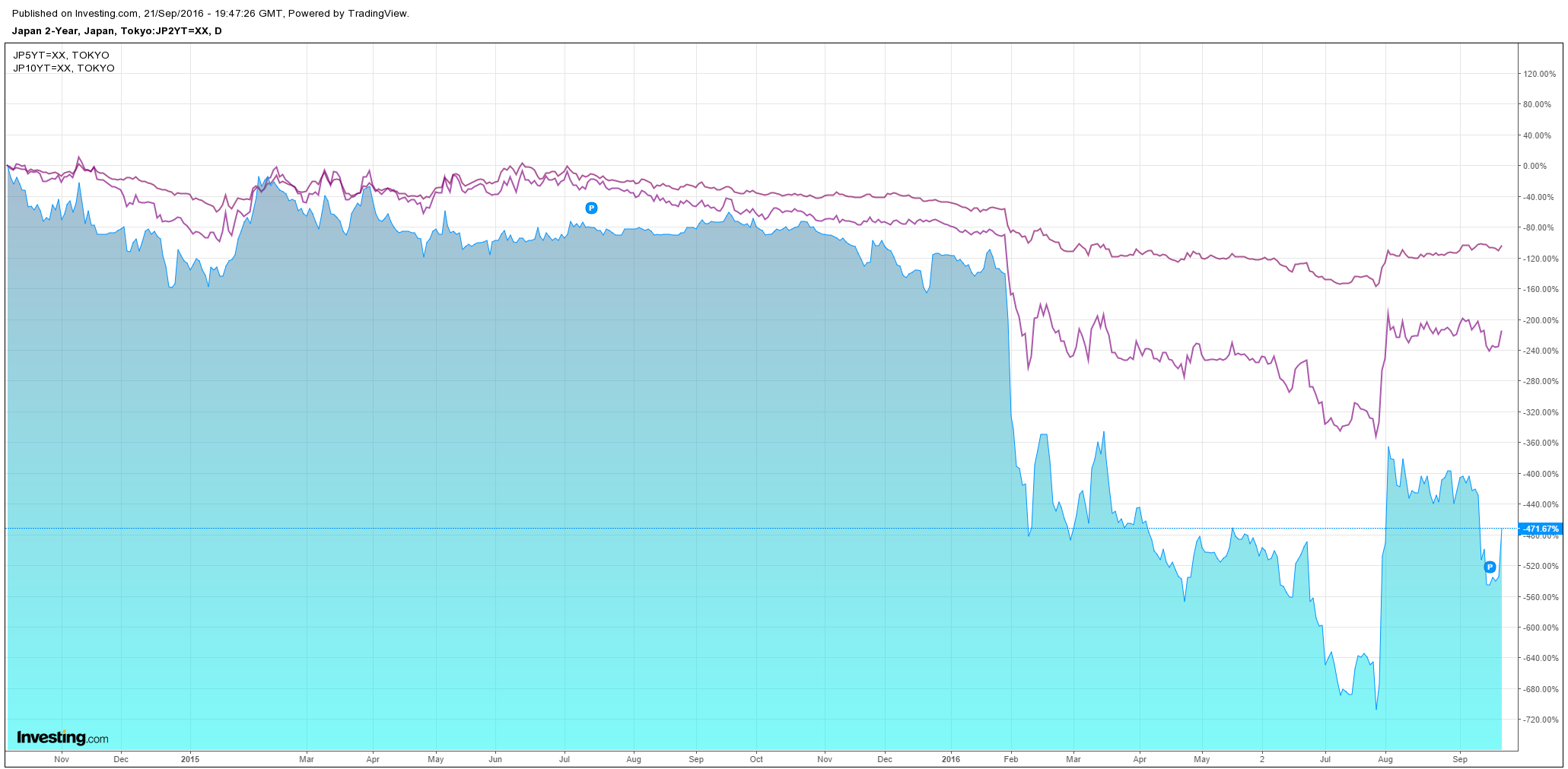

So did the Japanese curve when it was supposed to steepen:

Advertisement

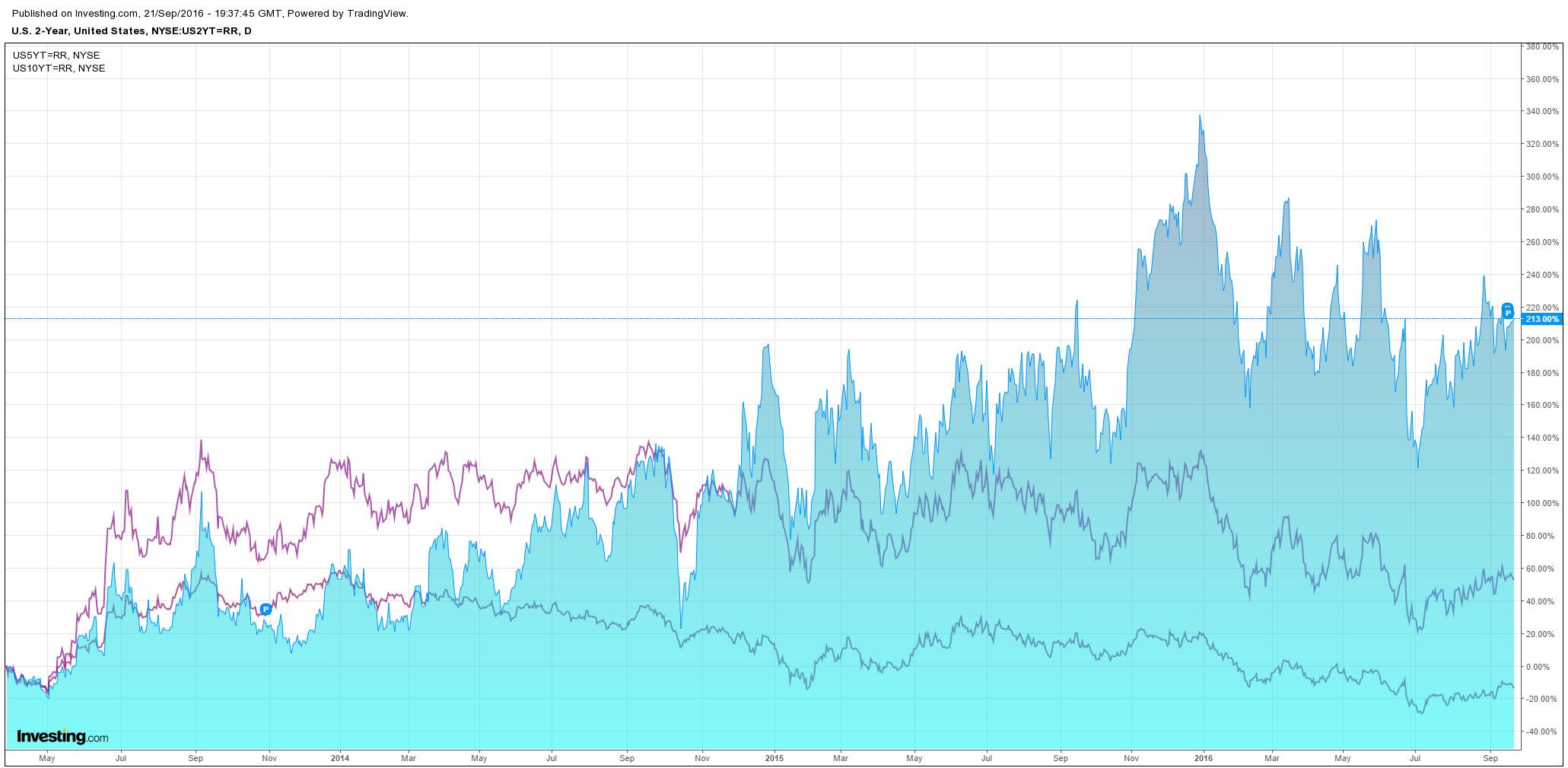

Stocks were bought:

The BoJ’s attempted steepening of the yield curve was spat on by traders which sold the short end of the curve more enthusiastically than the long despite the BoJ’s “strengthened forward guidance” that it will cut the short and anchor the long at zero. Markets looked straight through it as a bluff, perhaps busy looking at one another rather than the bank.

Advertisement

As such, the BoJ now has only two choices. It can watch its reputation and powers of suasion collapse or it can follow through on its threat to keep “…expanding the monetary base until it exceeds this [2% inflation] target.”

It is now in a position to do so which, in my view, markets are seriously underestimating. It may be that the BoJ wanted to try jawboning first but the major impediment to it actually going deeper into NIRP was this, from Algebris:

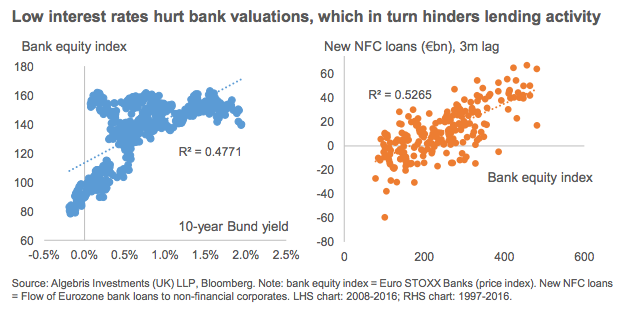

The key issue is the sustainability of banks’ business models. As discussed at length by the BIS and ourselves previously, low interest rates support banks with a one-off gain on their government bond holdings, but they also erode profitability, equity valuations – increasing their cost of capital –and reduce the banks’ ability to lend. This is what has happened in Europe and Japan, and at the latest ECB press conference in August, ECB President Draghi specifically talked about the positive correlation between credit intermediation in the Eurozone and bank equity prices. The BoJ shares similar concerns, with some Japanese banks starting to impose negative rates on clients earlier this year. In a meeting to assess the effectiveness of QE, Mr Kuroda stated that central bankers should weigh the benefits of QE and negative interest rates on corporates and consumers with its negative impact on financial intermediation.

Advertisement

Now with an anchored 10 year yield, the BoJ can slash the cash rate to the centre of the earth and bank net interest margins will be intact. There are still problems for banks with NIRP, not least being the mattress stuffing effect, but I can’t see why the BoJ would set this up if it is not going to follow through on it so for me the yen just became uninvestable.

However, any impact on other currencies was swiftly blown away by the FOMC which squibbed its September hike as expected but set up for one soon:

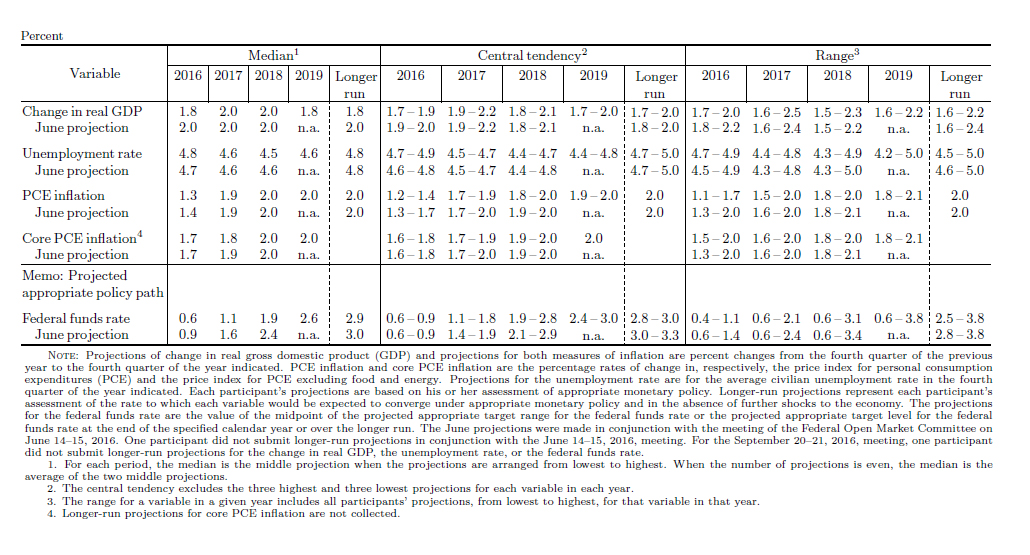

Information received since the Federal Open Market Committee met in July indicates that the labor market has continued to strengthen and growth of economic activity has picked up from the modest pace seen in the first half of this year. Although the unemployment rate is little changed in recent months, job gains have been solid, on average. Household spending has been growing strongly but business fixed investment has remained soft. Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will strengthen somewhat further. Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further. Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent. The Committee judges that the case for an increase in the federal funds rate has strengthened but decided, for the time being, to wait for further evidence of continued progress toward its objectives. The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Jerome H. Powell; and Daniel K. Tarullo. Voting against the action were: Esther L. George, Loretta J. Mester, and Eric Rosengren, each of whom preferred at this meeting to raise the target range for the federal funds rate to 1/2 to 3/4 percent.

Advertisement

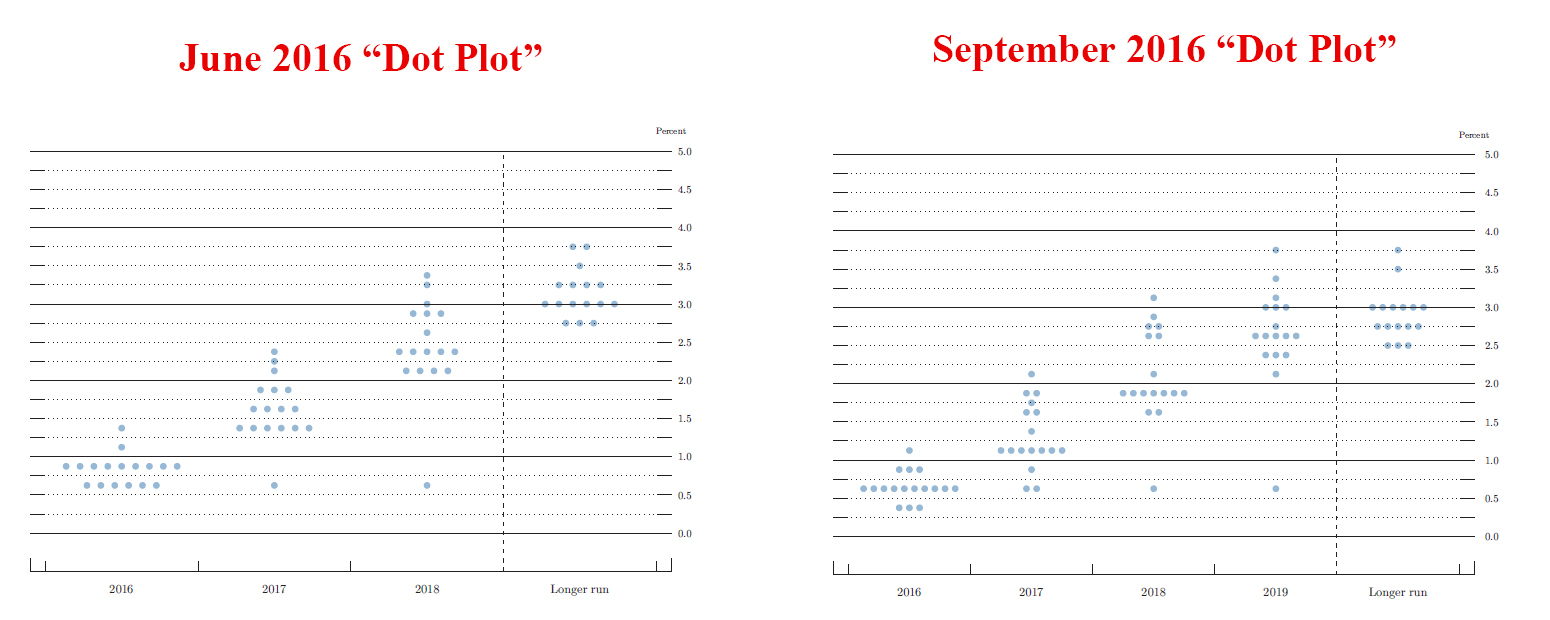

Both the outlook and path of future hikes eased very slightly:

The Fed clearly wants to hike but just cannot find the cojonies, as such risk was bought. But it can’t get far. There is enough hawkishness here to keep the lid on.

Advertisement

In sum, the BoJ is either poised to see its reputation collapse or to go much deeper into NIRP. I favour the latter so do not buy the rally in JPY. The Fed is poised to hike but whether it can is now held hostage to the dizzying array of risks presented yesterday:

US election;

Italy referendum, Brexit and the zombieuro;

China slowing, and

oil weakness.

If I’m right about the BoJ then you can add much stronger upwards pressure on the US dollar to that little lot as well.

Advertisement

It’s a rather unfashionable view I’ll admit, but for me the BoJ window looks open while the FOMC window looks closed.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.