The Reserve Bank of Australia (RBA) released a Bulletin article yesterday examining household wealth using evidence from the 2014 Household, Income and Labour Dynamics in Australia (HILDA) survey.

This survey showed that the average Aussie household had a total wealth of around $740,000 in 2014, although housing accounted for 60% of total household assets. Below are some key extracts from this report:

The HILDA Survey data suggest that the average Australian household had total wealth of around $740 000 in 2014…

Housing is the largest asset class on Australian households’ balance sheets, accounting for around 60 per cent of total assets…

Looking more closely across the states reveals large differences in the mean and median values of housing assets (Graph 5)…

…

Overall, around 66 per cent of all households in Australia own their primary place of residence and 20 per cent of households own other property (including investment property). Similar to previous surveys, home ownership typically increases with income, wealth and age (until retirement), and ownership of other property was highest for households where the household head is aged 45 to 64 years…

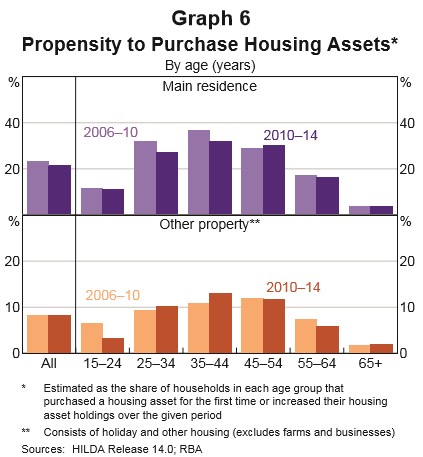

The data also allow analysis on which households entered the housing market or increased their housing asset holdings between 2010 and 2014. This shows that the share of households that either became home owners for the first time or upgraded their main residence decreased relative to the 2006–10 period (Graph 6). This was particularly apparent for households aged 25 to 44 years. Households in this age range were more likely to have increased their holdings of other property assets, while those aged 15 to 24 years were less likely to invest in other property than they were between 2006 and 2010 (Graph 6).

Although households aged between 55 and 64 years were also less likely to purchase housing assets over this period than over the previous four years, they remained the age group with the highest rates of property ownership and were the largest holders of housing assets. Households in New South Wales and Victoria were slightly more likely to increase their holdings of other property than was the case from 2006 to 2010…

Household Debt

The distribution of debt in Australia is highly skewed. High-income households hold the majority of debt. The top income quintile held almost 50 per cent of the stock of household debt in 2014. Almost a third of households held no debt, with the majority of these being retired households…

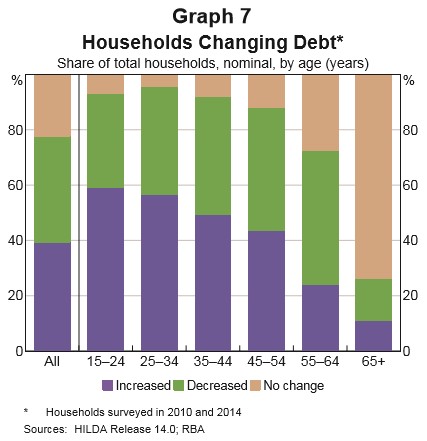

As was the case in previous surveys, younger households were more likely to have increased their debt levels than older households…

Property debt accounted for a little over 80 per cent of the stock of debt held by households in 2014…

Any foreigner looking at the $740,000 average household wealth figure in Australia could easily conclude that Aussies are very wealthy. But there is a huge caveat to this result.

First, according to IMF data, Australians along with their Kiwi cousins have a particularly high exposure to property and a lower share of wealth stored in liquid financial assets:

However, is having the lion’s share of one’s wealth stored in illiquid housing really all that beneficial? We all need somewhere to live and higher home values serve little purpose to the vast majority of owner-occupiers, who typically must sell and buy into the same market. Expensive housing also punishes those who have recently entered, or are yet to enter, the housing market, who are required to either take-out mega-mortgages and have a life of debt slavery, or miss-out altogether.

Would Australians really be worse-off if the median house capital city house price was $300,000 instead of $600,000, mortgage debt was 70% of disposable incomes instead of 134%, and the banking sector was smaller and less profitable?

The answer is obviously no. Lower debt loads would make households better-off, whereas the broader economy would benefit from the productivity-boosting effects of lower land prices, increased business lending (investment), and a more balanced economy.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

…