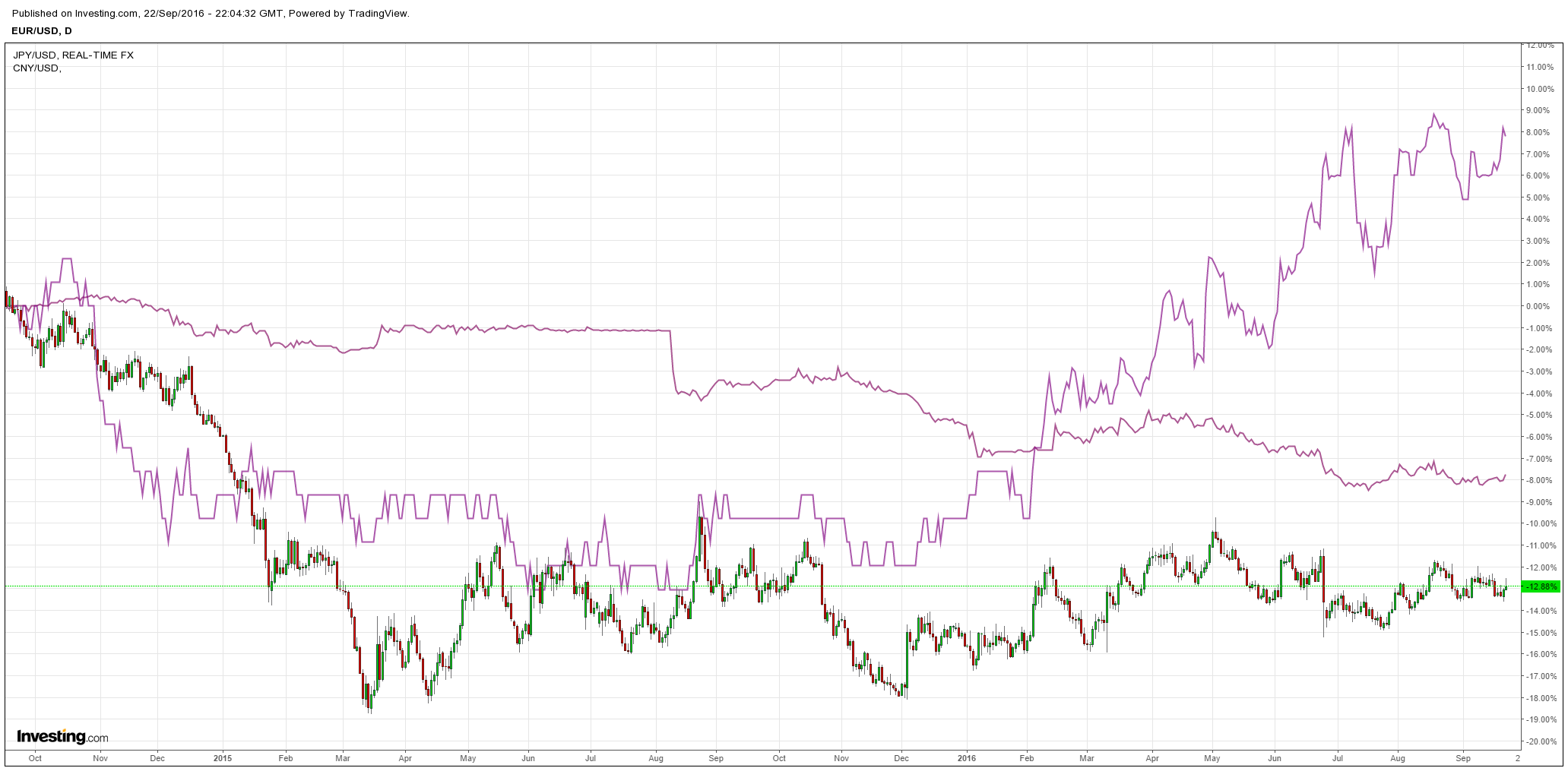

The USD was weakish again last night:

Others were not strong, however:

Commodity currencies were:

Gold was firm:

Brent too:

Base metal jumped:

Big miners are breaking out:

US and EM high yield jumped:

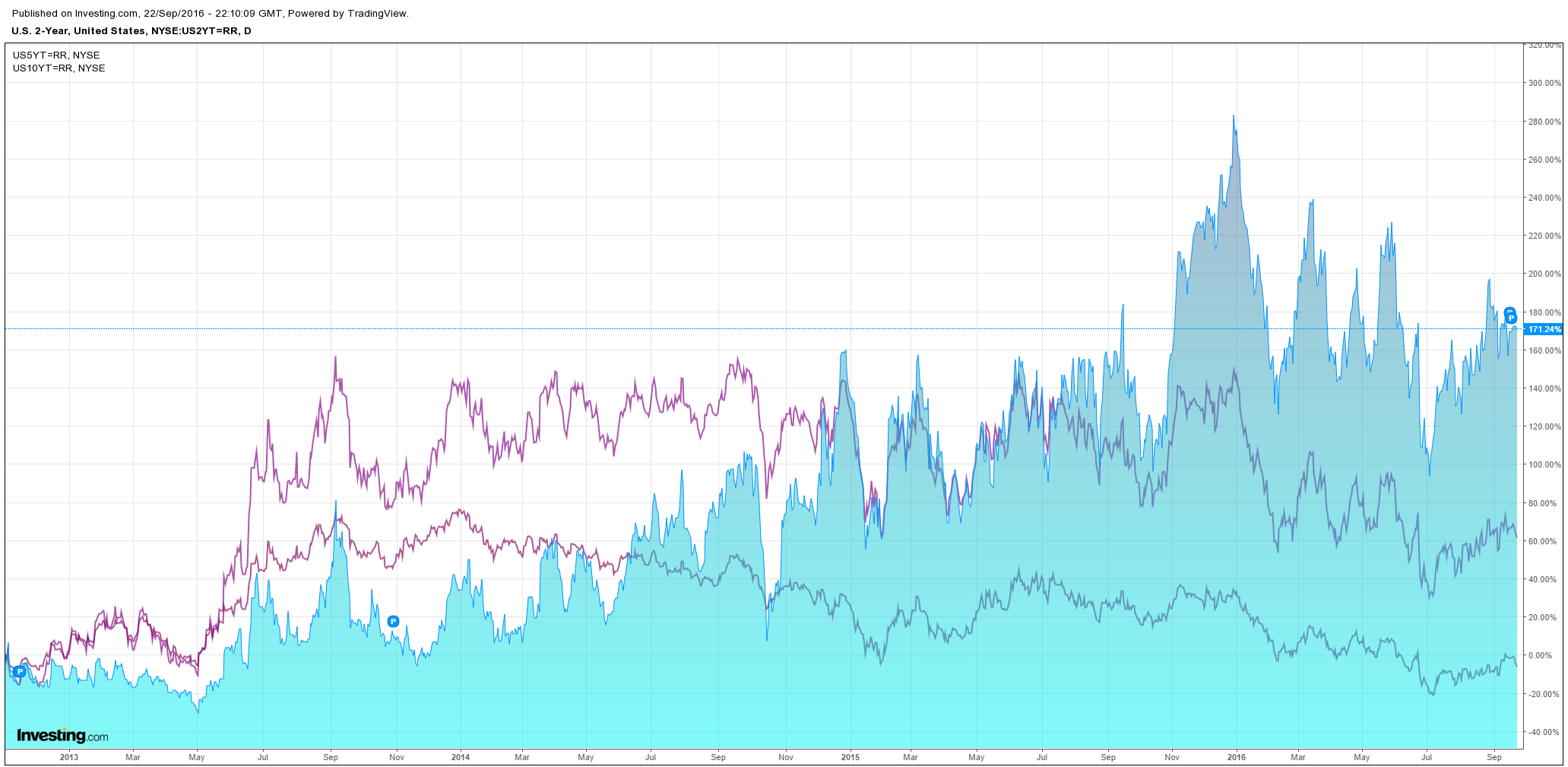

US bonds were bought:

Equities too:

The EM and commodity pain trade has resumed. The question is why? From RBC:

COMMENTARY: The Fed was some much more dovish than market had anticipated, specifically noting the FOMC’s 1) lowered dot plot, 2) removal of future dots, 3) the cut to their long-term GDP estimate–were what the equities-world fixated-on. Why? Clearly, the Fed is of the view that slower-growth is what lies ahead, and as such, the lower neutral rate means fewer hikes in the future—i.e. back to “lower forever.” Bottom line: nobody within the Fed–or market watchers outside of it–is expecting much hiking in the years ahead. I will highlight a quotation (noted by RBC’s Tom Porcelli) from Yellen yesterday which crystalizes the implied reticence towards making a definitively hawkish move in the near-term—showing that a very high bar still remains in her mind:

“…but with labor market slack being taken up at a somewhat slower pace than in previous years, scope for some further improvement in the labor market remaining, and inflation continuing to run below our 2 percent target, we chose to wait for further evidence of continued progress toward our objectives.”

As such, the “QE / reflation trade” is back “ON” for at least another two months—EM (EEM +2.8%), crude (USO +3.3%), gold (GDX +7.1%!), credit gapped tighter (esp beta energy and materials HY) and ‘cyclical-beta’ equities / Nasdaq (new all-time highs) all screamed higher, while the UST curve bull flattened, and the Dollar (and $Yen–sorry Abe / Kuroda—you’ve been usurped) and VIX (-16.5% on the day LOLOLOL) were smashed. An interesting note from Brian Chen on our ETF team this morning regards HYG / JNK too, where both ETFs closed ~90bps-ish premium to NAV. He expects significant “offers wanted in competition” activity in the create lists, as “…HYG has been difficult to source in the sec lending market, and short-covering ensues.” Major golf-clap for the UST long bond upside (Noorani) and VIX put spread (Simon) trade ideas pushed by RBC Macro this past week—these bad boys both have room to run. Also want to note that Mark Orsley this morning is putting out a “long NQ” (Nasdaq emini) call in light of the risk-environment provided by the central bank “vol murdering spree,” as the index sets-up as a reverse head and shoulders which broke its neckline.

Specifically with the equities market’s reception of the hyper-anticipated dual-policy updates, “everything” worked. We saw an enormous rally in “inflation” plays / leverage / weak balance sheet plays / “cyclical beta”—while too the opposite-end-of-the-spectrum “yield compression” trade re-reality helped drive performance back into the “bond proxies” (div yld, low vol factor, defensives). SOMETHING FOR EVERYBODY.

Judging from the extent of the squeezes in various “most-shorted” proxies, net exposure was added with gusto on the session as shorts books were reduced sharply. Perhaps some of this “buy everything” (both long buying and hedge fund short covering) was driven by the “real” source of funds—high mutual fund cash levels being taken-down and “put to work”….after all, on a year-to-date basis, the mutual fund equities “overweights” basket is trailing the mutual fund equities “underweights” basket by an ABSOLUTELY BRUTAL 9.6%, and that underperformance gap has to be closed for career-preservation purposes (GS noting only 16% of large-cap mutual funds are beating their benchmarks YTD, below the 10 year avg of 37%–h/t MF).

I suppose so. But in the background it is Japan that is leading the way here not the Fed, from Citi’s Willem Buiter:

First, these actions signify that central banks (notably the BoJ and, to a lesser extent the ECB) increasingly recognize that the previous paradigm of linking specific increases in balance sheet size to changes in aggregate demand and inflation is deeply flawed and needs to be replaced. But the immediate concern for these central banks is not so much diminishing efficacy of such purchases but rather the narrower issue of running out of suitable assets to buy and collateral damage of incipient asset shortages (including excessively flat yield curves and volatility in long-end yields), in our view (Figure 1).

Second, the obvious response to asset shortages is to move from a quantity-based framework to a price-based one: asset price targeting, or more specifically (or at least in the first instance) yield caps or yield targets. At least in principle this shift may create some useful additional flexibility for central banks and allows them to move away from the potentially unnecessary fixation on quantities and balance sheet sizes. However, such an approach also comes with a number of potential – conceptual and practical – limitations and complications, which vary by country, but make it unlikely that the ECB will follow suit and move to explicit asset price targeting anytime soon.

Third, the BoJ decision leaves open the question what central banks could still do to boost aggregate demand and raise inflation expectations. In some ways, it is startling that the BoJ, while admitting that inflation rates have weakened (even though still forecast to reach the target in 2019), left the policy rate unchanged and picked the new 10-year yield target around current levels (Figure 2). Today’s decision therefore does not imply any further easing. The only announcement introduced to boost inflation expectations was the so-called ‘inflation-overshooting commitment’ to maintain expanding the monetary base until observed CPI inflation exceeds 2% and therefore indicated that the BoJ would be prepared to tolerate inflation overshoots. However, without adequate instruments, such a commitment is hardly credible and raises the question of how the BoJ intends to meet (or exceed) its inflation target.

The BoJ announcement did point at various options to ease further (including lowering the policy rate further into negative territory, further asset purchases and increases in the pace of monetary expansion), also highlighting the synergies between fiscal and monetary policy. But in our view, in the absence of more forceful fiscal stimulus, it is far from clear – in the case of the BoJ specifically, and in the case of central banks faced with long-running inflation undershoots more generally – how central banks can boost aggregate demand and inflation significantly (Figure 3 and Figure 4). In the case of the BoJ, the likeliest next easing step is probably a moderate cut to the policy rate (which may or may not be associated with a cut to the 10-year yield target).3

Yield targets are therefore at best an answer to asset shortages, but not to the broader question of how to reach their inflation targets. But for now, central banks are not prepared to give up just yet, which is why we are likely to see them experiment even more over time.

Don’t we all already know that Japan will fail to stimulate demand and inflation? As such, it’s not going to stop doing whatever it has to to lower the yen, from Goldman:

We think deepening the negative interest rate remains the BOJ’s main option for future easing going forward. As the BOJ acknowledges, an impact on financial intermediation is one side-effect of negative interest rates, which means the policy has to be used sparingly. However, given that the BOJ seems to believe that this is the only policy tool that could be an effective means of correcting yen appreciation, we think it will inevitably become the BOJ’s policy tool of choice. In a recent speech, Governor Kuroda stated: “NIRPs certainly provide more leeway with central banks in coping with a variety of adverse shocks as a practical monetary policy tool.” We see a possibility that the BOJ may move to deepen the negative rate more on an ad hoc basis in response mainly to exchange rate shocks, rather than as a response to economic fundamentals such as real economic conditions and prices. That said, the BOJ may now refrain from playing any further cards until market participants have had time to figure out how the new framework will function.

Yep. They’re going to take NIRP to the centre of the earth. How can that possibly be yen bullish? And if so how can that possibly be consistent with an EM and commodity pain trade? Moreover, ever if you reckon Japan is out of bullets and you’re going to buy the yen on, say, a theory about a forex snap-back, then how can Japan sinking into a deflationary morass from which it cannot escape possibly be bullish for Western economies heading down the same path?

Perhaps the EM and commodity pain trade is back because the Fed is now seen to be cornered on further hikes.

Beyond quantitative failure is helicopter money but nobody appears willing to take that step and until the do collapsing central banks credibility is not bullish for anything, except perhaps gold.