In a rare glimpse of honesty from an Australian politician, former Labor minister for superannuation, Nick Sherry, yesterday warned that further reforms to Australia’s retirement system will be necessary even if the Coalition’s superannuation package is implemented in its entirety. From The AFR:

With the age pension forecast to rise by $2 billion a year to $52 billion by 2019-20 and the cost of super tax concessions increasing by 7.6 per cent a year – assuming the current reform package is passed – the retirement savings system will remain unaffordable, Mr Sherry will argue.

“It is still unsustainable, hence more change will occur. Calls to halt change or ‘stop fiddling’ are unrealistic”…

Mr Sherry is largely supportive of the Coalition’s reform package, apart from the proposed changes to transition to retirement pensions, which he says do not go far enough, and the removal of anti-detriment provisions.

Sherry is spot on.

However, while there will still be lurks remaining in the superannuation system, even in the event that the Coalition’s package is implemented, further reforms to super will remain off-limits for some time.

The other major area that needs addressing to make the retirement system sustainable is the Aged Pension, whose cost is blowing-out and could be far better targeted towards those in genuine need.

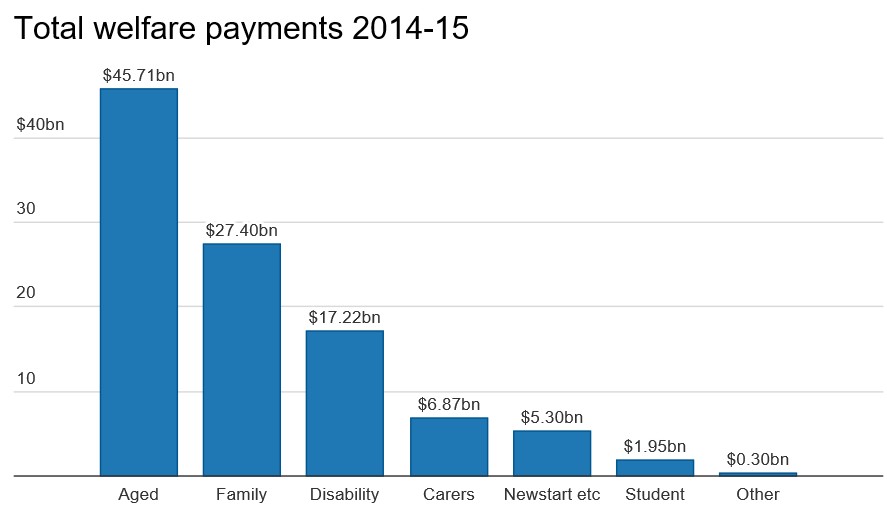

As shown in the next chart, the Aged Pension dwarfs the other forms of welfare expenditure, costing $45.7 billion in 2014-15 (see below chart).

Moreover, as noted by Sherry, Aged Pension costs are projected to rise by $2 billion per year to $52 billion by 2019-20.

The major issue with the pension is that it is poorly targeted because it excludes most people’s biggest asset – their principal place of residence – from the assets test to qualify.

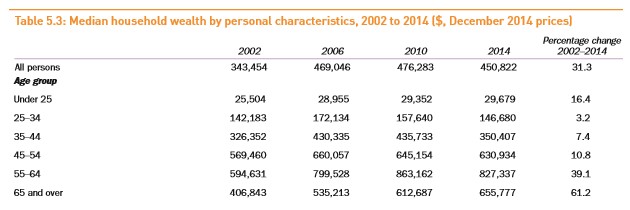

Last week’s HILDA survey revealed a rapidly growing wealth divide, whereby median wealth increased by 61% among those aged 65 and over between 2002 and 2014, compared with just a 3.2% increase in wealth among those aged 25 to 34:

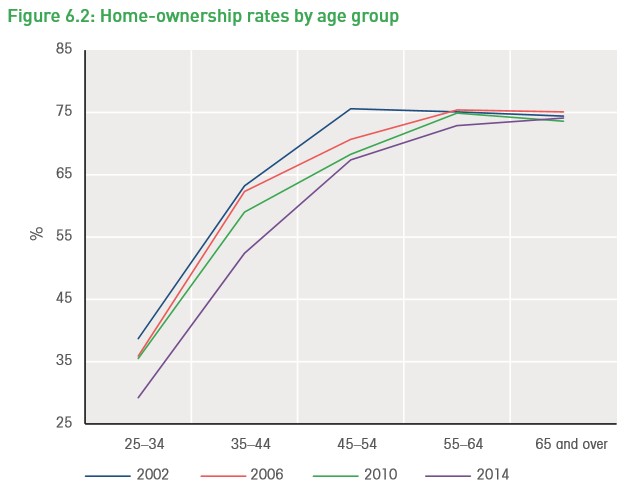

The HILDA survey also showed that while home ownership rates have collapsed for younger cohorts, those aged 65 and over have experienced stable ownership whereby roughly 75% own a home (most outright):

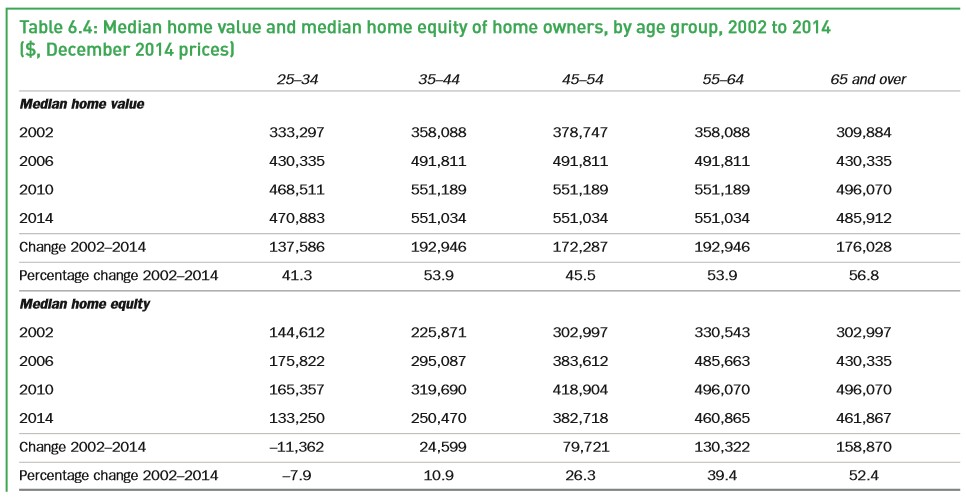

Meanwhile, those aged 65 and over have also enjoyed the biggest rise in median home equity, which stood at a whopping $461,867 as at December 2014:

Therefore, Australia has the perverse situation whereby older Australians have experienced an unparalleled rise in wealth at the same time as their dependence on the Aged Pension has risen rapidly, and is projected to continue doing so.

Meanwhile, relatively poorer younger Australians are heavily subsidising the retirements of their well-off parents and grandparents, whose biggest asset (their principal place of residence) is excluded entirely from the means test to qualify for the Aged Pension.

This situation makes absolutely no sense from either a budgetary or an inter-generational equity perspective.

For these reasons, MB has for years supported the following reforms to the Aged Pension to better balance Budget sustainability and equity:

- Include one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Extend the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HELP-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under this plan, house-rich pensioners could continue to receive an income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers.

Without reform to the Aged Pension, the burden of Budget cuts/tax increases will fall entirely on the growing pool of younger (and renting) Australians. This situation is clearly unsustainable from a Budget perspective and inequitable from an inter-generation one.

One wonders how much longer politicians can continue ignoring this elephant in the Budget room.