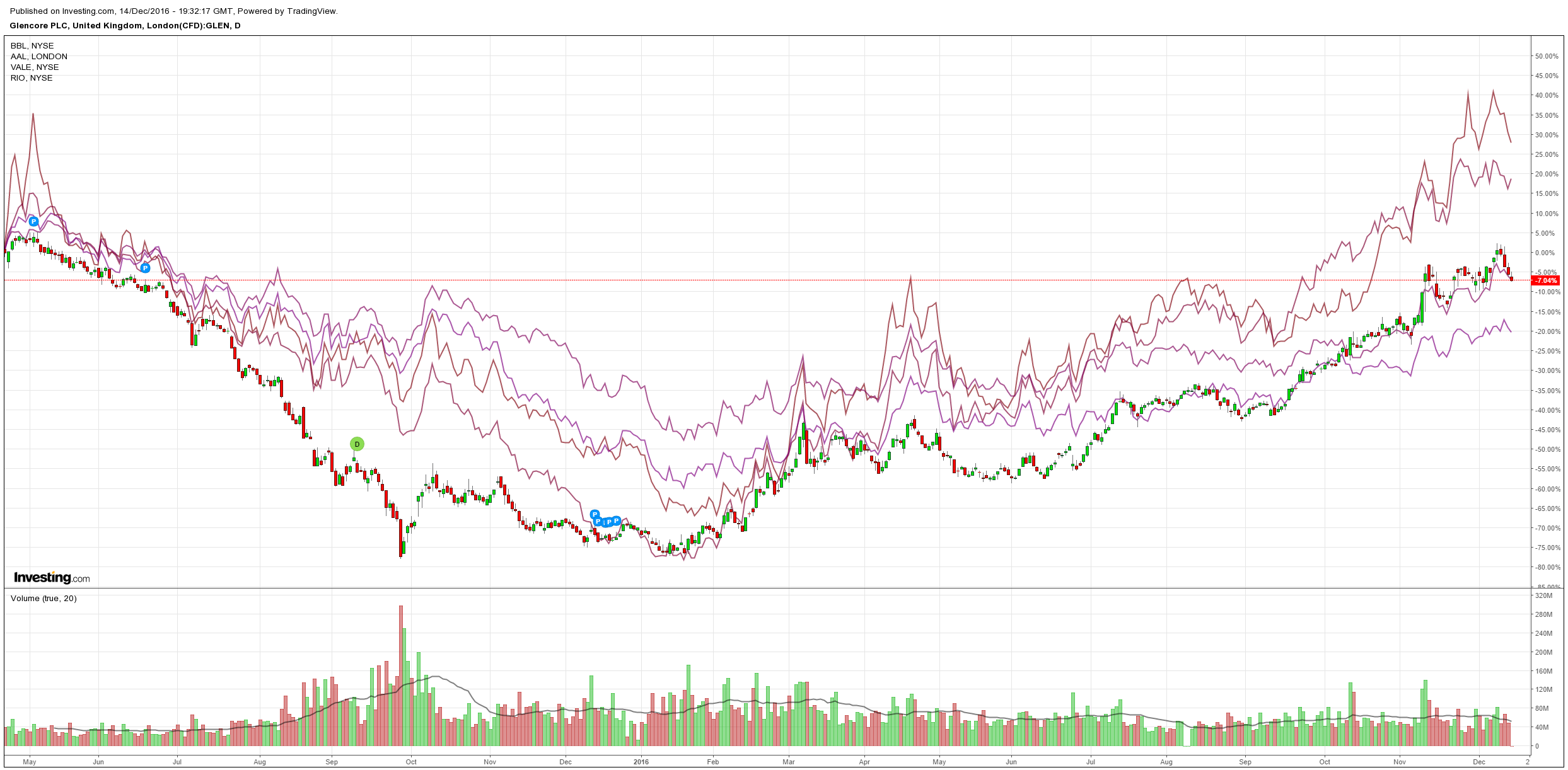

Big miners were hit:

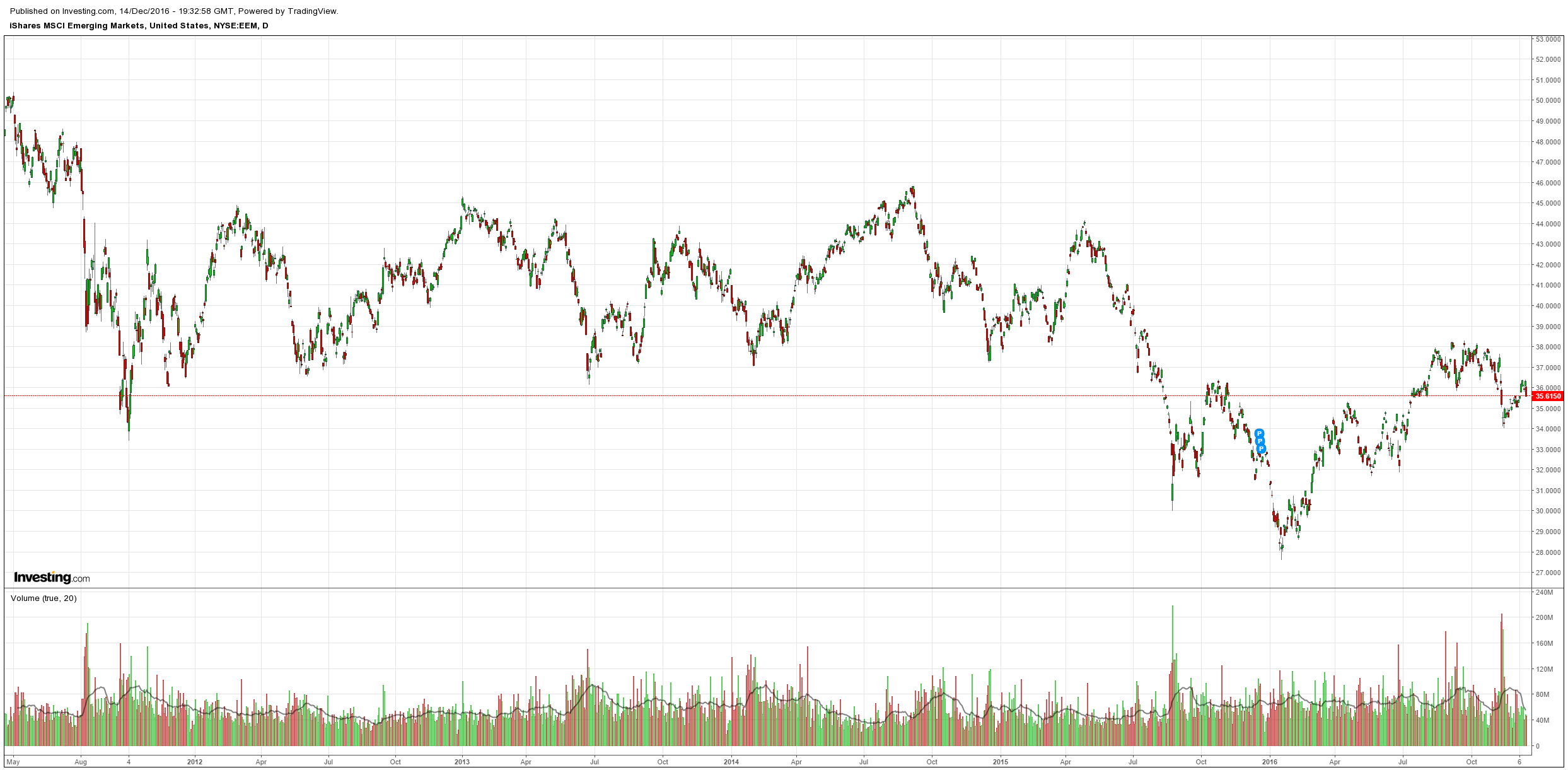

EM stocks caned:

US and EM high yield debt eased:

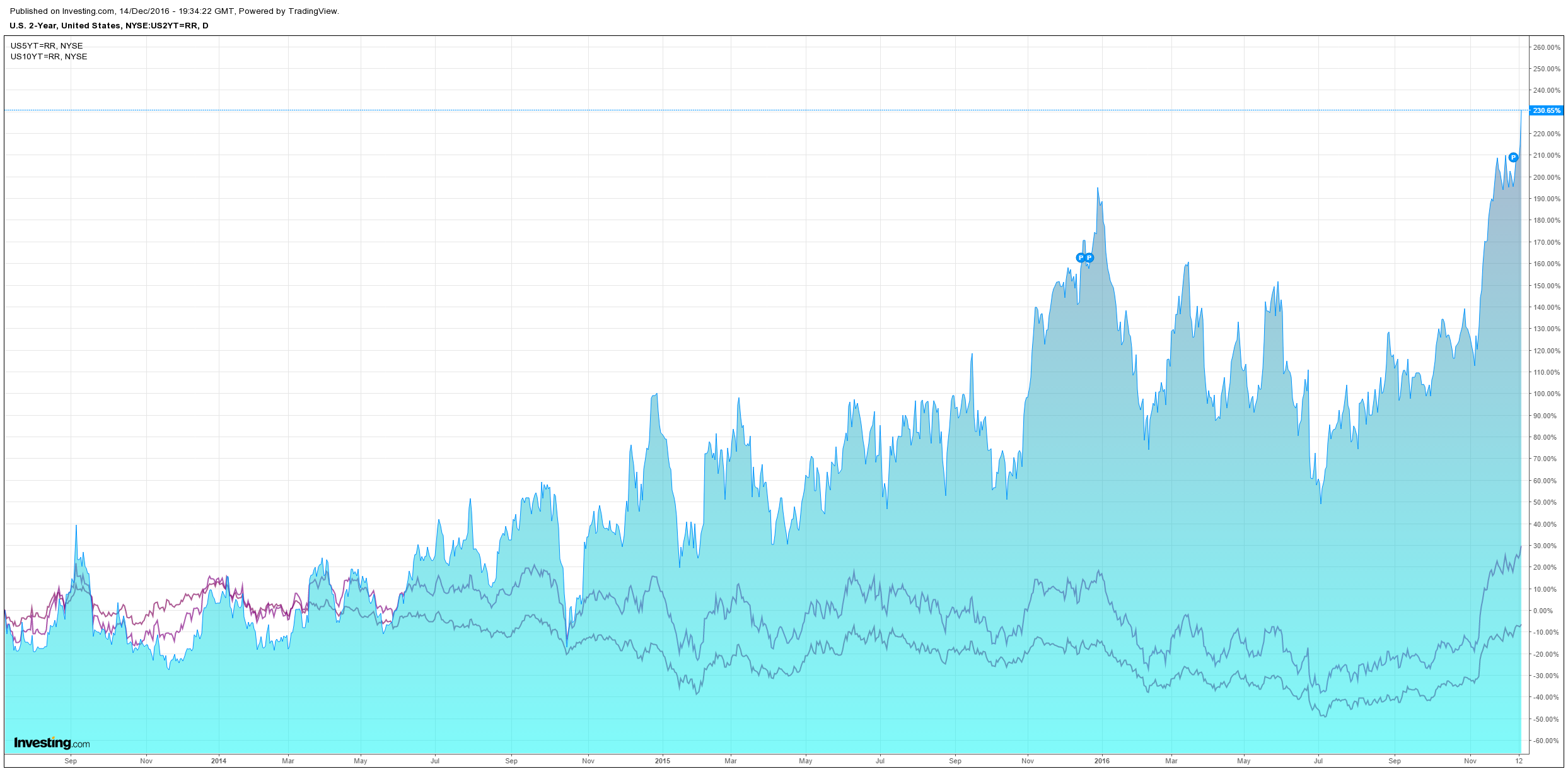

Treasuries got smoked but the curve flattened again:

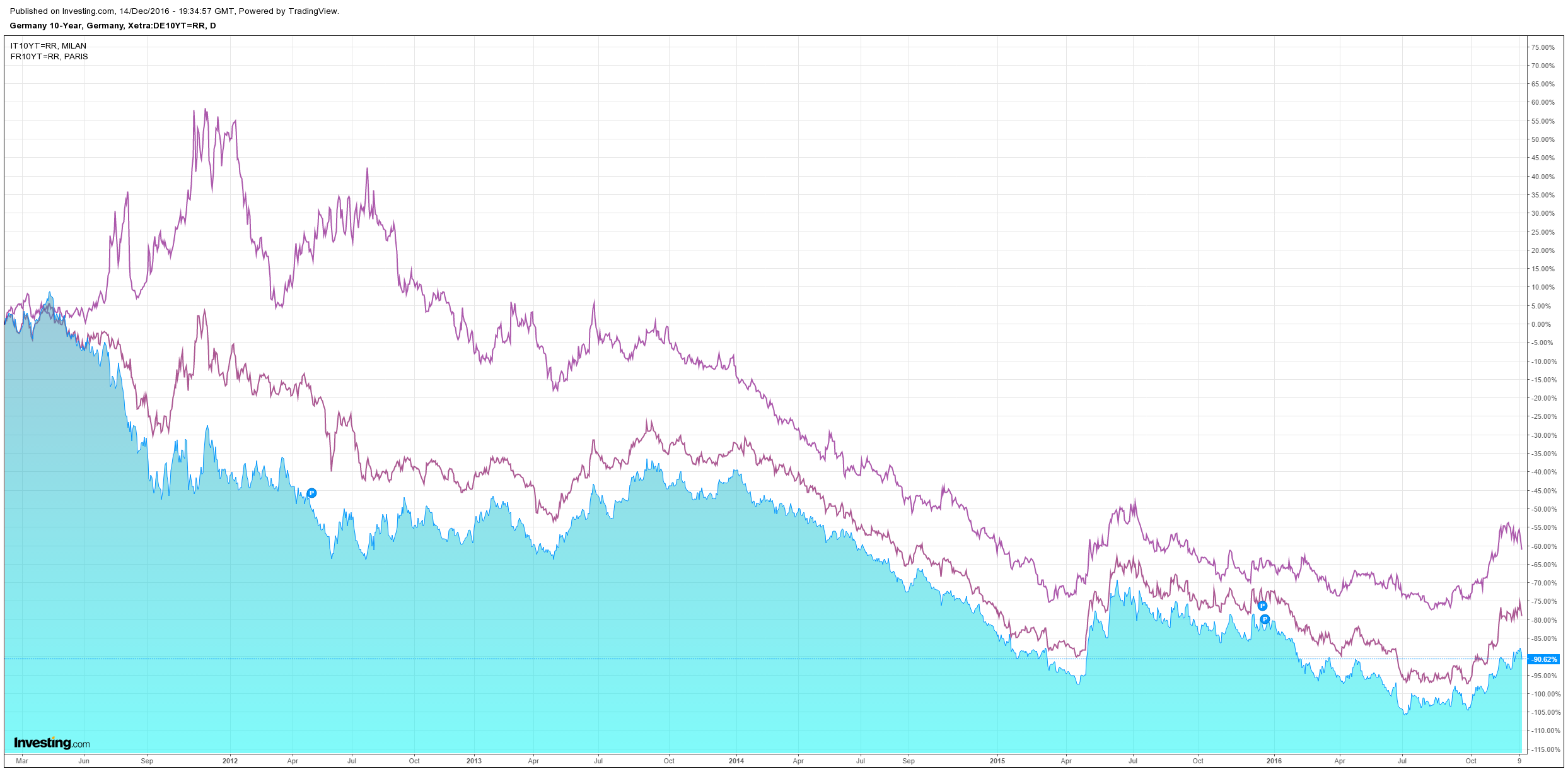

EU spreads tightened:

The S&P500 lost a half percent:

The culprit was not hard to find! The Fed hiked:

Information received since the Federal Open Market Committee met in November indicates that the labor market has continued to strengthen and that economic activity has been expanding at a moderate pace since mid-year. Job gains have been solid in recent months and the unemployment rate has declined. Household spending has been rising moderately but business fixed investment has remained soft. Inflation has increased since earlier this year but is still below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation have moved up considerably but still are low; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will strengthen somewhat further. Inflation is expected to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further. Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments. In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1/2 to 3/4 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

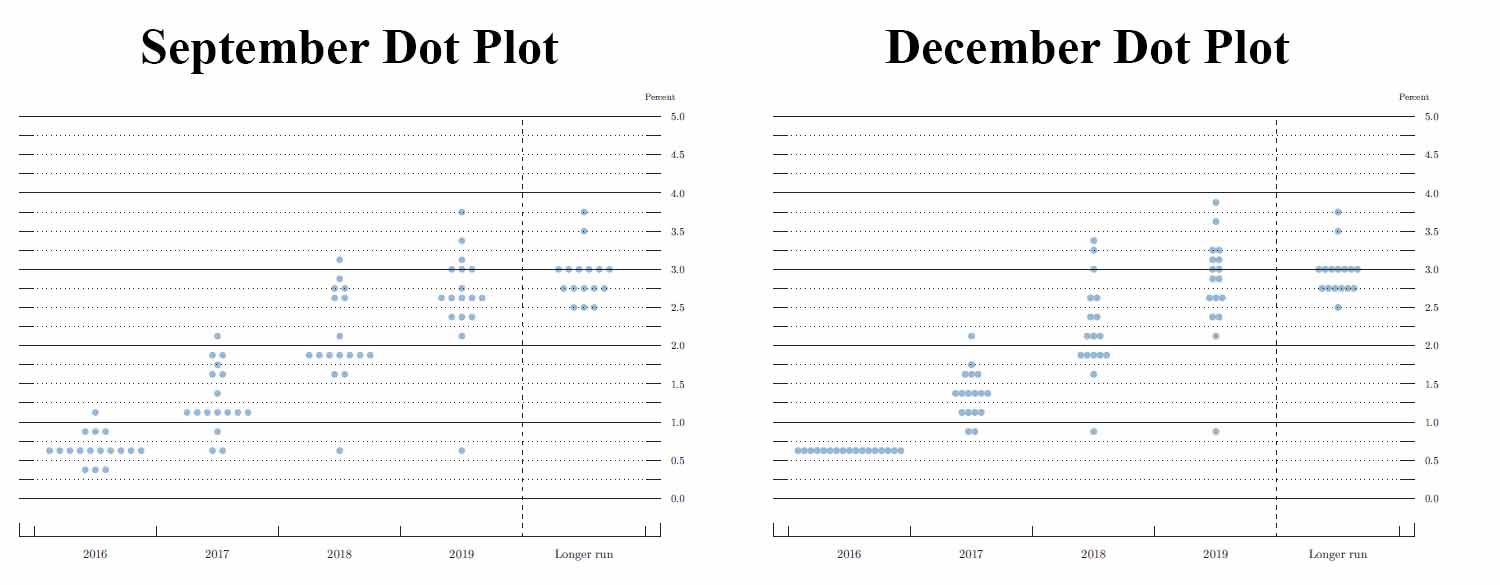

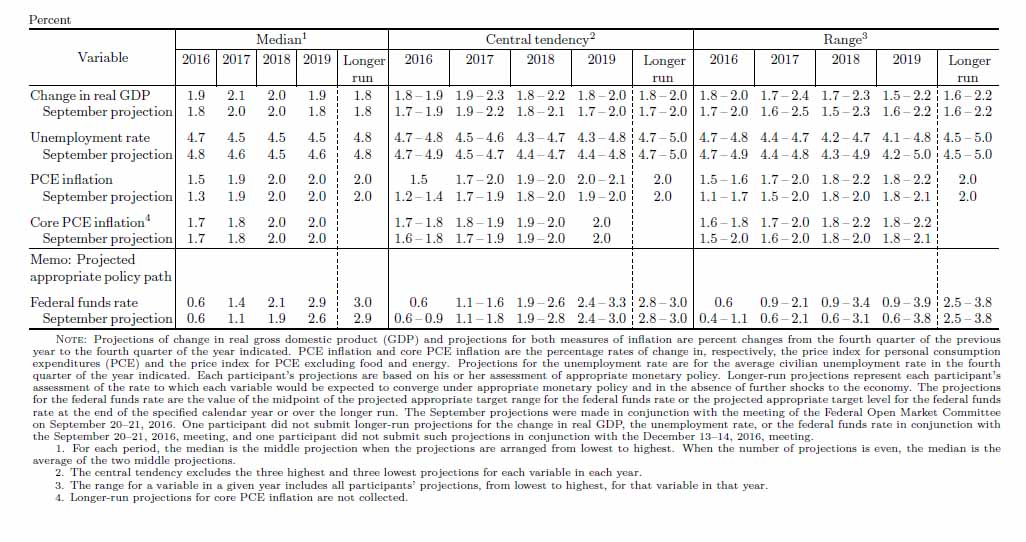

And hawked up in its outlook with three rate hikes now the median view for next year:

Though all other outlooks were unchanged:

From Goldman:

BOTTOM LINE: The FOMC raised the funds rate target range, as widely expected. In the accompanying projection materials, the median estimate of rate hikes for 2017 increased, and now shows three hikes for the year instead of two. The statement said that the committee aims to see only “some” further improvement in labor market conditions.

MAIN POINTS:

1. The FOMC announced an increase in the target rate for the federal funds rate to 0.50-0.75% from 0.25-0.50%, as widely expected. The post-meeting statement indicated that an increase was warranted due to “realized and expected labor market conditions and inflation”. The committee said that the stance of policy remained “accommodative” (rather than “moderately accommodative”, as in Chair Yellen’s recent Congressional testimony), which would help achieve “some further strengthening” in the labor market—with the “some” qualifier added to the statement at this meeting. Elsewhere the statement noted that the economy has been “expanding at a moderate pace”, and noted that inflation expectations in the bond market had increased “considerably”.

2. In the Summary of Economic Projections (SEP), participants made relatively few changes to their economic projections, but some upgraded their projections for the funds rate. The median projections for the funds rate showed three rate increases next year, up from two at the September meeting, with no changes to the number of hikes in 2018 and 2019. Longer-run projections for the funds rate also edged up, with the median rising to 3.0% from 2.9% previously. Elsewhere, the SEP showed slightly higher growth and headline inflation and lower unemployment for this year and also slightly higher growth and a lower unemployment rate for 2017. With a stable long-run unemployment rate but lower unemployment rate projections in 2017 and 2019, the higher projected pace of hikes next year may reflect the committee’s assessment that the economy is close to full employment.

Welcome to the Trump tightening!