As already noted by Houses & Holes, Treasurer Scott Morrison today delivered a speech to Bloomberg in Sydney. While Houses & Holes has already analysed the overall content, I want to focus on just one part: the discussion on Australia’s debt trajectory, which Morrison claims is perilous if various Budget measures are not passed:

To ensure we are prepared for whatever events may occur in the future we have much more work to do, especially in the area of budget repair, to strengthen our nation’s finances… we must arrest the growth in our public debt, before it is too late, by getting expenditure under control at sustainable levels and boosting revenues through growth friendly tax policies and protecting the integrity of our tax base…

Our debt now stands at around $430 billion, with interest payments at $16 billion this year, now one of the largest line items in the budget and growing.

Our CGS on issue, our gross debt, is increasing by $6 billion a month or $1.4 billion per week in 2016/17 ($72 billion for the year).

While our debt is low by global standards, and our placements are well covered, this is no excuse to be complacent about debt.

Our government debt to GDP is well below other AAA rated countries. However our net international investment position is the inverse.

This is because Australia has always been a net importer of capital, especially in the private sector. This has been a key source of our prosperity and development. Of itself, this is not a problem, as the investment is supported by real assets and is in productive enterprises.

However, it does mean we have less head room for Government debt than other advanced economies that fund their own debt, and why ratings agencies tend to be very focussed on Australia’s deficit and debt position. All Australian Governments must therefore be more conscious of our collective debt position. Just because rates are low, doesn’t mean the money is free – you still have to pay it back.

To arrest our debt we must restore the budget to balance…

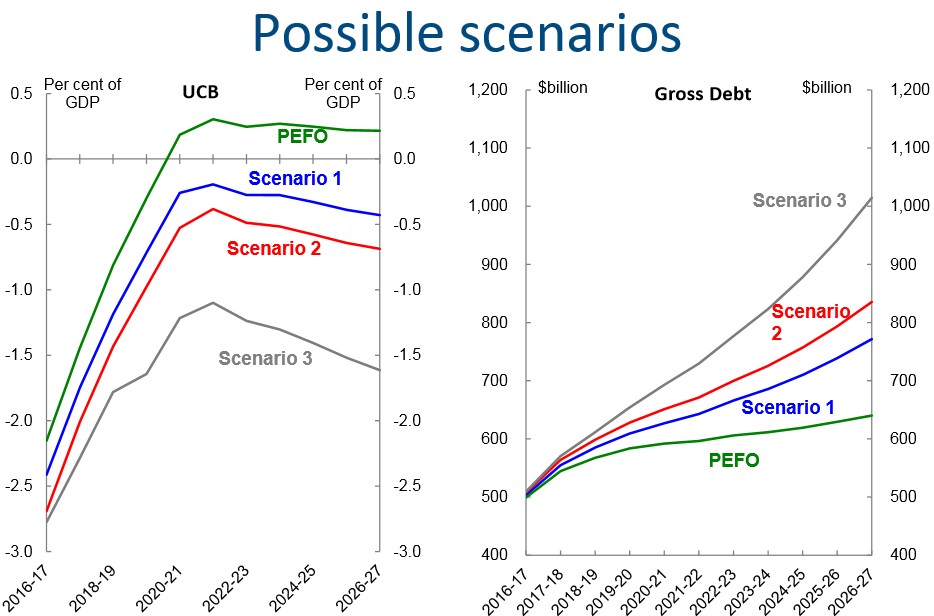

The worst case scenario will see our gross debt exceed $1 trillion in a decade. The other scenarios place debt just above and below $800 billion…

The period of this term could well prove to be the tipping point on the trajectory of debt our children and grandchildren will be saddled with. Once that debt fully takes hold, it will build its own momentum and will only grow more difficult to tame.

Let me state from the outset that I agree with Morrison’s position that current Budget settings are unsustainable and need to be fixed.

However, what I find irritating is that there is little acknowledgement of Australia’s monster household debt, which is now the highest in the world at 124% of GDP:

Advertisement

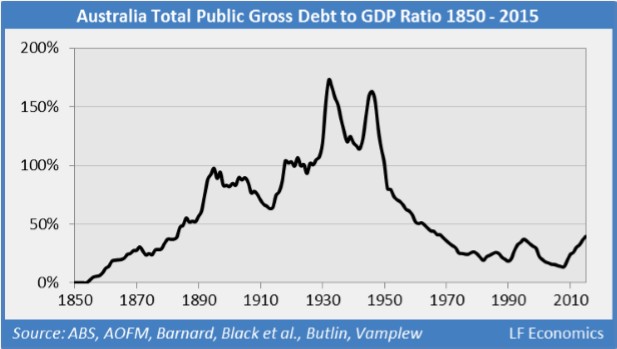

And dwarfs Australia’s public debt load:

Yet, rather than acknowledging the household debt elephant, Morrison – like most Australian politicians and commentators – has chosen bury his head in the sand, clinging to the out-dated Pitchford thesis that private debt doesn’t matter. All the while he supports policies like negative gearing and the CGT discount, which encourages further speculation in non-productive housing and the accumulation of more debt.

Advertisement

Instead of focusing solely on Budget reform for the sake of our “children and grandchildren”, how about some reform of Australia’s housing policies, which have left Australia’s youth with monster private debt loads that they will struggle to repay, or priced them out of home ownership altogether?

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.