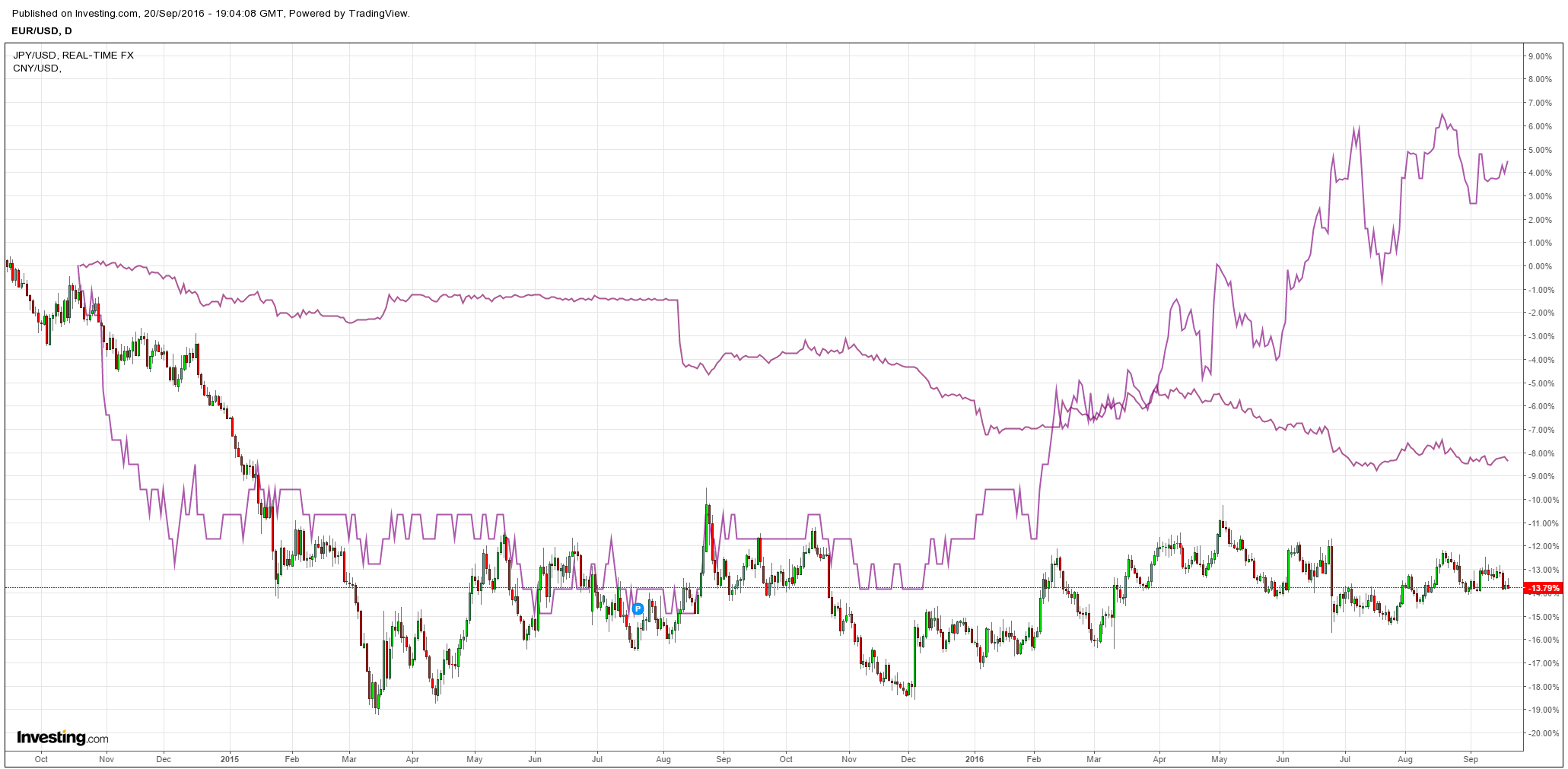

There’s a bewildering series of risks bearing down on markets and, to be honest, there’s absolutely no saying where it will all end up. Markets themselves are telling us nothing. The US dollar is still strong:

Other majors sideways:

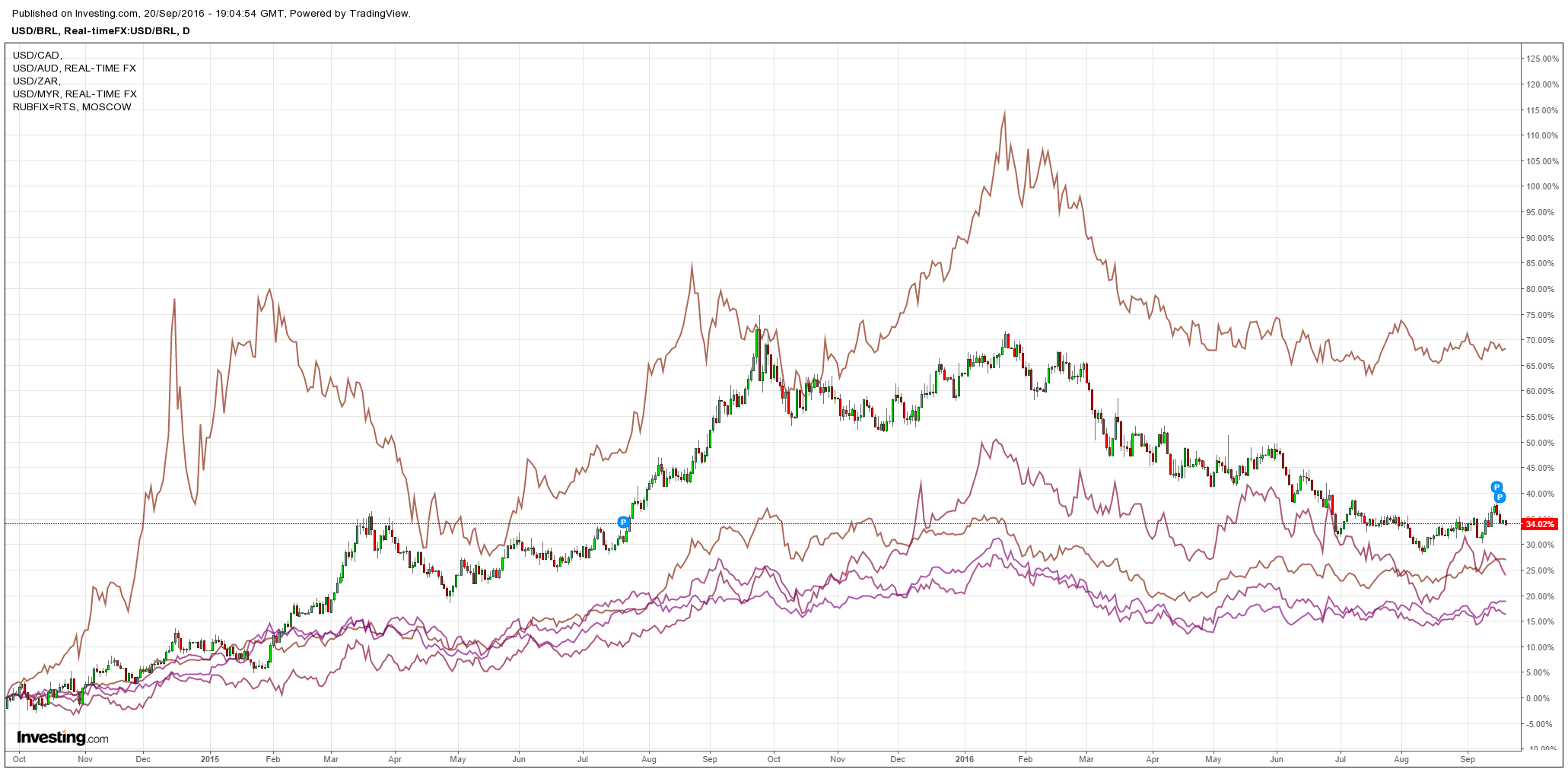

Commodity currencies range bound:

Advertisement

Gold still weakish:

Oil hit new lows but held on:

Base metals are liking the Chinese property bubble:

Advertisement

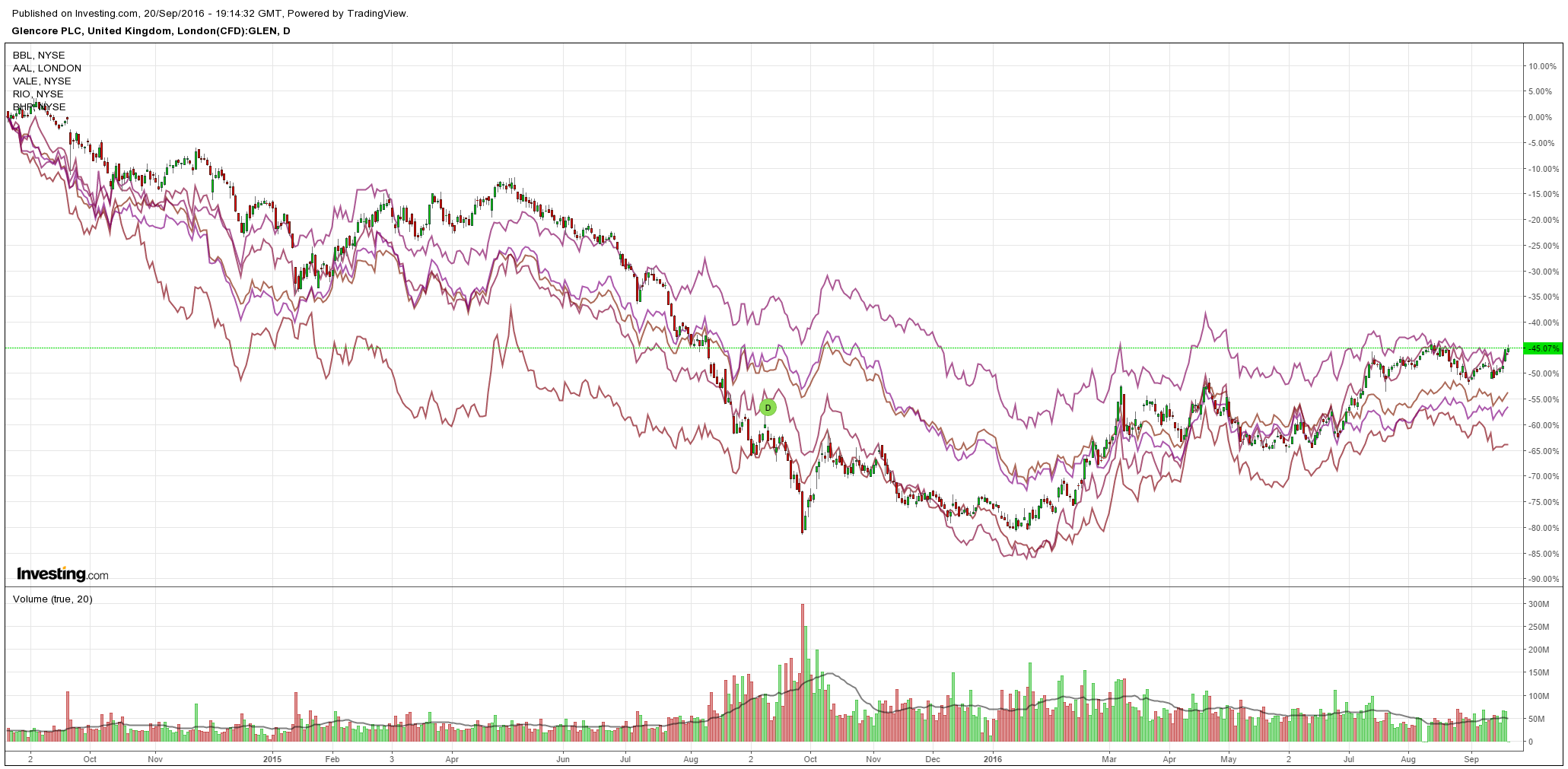

Big miners were mixed:

EM and US high yield has stalled:

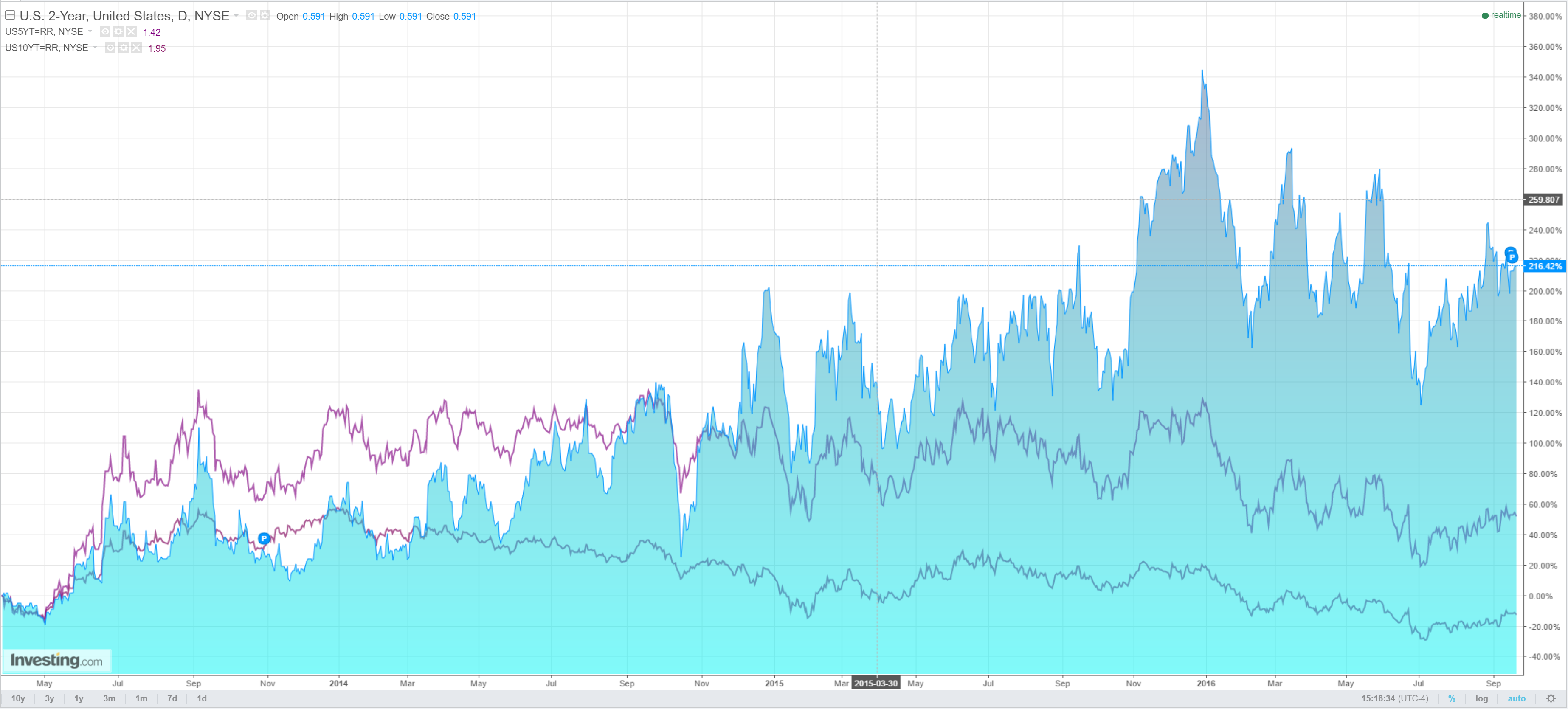

US yields too:

Advertisement

And shares:

It’s a waiting game and why not? Let’s describe the risks. First, the Fed meets today. It seems very determined to tighten and GDPNow is still at 2.9% for Q3 so if it is going to do it it should do it now. But WSJ’s Jon Hilsenrath says December. I can’t gainsay that but reckon, if so, it won’t happen at all.

Next is the Bank of Japan, also meeting as we speak, here’s Nomura:

Advertisement

BOJ’s “comprehensive assessment”—the key points

The Bank of Japan (BOJ) plans to carry out a “comprehensive assessment” of its monetary policy at the monetary policy meeting scheduled for 20-21 September. We expect this assessment to focus mainly on two key areas: (A) how well its monetary policies haves functioned up to now, and what has hindered the achievement of the 2% price stability target, and (B) the positive effects and negative side-effects of its quantitative and qualitative easing policy with a negative interest rate (QQEN).

We have now formed an overall picture of what the “comprehensive assessment” is likely to entail

With respect to (A), we think the BOJ will conclude that the main reason for the failure to achieve the 2% price stability target is that inflation expectations have not risen as it expected, and also expect it to note uncertainty about future price movements. With regard to (B), we think it will say that the positive effects of QQEN outweigh the negative side-effects, but will also point out the need to pay attention to these sideeffects. One possible side-effect of QQEN is that the flattening of the yield curve and the fall in long-term and superlong interest rates might have a negative impact on the financial intermediation function.

Policy implications of the outcome of the “comprehensive assessment”

In our view, two possible policy implications from the outcome of the “comprehensive assessment” are that it will (a) highlight the relative effectiveness of a deepening of negative interest rates and (b) lead to a greater awareness of the need to deal with the negative side-effects of QQEN.

A deepening of negative interest rates looks likely, but we do not expect a rate cut in September

We think a consensus is likely to form within the BOJ for a deepening of negative interest rates. However, we regard an interest rate cut in September as unlikely. The BOJ’s negative interest rate policy (NIRP) has come under a lot of criticism, particularly from the financial sector, and we therefore think that the BOJ will aim to deepen negative interest rates only very gradually.

One way of mitigating the side-effects of QQEN would be to remove the rule limiting the average remaining maturity of its long-term JGB purchases

In terms of measures aimed at dealing with the negative side-effects of QQEN, one option would be for the BOJ to become more flexible about the average remaining maturity, and/or the volume, of its long-term JGB purchases. There is strong resistance among some members of the BOJ’s policy board to an increase in flexibility regarding the volume of these purchases, so we think it highly likely that the board will opt instead for greater flexibility in terms of the average remaining maturity of the long-term JGBs it buys.

Sounds like deck chairs on the Titanic to me and will only add that anything that does reverse the rising yen will comprehensively fail to trigger inflation. But that will take something more radical. Without it the yen will climb on “quantitative failure” and take some marginal pressure off the US dollar. If it does try to steepen the yield curve then that will play into a further global bond yield back-up. In turn, that would combine with and intensify the review underway at the European Central Bank of negative interest rates.

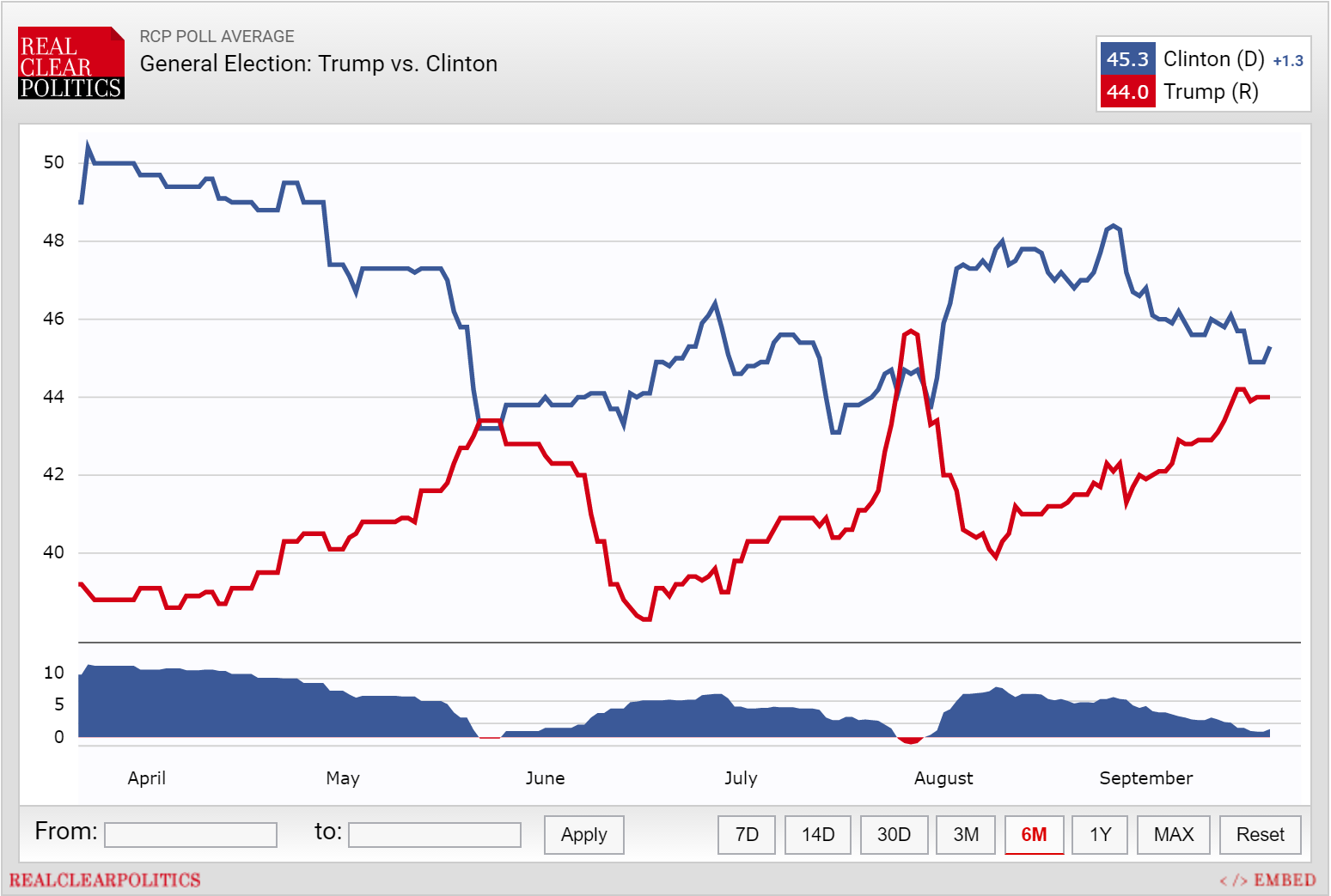

After that we shift to politics and the US election on November 8. Latest polling has a little rebound for Hillary:

Advertisement

My view at this point is that Trump will win but, obviously, that is a guess of the worst kind. If it is Trump then I expect the US dollar to rally and markets to fall in the short term. If it’s Hillary then still a firm US dollar as markets rally.

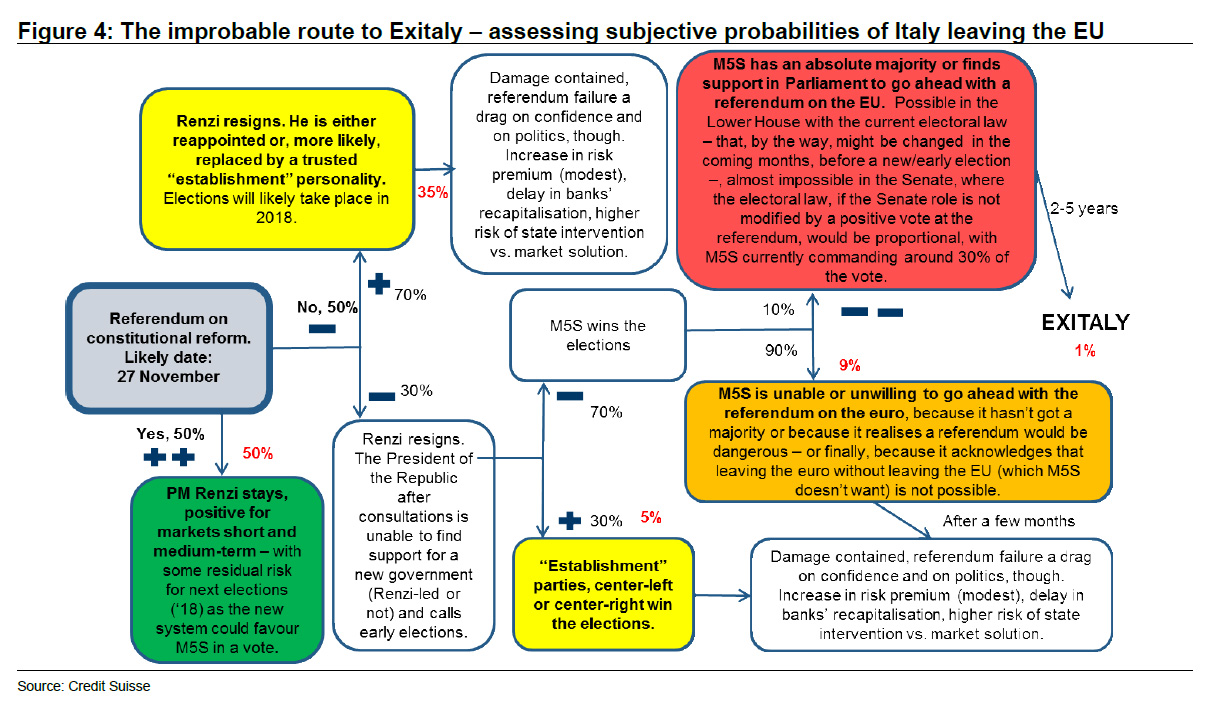

After that comes the next round of European exit problems: the Italian referendum in late November, from Credit Suisse:

Advertisement

…the referendum will allow Italian citizens to approve or reject a bill – already approved by Parliament – that aims to slim down and raise the efficiency of the political system. The bill, if approved, would reduce the number of MPs, essentially cutting from 315 to 100 the number of senators, making the government cheaper to run. More importantly, it would end the perfectly symmetric nature of the Italian parliamentary system, in which both the Senate and the Lower House have equivalent powers – meaning that the Senate can effectively veto the Lower House’s rulings and vice versa. The Senate would retain some control functions, but be essentially the chamber of the local authorities – with no veto power.

The constitutional bill, presented by the government in 2014, went through a double round of parliamentary scrutiny and was approved by an absolute majority, although it fell short of the qualified majority of two-thirds required for it to become immediately current, as Berlusconi’s center-right party, after having supported the reform in its initial phase, decided to withdraw support for motives seemingly unrelated to the bill itself. The constitution requires a confirmatory referendum in that case: as such, the decision to hold a referendum was a legal requirement – a necessity more than a decision of the PM.

Theoretically, a “No” vote would have no consequences for the government, although the prime minister has committed a significant amount of political capital to this specific reform, and would probably be seriously weakened as a consequence. Although it should be easier to get a “Yes” vote in the Italian referendum compared to the Brexit one – given that the question asked is, basically, if one wants to cut the number of MPs and simplify the political system – as often happen with referendums it could morph into a judgement on the overall actions of the government rather than on the question asked.

We think that a “No” vote is a real possibility, which could have negative political, economic and financial consequences for the country – but we also believe that the impact would be contained – and that it would not lead to Italy leaving the euro. The “domino effect” concern – from the constitutional referendum, to early elections, to a referendum on the euro and eventual “Exitaly” – is motivated by the earlier positioning of Renzi, who initially said he would resign and even suggested he would leave politics completely in case of a “No” vote, while also seeming to hint at precipitating early elections in that event. Were M5S to win those elections – and with its stated intention to call a referendum on the euro – that could open the way for “Exitaly” in short order.

We have explained above that some of the dominoes are not in place anyway, as even a victory after a “No” vote would still leave M5S, in all likelihood, short of a majority in the Senate. Over the past few weeks, moreover, Renzi seems to have back-tracked from his original position. He has stopped mentioning his pledge to resign – though not denying it either – and has said that new elections will take place in 2018, as scheduled, whatever happens with the referendum. Moreover, it must be noted that it is contrary to the Italian Constitution (art. 75) to hold a referendum on decisions taken through international treaties, such as the membership of the European Union and the euro area.

Besides, a referendum on the euro would not be possible per se, as leaving the euro but not the EU is impossible, according to the EU Treaty. Again, this would be an issue for M5S, whose leaders have stated they would like to hold a referendum on the euro, but not on the EU – which is an internally inconsistent proposition. Finally, support for the EU has fallen but remains sufficiently high in Italy, meaning that even in the unlikely event of a referendum, “remain” would likely win.

In summary, Credit Suisse believes the Exitaly scenario requires a sequence of unlikely or even internally inconsistent events. Which is why the bank’s subjective assessment of the probabilities leads it to to assign a mere 1% (or less) chance of it happening. Then again, we wonder what CS’ estimate of Brexit odds was.

That is way over-complicating things. If Five Star wins it will be another serious blow to Europe. It may or may not herald Italexit but what it will unquestionably signal is that Brexit was indeed the beginning of the end. Markets are hopeless at discounting political risk, especially dunderheaded equities, so I would not necessarily see any big immediate fallout, but it’s huge for forex given markets would be unable to ignore the possibility of a National Front win in France next year and Fraxit. The zombieuro would surely be hit and the US dollar rise.

Meanwhile, in the background will be Brexit, from Martin Wolf:

Advertisement

Brexit means Brexit.” As circular as it is concise, this three-word sentence tells us much about the style of Theresa May, the UK prime minister. I take this to mean that the UK will, in her view, formally leave the EU, without the option of a second referendum or a parliamentary override. If so, it seems overwhelmingly likely that the outcome will be “hard Brexit”.

By “hard Brexit” I mean a departure not only from the EU but also from the customs union and the single market. The UK should, however, end up with a free-trade arrangement that covers goods and possibly some parts of services and, one hopes, liberal travel arrangements. But the “passporting” of UK-based financial institutions would end and London would cease to be the EU’s unrivalled financial capital. The UK and the EU would also impose controls on their nationals’ ability to work in one another’s economies.

This is not the outcome many desire. As the Japanese government has made brutally clear, many Japanese businesses invested in the UK in the justified belief that the latter would provide a stable base for trade with the rest of the EU on terms as favourable as those available to producers anywhere else. These businesses are understandably worried about their prospects. The same applies to many others whose plans were made on the assumption that the UK had a settled policy of staying inside the EU.

There are no obvious accelerants but Article 50 will intensify, also hollowing out zombieuro sentiment.

Until this week my next risk factor would have been to add a slowing China with certainty. But its housing bubble was so out of control in August that that is now in question. Yet the odds still favour Chinese growth easing into year end. Despite rampant house prices, credit has fallen away materially since April and infrastructure projects have diminished. More are coming but not before growth peters out a little. As well, Chinese prudential tightening on the runaway housing market will ratchet up.

Advertisement

Finally, there is oil, with Libya and Nigeria set for their return, Brent will remain under intense pressure throughout the next six months. OPEC will jawbone it upwards but it is on a hiding to nothing given all that will achieve is to further slow an already stalled US shale shakeout. Oil needs lower prices to clear and in my view is that they are coming. $40 at least and probably lower as OPEC loses its handle on traders. That will choke up US high yield debt markets that fund shale and also hurt fund flows into emerging markets.

Current MB allocations to deal with this briar patch of risks are unchanged:

long cash, bonds (preferably short duration) and gold;

short commodities, equities, property and Australian dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.