Are markets pricing for QE4? That’s the only way to make sense of today’s bizarro action. The US dollar eased:

Yen and euro were flat:

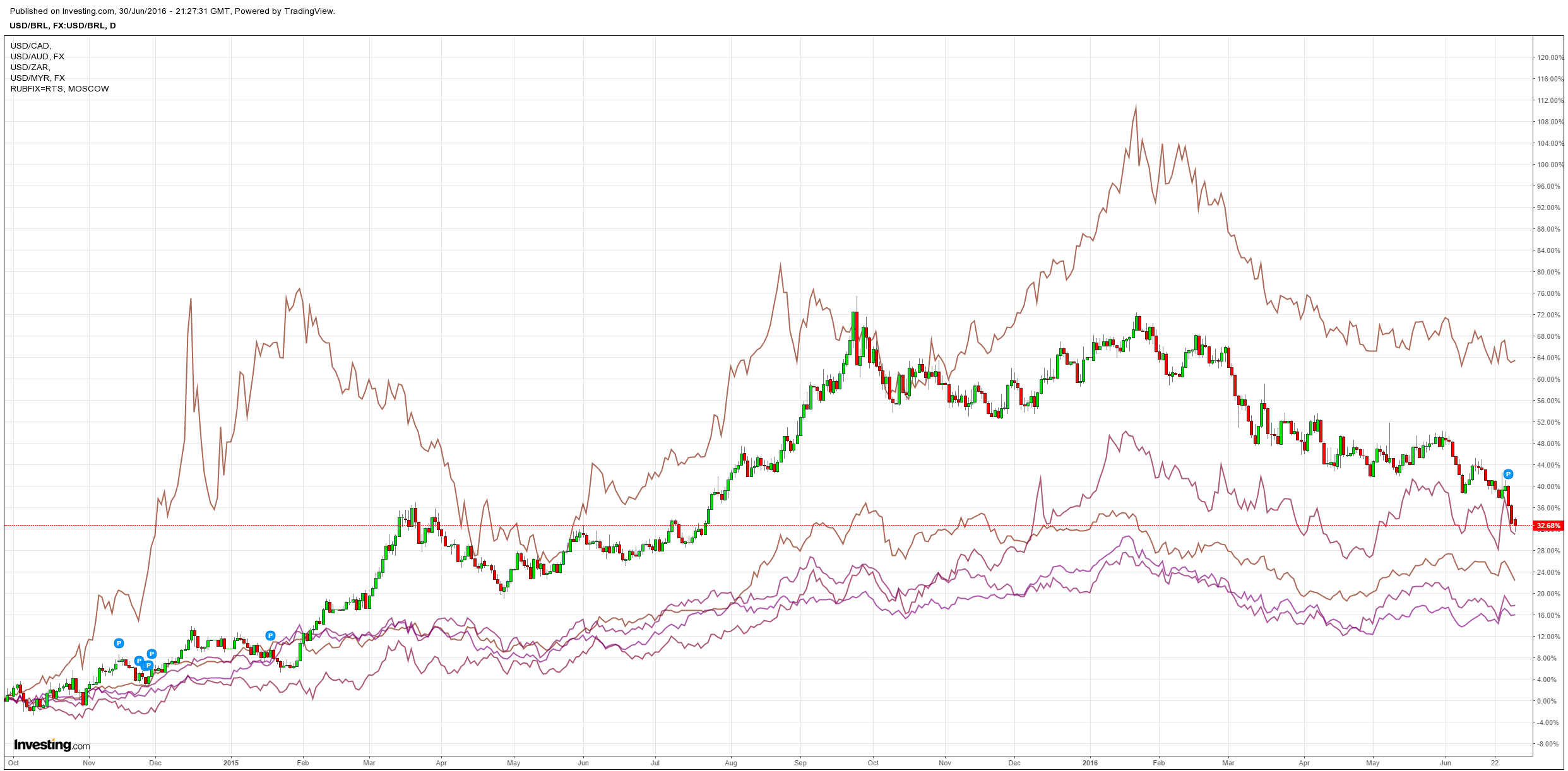

Commodity currencies were mostly firmer:

The Chinese yuan sank on rumours the PBOC is targeting lower:

Gold was firm:

Oil was whacked:

Base metals flew:

So did big miners:

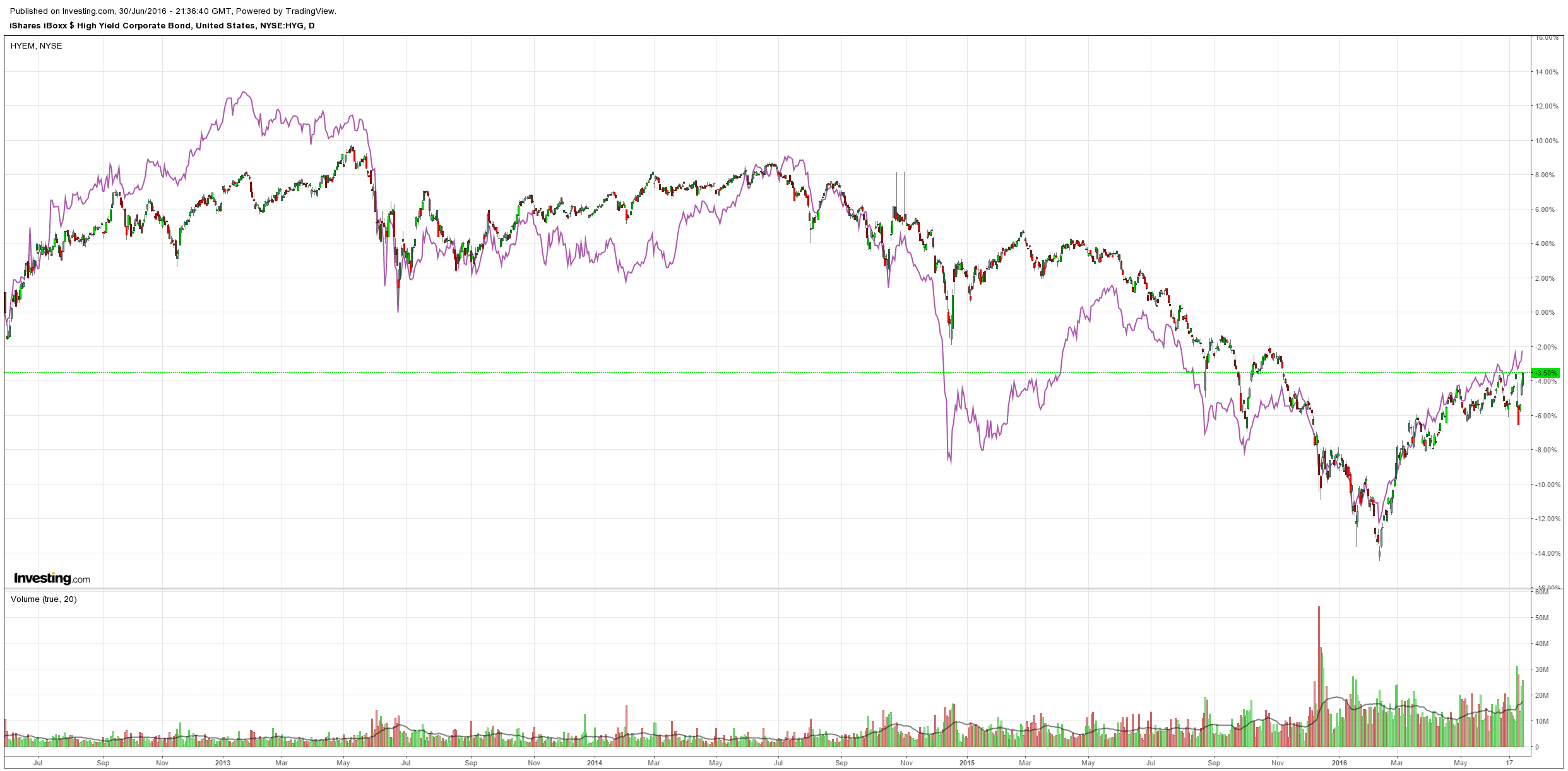

EM and US high yield debt broke out despite oil:

Stocks roared:

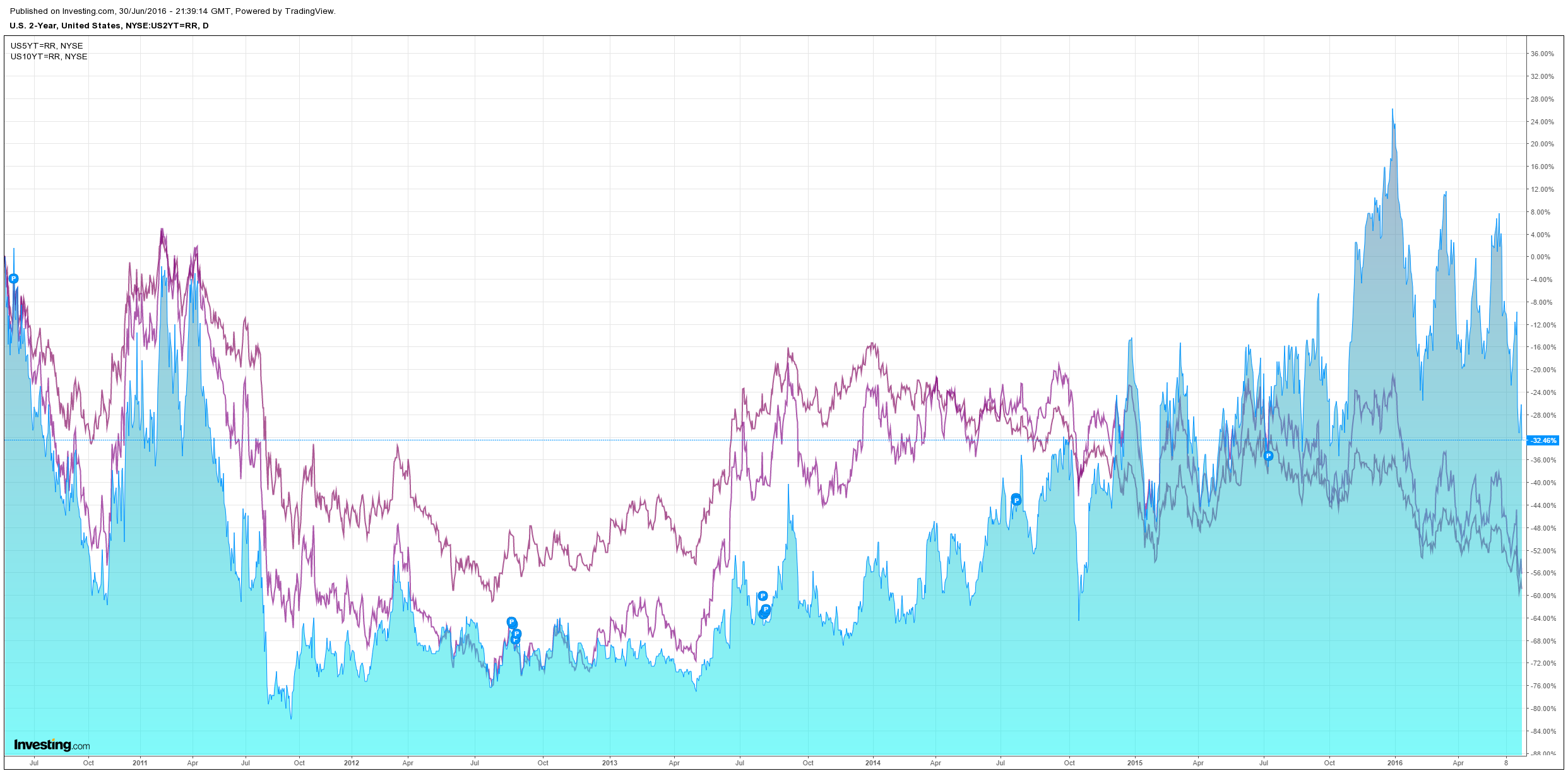

Bonds yields crashed:

That’s about as close to nonsensical market action as I can recall. Stocks have forgotten Brexit or are so confident of stimulus that they’r rising anyway. But have moved so far, so fast that it is no longer necessary anyway. Bonds are very bearish. Commodities are flying even though China is slowing and yuan tumbling meaning less need for imported commodities. Yet oil wanted no part in it even as high yield credit was heavily bid.

The only way to make any sense of this action is that markets are pricing for QE4, though gold and oil weigh against that. Or, or course, it is just a night of nonsense!

The news flow was certainly that with Boris Johnson bailing from the UK PM race, Italy demanding bank bailouts, China rumours about a weaker yuan, S&P downgrading the EU, BOE signaling more easing, IMF warning on EU and UK growth and the ECB warning it is running out of stuff to buy.

Let’s leave it with JPM:

Market update – the SPX opened flat-to-up small but caught a lift around ~10:30amET, around the time DJ reported on a MDLZ bid for HSY (which would be a >$20B deal) and this WSJ Italian bank article hit (http://goo.gl/R6UccS), while Carney’s prediction of BOE easing later this summer isn’t hurting (although the BOE was widely expected to enhance accommodation in the coming months). Also at 12pmET Bloomberg reported on how the ECB was considering easing its QE criteria to account for the expanded pool of bonds w/yields below the deposit rate. Beneath the surface sentiment is increasingly cautious, with most investors anticipating the resumption of selling once we get past month/quarter-end (nearly no one thinks stocks will get off “this easy” from the referendum decision last week). Other than the MDLZ/HSY news, Italian bank noise, and the Carney remarks,narrative-shifting news was pretty minimal over the last 12-18 hours. The UK political dynamics are interesting but Boris Johnson wasn’t the PM front-runner even before today and regardless it will likely be a few more weeks at least before the next British leader is known (and the triggering of Article 50, if it comes at all, won’t occur until 2017 at the earliest). The China CNY Reuters article created initial anxiety (as CNY depreciation was the catalyst behind the Aug and Jan/Feb swoons) but stocks (esp. in the US) seem less sensitive to this topic (the issue isn’t so much the absolute CNY level but instead pace and this is something China’s leadership appears to now appreciate).