Earlier this month, researchers at the Swinburne Institute for Social Research released a new report entitled Security in retirement: the impact of housing and key critical life events, which found that renting pensioners are doing it tough, with the situation likely to worsen over the decades ahead:

An increasing number of older people in Australia are experiencing housing insecurity and impoverishment in retirement. Overwhelmingly these are lone person households living in private rental. A lone person renter paying market rent on a one bedroom dwelling in Melbourne will have after housing income of $9,635 pa and a couple $10,540pa.

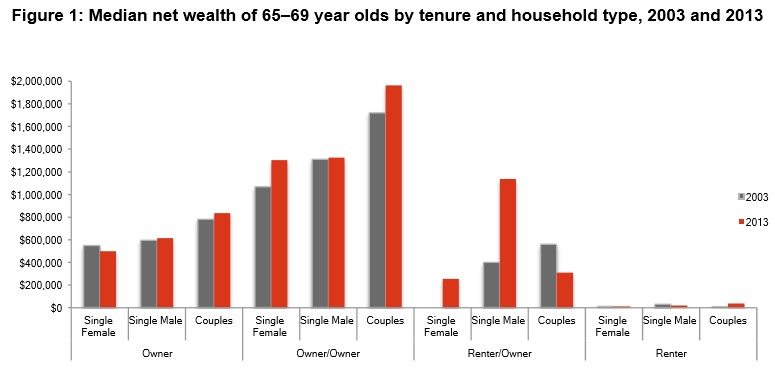

Retired lone person and couple-only renters have little wealth and women tend to be somewhat poorer than men. The median net total wealth for single female private Renters in 2013 was $14,025 and $18,900 for single males (Figure 1)…

University of Technology Sydney Institute for Public Policy and Governance research professor, Alan Morris, has launched a new book warning that at least 100,000 older Australians in the private rental sector are living in “dire circumstances” across the country, due to a lack of rental security and untenable rent increases. From All Homes:

“Those older Australians renting privately are often struggling to purchase necessities and running out of money for food before the next pension payout”…

Tenants Union of NSW project manager for older tenants Robert Mowbray warned there was likely to be an increase in those facing “immense hardship” if the government didn’t take action.

He recommended the Federal Government challenged speculation in real estate by “mum and dad investors” by tackling tax incentives, such as negative gearing, and instead look to incentivise institutional investors.

“If we leave the private rental market like it is, we’ll see more people pushed into an unaffordable sector where stress will take over their lives,” he said.

Advertisement

These findings argue for broad reforms to both the housing and the Aged Pension systems.

On the housing side of the equation, there is a clear need for greater public investment in social and community housing, as well as reforms to taxation arrangements to boost affordable housing via targeting negative gearing at new builds (similar to Labor’s policy). We also need rules that give greater security of tenure to renters, like those that exist across much of Europe.

Regarding the Aged Pension, it should be reformed to provide less taxpayer assistance to wealthy home owners and more assistance to renters, via:

Advertisement

Including one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

Once implemented, raising the overall assets test for the Aged Pension, and the base rate as well.

Extending the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HELP-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under this plan, house-rich pensioners could continue to receive a regular income stream as they do now under the Aged Pension, but with less longer-term drain on the Budget and on younger taxpayers. At the same time, the 25% of renting pensioners (see below) would receive greater financial assistance – both via and expansion of the assets test and an increase in the base rate (see here for a detailed examination of this issue).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.