Academic Professors Ralph Horne and David Adamson have joined the campaign calling on Australia’s political leaders to implement a national housing policy. From The Conversation:

We have to move the housing conversation beyond a game of political football about negative-gearing winners and losers. Australia needs a bipartisan, long-term, housing policy. Why? Because we have a slow-burn, deepening crisis that is affecting Australians who are already highly vulnerable and disadvantaged. They include:

The UN Rapporteur on Human Rights, following a visit in 2007, concluded that Australia was failing to deliver the fundamental human right of adequate housing because of the lack of any co-ordinated national strategy. Nothing has changed since 2007.

A failure to join the dots of housing policy

Our cities will stop working if we do not do something. A decent long-term housing policy is not just about the million or so Australians who are in housing need, marginal housing or homeless. In reality, housing demand and supply for all tenures is intricately connected.

Failed first-time buyers rent privately, increasing demand and rent levels. This pushes lower-income families towards social housing waiting lists and, at the end of the queue, those on marginal incomes are more likely to experience homelessness. Investors push out would-be home buyers by leveraging generous tax breaks that are not available to renters who are saving up to buy.

Changes in the value of new lending to investors, first-home buyers and subsequent buyers from December 2008 to March 2016.CoreLogic, ABS

More than 40% of people in private rental pay more than 30% of their income for housing – and this is after taking into account Commonwealth Rent Assistance. The 30% threshold is generally recognised as the level at which financial stress is experienced.

While states and territories have a wealth of experience and a clear role in delivery, the fact is the Commonwealth government must take a leadership role in co-ordinating national housing policy and connected programs across the four sectors of our housing system: home ownership; affordable private rental; social housing; and specific housing for Aboriginal, disability and homelessness needs.

It can be done; it has been done before. In 1945, Australia also faced a housing crisis. Despite skills and materials shortages and the financial difficulties of the post-war economy, the Commonwealth built 670,000 homes in ten years.

Decent housing underpins jobs, growth and productivity. Well-located, affordable housing is critical for preventative health, to provide a stable home environment for education and self-confidence, and for a productive workforce.

We need a national program of home building to meet the shortfall in all forms of housing. While this will not in itself resolve all problems, it is critical to a successful housing policy.

How much will it cost and where’s the money?

This is the subject of a new research report, Towards a National Housing Strategy, by Compass Housing working with a group of peak bodies, housing academics and community housing providers.

To get the long-term benefits of decent housing, we must recognise that providing this has an up-front cost and we are in a tight fiscal environment. The Ache for Home Report estimates a A$10 billion housing bond could meet the needs of the 100,000 currently homeless people. Across all tenures, Australia could build 500,000 homes in ten years for an annual investment of $12.5 billion.

Even if the Commonwealth government took full responsibility for funding a national building program of such scale, the annual investment would equate to less than one-fifth of the current annual cost of capital gains (CGT) exemption on the main residence. The bonus of investment on such a scale could be the boost to the wider economy in which each $1 spent on construction created a $1.30 gain.

A national housing strategy would need to do two key things to raise the cash needed:

rebalance current tax settings to redirect money to where it is most needed; and

revise fiscal settings to attract more private capital into housing.

Innovative financial models have been developed internationally that can bring private finance to the table. The development of an arm’s length, government-funded financial intermediary to provide loan guarantees within a housing bond approach is one model with merit. It is used in the UK, the US and Europe.

Rebalancing subsidy arrangements across housing sectors means ring-fencing current housing support and redirecting it across the housing system. Reforms of capital gains tax exemptions and discounts, as well as negative-gearing concessions, are contentious, but are levers to improve housing supply.

Negative gearing amounts to an average saving of $2,900 per year for the 1.2 million who claim. However, its impact on the budget means it costs the remaining Australians $310 per year each in tax that they would not otherwise need to pay.

Across these subsidies alone, a modest redirection would provide for a significant start-up fund for affordable housing, to be leveraged with private investment funds.

A national bipartisan approach would allow an independent review of all subsidies and recommend rebalancing options. It could also ease financial stress in the private rental sector by examining the current caps and levels of Commonwealth Rent Assistance to improve prospects for the many families where renting is a lifetime housing solution.

Without a national, integrated approach to housing, Australia will by default continue the mistakes associated with seeing the four sectors of the housing continuum as discrete and conditioned by different factors.

While I agree with the thrust of this article, the biggest problem I see when it comes to housing policy is the separation of responsibilities and vertical fiscal imbalances between the Commonwealth and States.

The Commonwealth controls broad tax settings and immigration policy, whereas the states control land supply, planning and actual service delivery.

Advertisement

Accordingly, we have a dysfunctional situation at present whereby the Commonwealth has juiced housing demand by: 1) maintaining perverse tax rules (e.g. negative gearing and the CGT discount) that encourages excessive investor speculation into existing dwellings; and 2) maintaining very high levels of immigration.

Meanwhile, the cash-strapped states, who receive only a small share of the total tax take, have locked-up land supply, tightened planning, and under-invested in infrastructure partly because they cannot afford to fund the growth thrust upon them by the Commonwealth.

The end result is a housing system that is failing because of too much demand pushing-up against supply-side barriers, leading to escalating housing costs (both prices and rents).

Advertisement

While Labor, to their credit, has attempted reform at the taxation level via its proposed changes to negative gearing and the CGT discount, it does not go nearly far enough.

What Australia needs is the federal government to take the lead on the supply-side as well, to ensure that the states are both willing and able to cope with the population expansion thrust upon them by the Commonwealth, so that they can deliver affordable housing supply connected by good infrastructure.

There are many ways to skin the housing cat. As noted previously, the federal government could offer incentive payments to the states to free-up land supply, relax planning, and build housing-related infrastructure. Again, it is the federal government that has decided to run a high immigration program, so the least it should do is provide the states – the ones primarily responsible for service delivery and infrastructure – with the means to cope with this growth.

Advertisement

Ultimately, the best way to overcome the states’ reluctance to boost supply is to ‘show them the money’ and offer them incentive payments in return for genuine supply-side reforms.

Most importantly, the “First-User-Pays-All Model” used to fund housing-related infrastructure must go. The First-User-Pays-All Model works as follows:

Developers are forced to provide the long lasting housing infrastructure that largely benefits the entire community;

Developers then dump almost the entire cost on the first user of the land (usually a first home buyer), who then tries to pay for it with a jumbo-sized mortgage, much of which our banks borrow offshore;

Local and state councils are then motivated to try to load as much expense on the home buyer as possible, and often also whack on a nice assortment of fat levies and contributions as well;

The end result is a system that encourages gold plating and over charging when bringing land to market and forces the most vulnerable and less financially secure people pay the cost with hundreds of billions of foreign debt that requires a taxpayer guarantee.

Advertisement

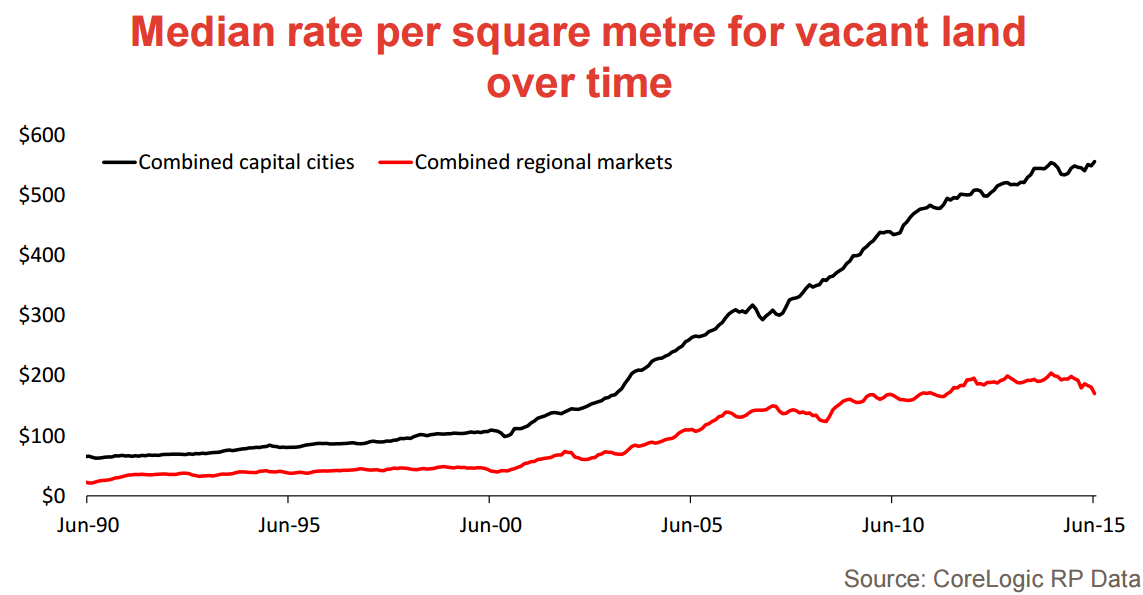

The First-User-Pays-All Model is a key reason why fringe lot values have experienced hyper-inflation over the past 15 years (see next chart). It is also why first home buyers are being gouged circa $600,000 to live in a basic 3 bedroom house on a tiny lot 50 kms from Sydney and why there is almost no-demand for expensive new housing like this unless interest rates stay close to zero.

One option for overcoming the First User Pays All model for financing development costs is for the federal government to pay the servicing and development costs of bringing the land to market and then recover part or all of the cost from rates or taxes on the land over the next 20-30 years (explained here and here).

Advertisement

The commonwealth could fund it directly via a Commonwealth Land Tax (which existed between 1910 until 1953) or have the state government collect it as rates and remit the required amount back to the federal government (or bond holder).

Alternatively, if the federal government remains reluctant to fund such vital infrastructure, it could instead set up a Municipal Utility bond model (explained here and here), like the one operating in Houston Texas, and then let the growing self-managed superannuation fund (SMSF) sector do the funding. The returns will be secure if the rates/taxes are a first charge on the property, and the SMSF industry is begging for simple secure long term investments that generate a steady return. In any event, the model certainly beats the current one whereby SMSFs are having a punt with retirement savings on the housing bubble through bank stocks and the like.

These are just two possible solutions out of many. The important thing is that the federal government stops ignoring the whole supply-side issue and takes a genuine leadership role, as well as providing the states with funding for growth.

Advertisement

New Zealand is currently showing Australia how it could be done, with broad political agreement now reached on freeing-up Auckland land supply (see here and here). The RBNZ deserves some credit, too, since it has placed intense pressure on policy makers to get their acts together on supply, shaming them into action and providing them with political cover. This is in stark contrast to the limp-wristed RBA, which chooses not to issue direct statements on housing affordability, thus giving our politicians a free pass.

In short, Australia desperately needs genuine leadership from the federal government to drive supply-side reform and improve housing affordability for the growing population. The feds control the lions share of the country’s revenue base and population (immigration) policy. Therefore, they simply cannot continue to bury their head in the sand and blame the states.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.