Commodity currencies were mixed, Aussie the strongest:

Gold roared:

Advertisement

Oil fell again:

Base metals yawned:

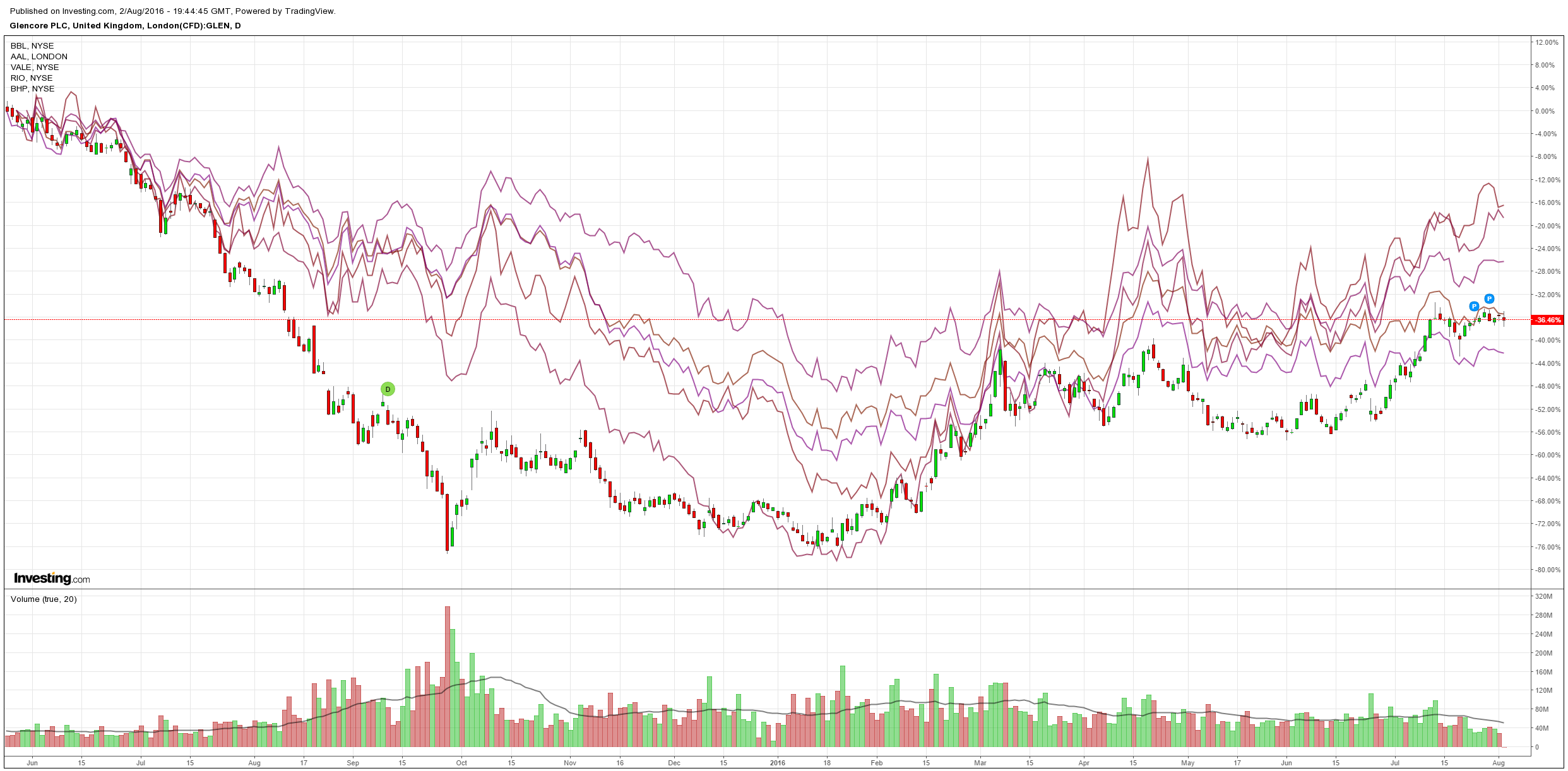

Big miners fell:

Advertisement

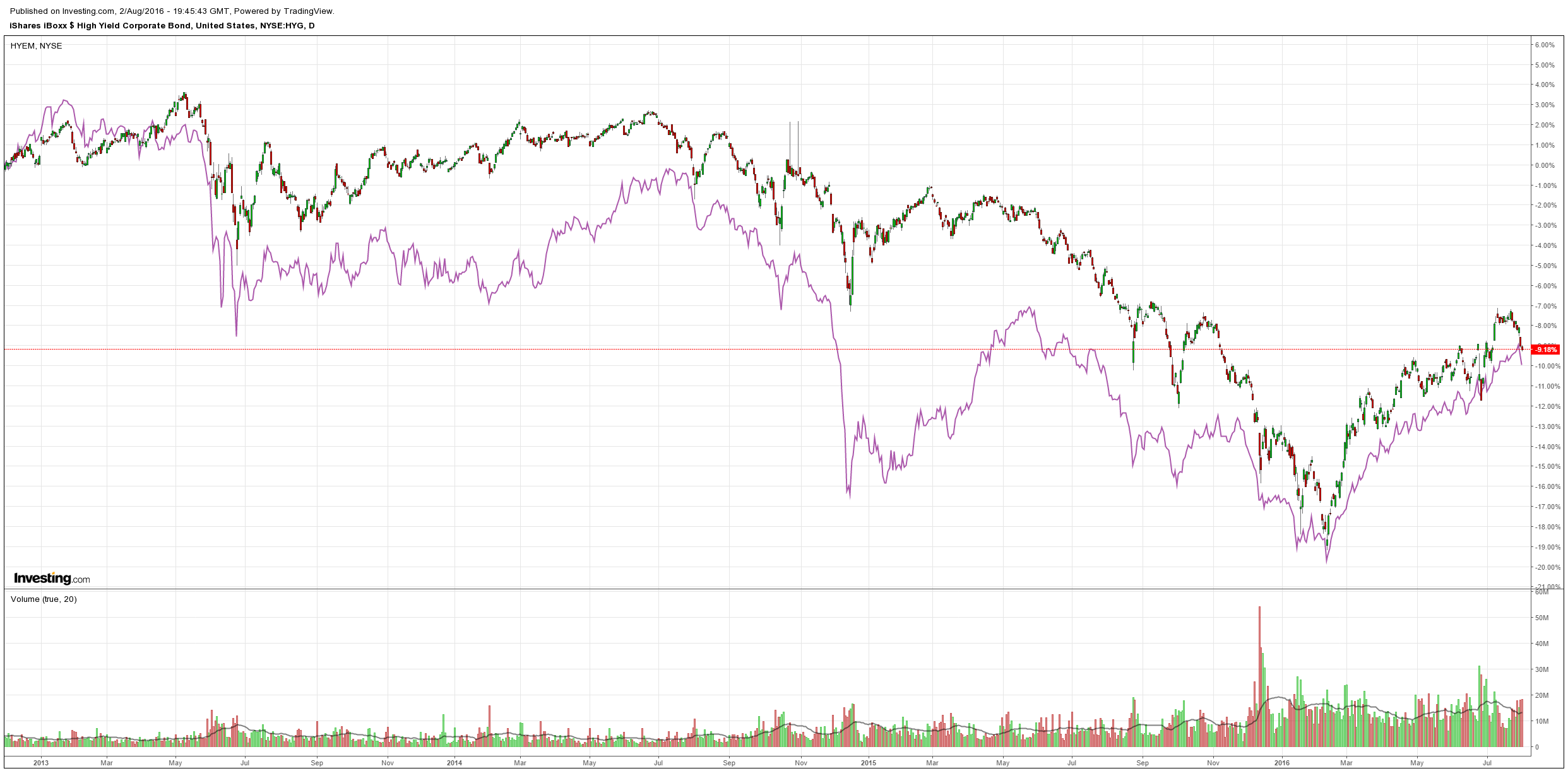

US and EM high yield woke to oil:

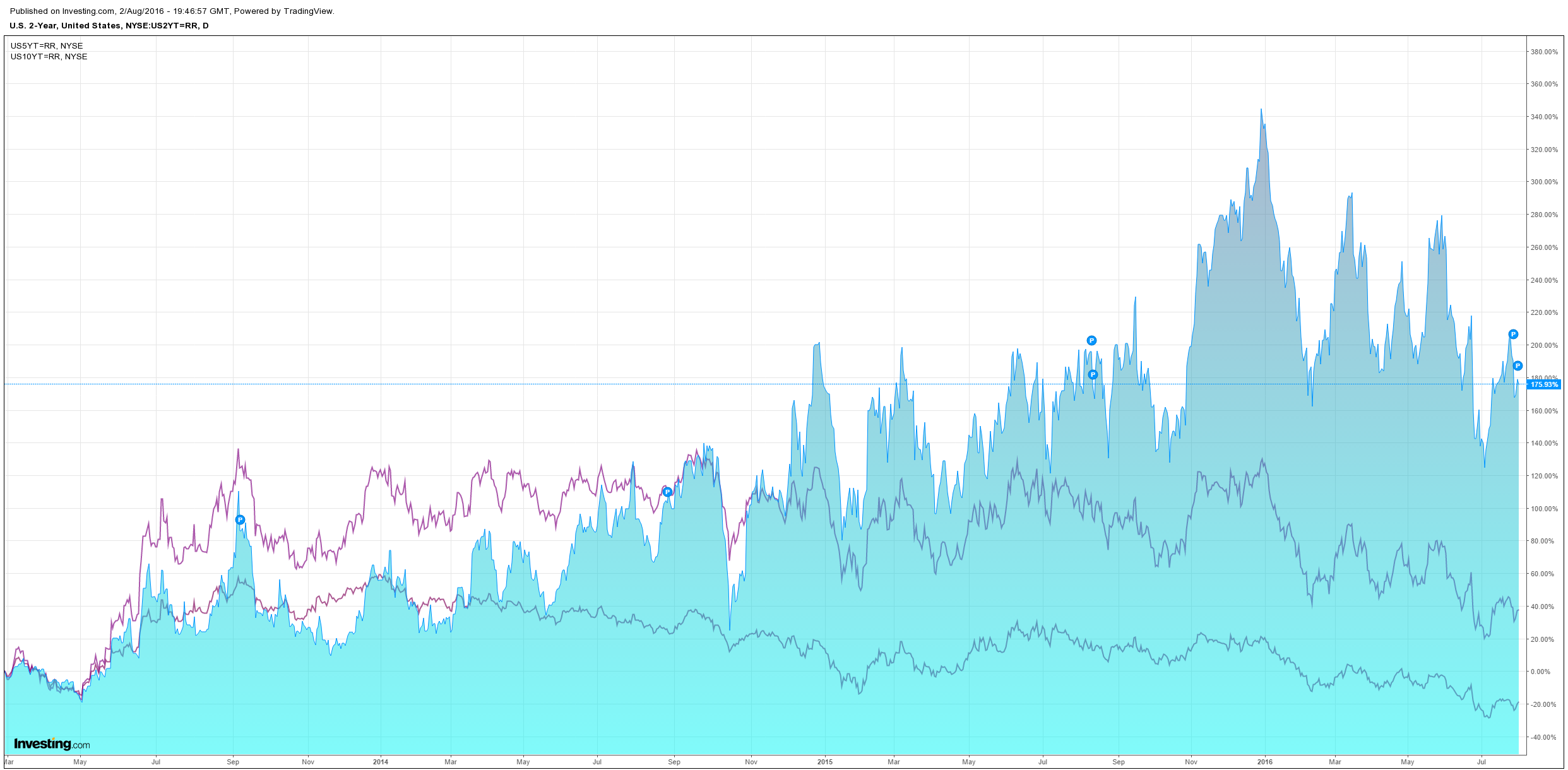

US bonds were mildly bid:

Equities took a modest hit:

Advertisement

So, the oil crash is starting to bite at the margin but only a little. The differences between today and early in the year are threefold:

the Fed is much less hawkish;

China has stimulated, and

we’ve seen some oil market rebalancing.

But that’s not enough. Oil is going to keep on falling. If it wants to clear the glut it has to. That presents us with a new set of market parameters:

Advertisement

Fed hawks will see inflation fall back;

US income growth will decelerate as its shale oil patch sinks further into recession;

the Fed is “one and done” for this year and probably next as well.

Thus we can expect a soft US dollar and upwards pressure on the Aussie. How much?

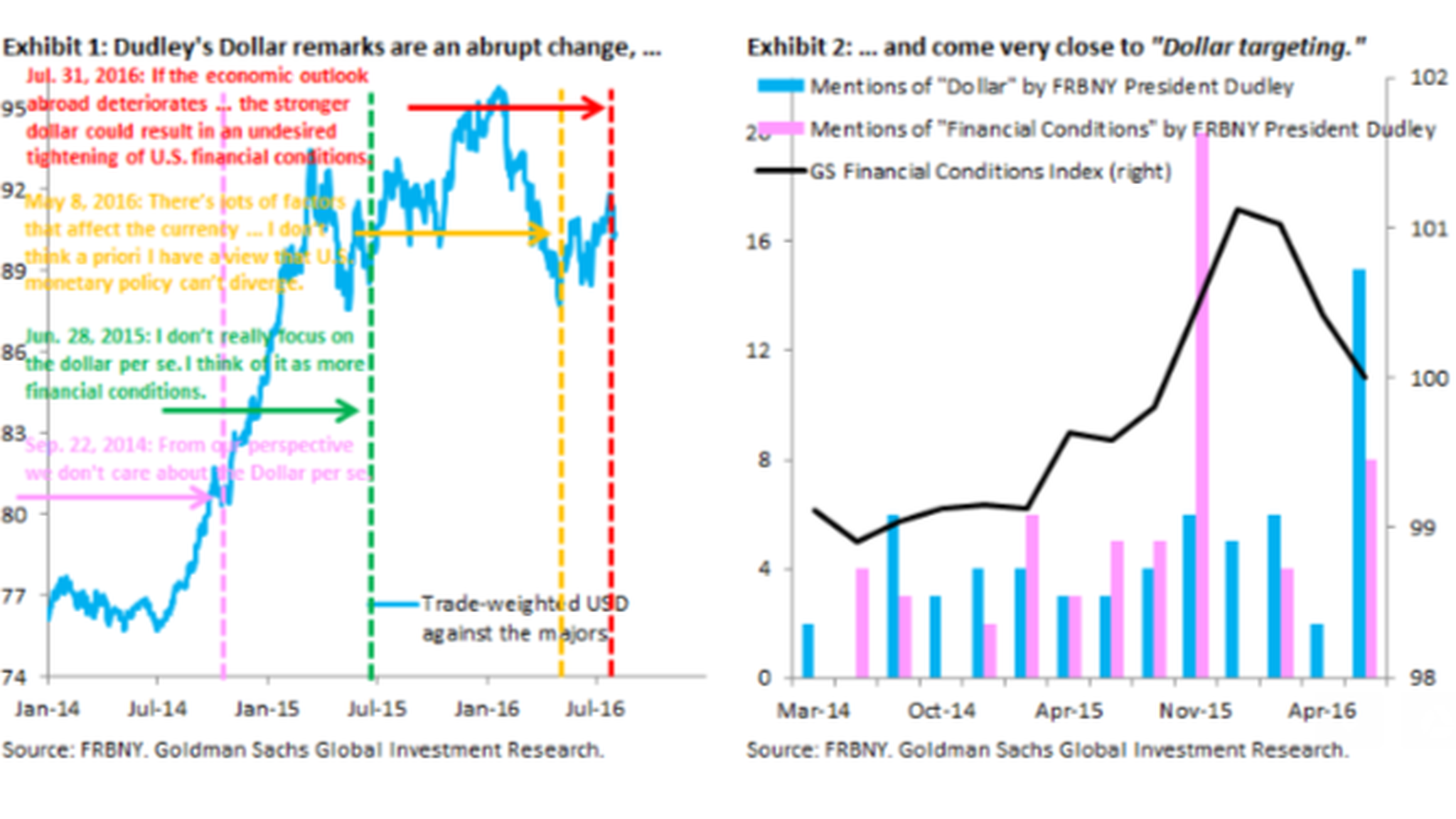

I’ve been of the view that a neutral Fed would not be enough to sink the US dollar, largely because everyone else would continue to easing much more. But that assumption is also under question. From President William Dudley of the Fed yesterday:

Advertisement

…U.S. financial market conditions depend, in part, on the stance of U.S. monetary policy relative to monetary policies abroad.

If the economic outlook abroad deteriorates and this causes foreign countries to pursue a more accommodative set of monetary policies, then the dollar would likely appreciate―other things equal― reflecting expectations of lower interest rates abroad relative to U.S. interest rates. In this case, the U.S. may need to adjust its own monetary policy path.

If the FOMC did not make this adjustment, the stronger dollar could result in an undesired tightening of U.S. financial conditions.

This is a crucial point and I want to make sure there is no misunderstanding. The Federal Reserve is not targeting the exchange value of the U.S. dollar.

What the FOMC considers are financial conditions broadly defined, because they affect the saving and investment decisions of households and firms.

The dollar is but one component of these financial conditions. The level of short- and long-term rates, credit spreads, and equity prices are also important components of the financial conditions that we closely monitor.

If international developments shift U.S. financial market conditions―including the dollar―then we need to take this into consideration in our U.S. monetary policy decisions.

And a response from Goldman:

Advertisement

It is an open question whether the speech marks a paradigm shift that moves the Fed in the direction of currency targeting. But if this is the case, the effort to reflate their economies by the ECB and BoJ could be a key casualty, because it requires both central banks to push further and further into unconventional territory, which is turning out to be difficult for both banks.

More reasons to be US dollar bearish. Then there is this from Michael Hartnett BofML:

Happily, the fiscal flip this summer has thus far been more biased toward redistribution & Keynesianism rather than protectionism. For example:

In Japan Abe has hinted at an economic package at the upper end of the ¥20-30tn range with ¥13tn in fiscal measures, possibly to include 3% min. wage hike and ¥15,000 cash to low income earners;

In Europe the growth of government spending has accelerated back to its pre-Global Financial Crisis pace, adding >1% to GDP growth in 2016 (note a newly permissive ECB cancelled Spanish & Portuguese fiscal rule-breach fines in the past month);

And in the US both presidential candidates are touting infrastructure spending packages (Clinton proposes $275 billion in infrastructure spending over five years; Trump has also proposed tax cuts, infrastructure & health spending. Note Ethan Harris argues that in coming years fiscal policy is likely to become more effective than monetary policy.

And Macquarie:

Advertisement

We maintain our view that the future of monetary policies is not impotence but merger and coalescence with fiscal and income supports (such as minimum income guarantees) as well as growing de-globalization (greater impediments to trade flows and closure of borders). This could become a potentially much more potent instrument in stimulating multiplication of aggregate demand and inflation, at least in the short-term. In our view, public sector funding from the bond market has its limitations as does re-distribution of wealth. Eventually public sector spending and investment is likely to be largely funded directly by central banks. These policies could lead to significant hyperinflationary, stagflationary or deflationary side-effects but alas there is no other choice.

This implies that investors are entering a world of public sector rather free market signals. However as highlighted, we believe that certain preconditions need to be met before such a significant shift in public policy can be accomplished. We have traditionally identified four door-step conditions, with much higher volatility being the most important one. Whilst the intellectual case for more proactive fiscal policy and its merger with income support and monetary policies have already been made and conventional (at least as defined since ‘08) monetary policies are coming to an end, we believe that one needs a volatility jolt to coalesce consensus.

In short, no helicopter money before the next crisis, the MB view. But, in the mean time, we are seeing modest fiscal loosening in economies where we expected greater monetary easing and that is another reason to be bearish on the US dollar.

At this point, given how horribly the RBA has misjudged this business cycle – seeing it as some kind of cyclical event instead of a structural change and has, therefore, completely failed to position Australian for the global currency wars – I would seriously consider abandoning my long held Aussie dollar short. However, there is a few reasons why I won’t:

the global business cycle is mature;

corporate credit metrics in the US are awful and getting worse;

Chinese stimulus goes through mini-cycles and will slow in H2 with its property market;

nobody in their right mind can go long euro beyond the end of their nose given the series of BREXIT-style elections that are coming, and

some kind of high volatility event is still a central case for the global economy in the foreseeable future and the Aussie will crash when it comes.

Advertisement

But, these are structural problems that coalesce at some unknown point. The cyclical pulses currently in play are going to push Australian dollar “pain trades” in the meantime, and the RBA is not going to move fast enough to prevent them.

I’m not going to change my outlooks for the currency and still see the trend going lower over the medium term but I have to warn that over periods measured in months the Aussie could hurt to the upside, so if you’re not comfortable with short term pain then take note.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.