Buy everything continues. The USD was up, other majors down:

Commodity currencies were up:

Gold is still struggling:

Advertisement

Brent consolidating, gas flying:

Base metals have stalled for now:

Big miners haven’t!

Advertisement

EM stocks joined the party:

As EM and US high yield was bought:

US bonds were sold a touch:

Advertisement

As were European:

And stocks are headed for the sky:

Better growth and Trump stimulus! So good, in fact, that a little ECB tapering couldn’t even dent the mood, via FT:

Advertisement

Until Ben Bernanke mentioned it, tapering was a word rarely heard outside barber shops. The former US Federal Reserve chairman coined the term to describe a slowing of his central bank’s asset purchases. It sounded neat, but it roiled global financial markets hooked on large-scale bond-buying and threw the Fed off course.

No wonder Mario Draghi was insistent that scaling back asset purchases by the European Central Bank was different. There was “no question” the ECB was tapering, the ECB chief said, “ . . . as a matter of fact, it’s not even been on the table”.

The market reaction suggested not all investors bought Mr Draghi’s line, however, with many interpreting the ECB’s decision to reduce the rate of purchasing from the €80bn a month it has promised to undertake until March to €60bn as the tapering of its quantitative easing programme.

The risk to the bank now is that the work done by QE in securing cheap and easy access to credit to businesses and households right across the eurozone goes into reverse.

While an initial rout was calmed by his remarks, governments’ borrowing costs rose across the region, especially in parts of its more troubled periphery such as Portugal. If those movements persist, interest rates charged by lenders in weaker parts of the eurozone are likely to rise too.

“It’s the Nike version of tapering. Don’t say it, just do it,” said Richard Barwell, an economist at BNP Paribas Investment Partners. “The bottom line is that the pace of purchases has been cut and the central bank did not make major changes to create space for massive purchases in the future. Indeed, Draghi hinted the programme may be running up against legal constraints.”

It’s an exuberant market now going long reflation having come through the Q4 risk gauntlet unscathed. What will pull it up I have no idea.

But pull up it very likely will. For 2017 a number of key risks present themselves:

Advertisement

China’s housing pulse and commodity rebound is going to slow. I expect bulk commodity prices especially to roll and that should pull down industrial metals as well;

Europe still faces its deglobalisation reckoning. The election gauntlet remains formidable and the UK is going to trigger Article 50;

Trump stimulus is not going to arrive until late 2017 though the Fed will keep tightening if markets do not stop. From Goldman:

The Trump Administration appears likely to focus on infrastructure among several competing priorities, and we have penciled in $25 billion per year into our forecast to account for this. We expect very little of this spending to show up in 2017, for three reasons.

First, it is not clear how the legislative process for infrastructure will unfold over the coming year, but it seems unlikely to us that legislation establishing a new program would be enacted into law before mid-year.

Second, it is unclear what channel new funding would run through, but a new financing scheme involving tax credits, tax-preferred debt, loan guarantees, or other mechanisms to incentivize public-private partnerships seems most likely.

Third, it takes time for contracts to turn into spending. Exhibit 2 shows the timing of “obligations” of transportation-related infrastructure funding following enactment of ARRA, and the timing of the actual spending that resulted from those contracts.

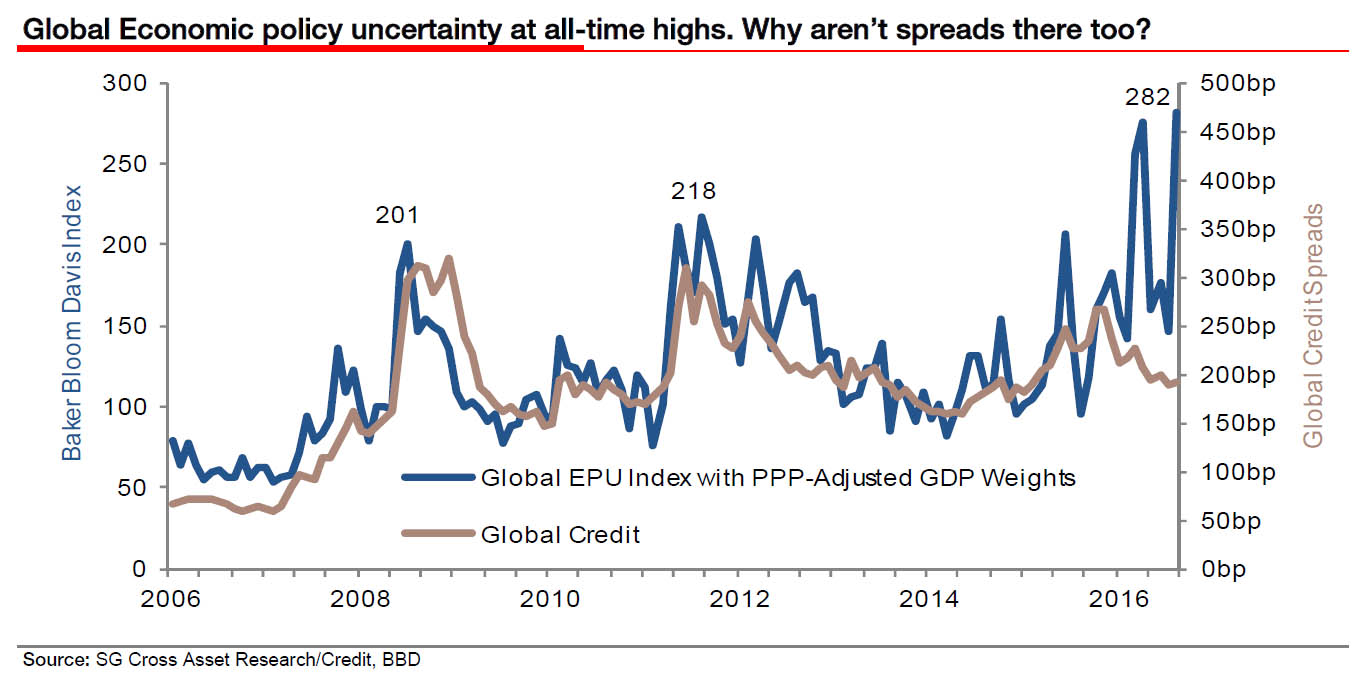

These risks are, for now, forgotten as Soc Gen point out today:

Advertisement

“I sometimes feel like ‘The Grim Reaper’, scouring the research savannah in a ghoulish quest to harvest bad news with a forceful sweep of my scythe. Imagine then my perverse delight when our credit team produced what is one of the scariest charts I have seen for a very long time. Markets shrugged off the Brexit vote in a couple of days. They shrugged off Donald Trump’s election in a single day. They shrugged off the Italian Referendum result in a couple of hours. Heck, in this mood they would shrug off an alien invasion of planet Earth. But global political risk is now at such elevated levels that investors must surely be on another planet.”

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.