We at MacroBusiness were thrilled when Malcolm Turnbull took over as Prime Minister, believing that Australia now had a leader that would provide intelligent debate about economic policy, rather than the scaremongering tactics employed by Tony Abbott, which was clearly aimed at sealing the grey vote. Oh how we were wrong.

As noted also by Houses & Holes, Malcolm Turnbull has morphed into another Tony Abbott, but with a nicer suit, engaging in the mother of all scare campaigns against Labor’s proposed changes to negative gearing and the capital gains tax (CGT) discount, sounding the alarm that the value of Australian’s houses would fall (i.e. become more affordable):

The Labor Party’s negative gearing policy and its wind back on the capital gains discount, or its increase in tax on capital gains, is a very dangerous one. It has been very, very poorly thought out. The consequence of it will be a decline in property prices.

Every homeowner in Australia has a lot to fear from Bill Shorten.

…what Bill Shorten has done, he has set out to smash the residential housing market… That will lower the price of property… Bill Shorten is going to gnaw away at that equity. His policies will make your home worth less…

Bill Shorten’s policy is calculated to reduce the value of your home.

The parallels with former Prime Minister, Tony Abbott, are uncanny. Here’s what Abbott said in June 2015 in response to rumors that Labor was considering winding back property tax concessions:

“Millions of Australians have mortgages and the last thing they want to see is the decline in the value of their most important asset.

“(Mr Shorten) is someone who wants to be the prime minister of Australia and he wants your house to be worth less.

“Do not trust this man with your house price, do not trust this man with your superannuation, do not trust this man with your future and do not trust this man with the government of Australia because what he wants is your house to be worth less.”

The toxicity of Turnbull’s comments are evident on multiple levels.

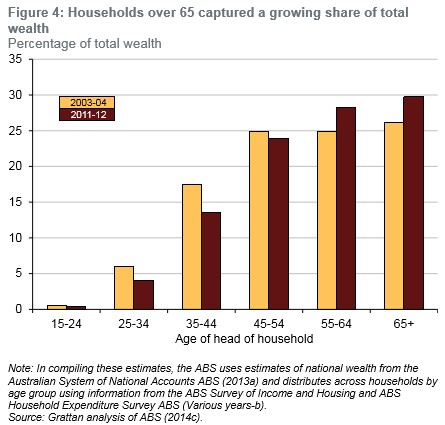

First, he has effectively endorsed the massive inter-generational transfer of wealth that has been occurring over the past 20 years, which has seen the lion’s share of wealth flow to older cohorts, whilst younger cohorts languish (see next chart).

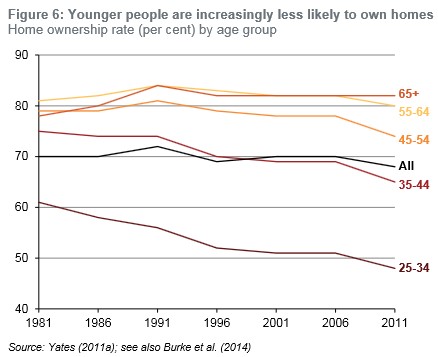

Turnbull has also effectively endorsed the declining levels of home ownership for younger Australians (see next chart).

And by ruling-out meaningful reform to Australia’s property tax concessions – the lion’s share of which flow to wealthier, older Australians – Turnbull has effectively ordered young renters to pay more and more tax so that they can fund the generous entitlements of their home-owning parents and grandparents.

However, Turnbull’s waging of inter-generational war is only example of his toxicity. Arguably, a bigger problem is the damage that will be done to the Australian economy from his penchant for ever-rising house prices.

The Australian economy is already badly unbalanced, with too much capital being channeled into unproductive land/housing and not enough into productive enterprise.

Fellow MB blogger, Cameron Murray, in 2012 estimated that a considerable slice of Australia’s declining multi-factor productivity has resulted from escalating land costs.

Land is a key input cost for most businesses. So when costs are inflated, it reduces the competitiveness of industry, making it harder for Australia to compete abroad. The associated higher housing costs also places upward pressure on wages.

For decades, resource allocation in Australia has been channeled away from the tradable sector and infrastructure investment towards the financial sector, as home buyers have taken on ever-bigger mortgages as they chased house prices higher.

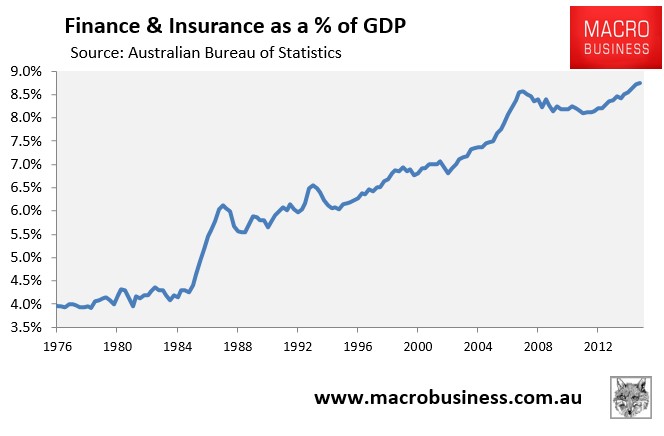

It should be no surprise, then, that the finance and insurance industries – which are dominated by mortgage lending – have grown at more than twice the pace of the rest of the economy since financial markets were deregulated in the mid-1980s, and now represent an all-time high share of the economy (see next chart).

Unfortunately, Australia’s productive economy has been collateral damage, effectively starved of credit as the housing obsession has steered banks away from business lending.

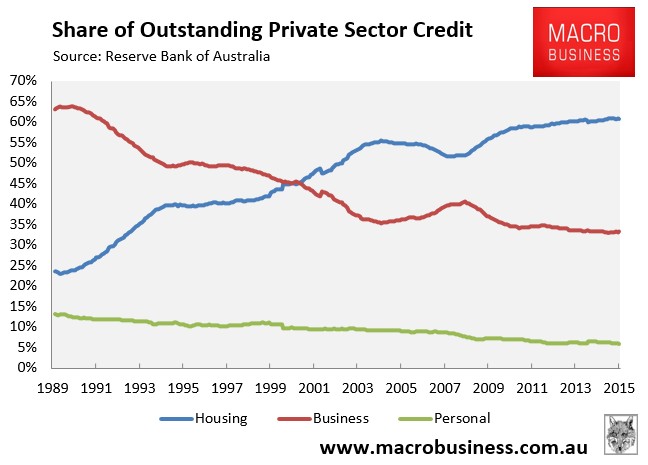

In the early 1990s, Australia’s banks lent nearly two-thirds to businesses, with the balance split between housing and personal lending. However, after the mid-1990s explosion of housing values, these ratios have reversed, with housing lending now at a record high share of total lending, whereas business lending is near an all-time low (see next chart).

A key contributor to this problem are Australia’s unique mix of tax expenditures, namely negative gearing and the CGT discount. These have increased the relative attractiveness of housing investment, significantly boosting speculative demand. The end result is too much of the nation’s capital tied-up in housing, which has chocked-off productive areas of the economy.

Indeed, in its its February Housing Market and Economic Update, Core Logic-RP Data valued Australia’s housing stock at a whopping $6.4 trillion, or around 4.0 times GDP.

But rather than address these policy distortions, as Labor has attempted to do, Prime Minister Turnbull has effectively embraced them with both hands, ruling-out meaningful reform whilst cheering house prices ever higher.

One can only wonder how Australia would have looked if the many billions of dollars of excess capital that has been poured into established housing had instead been funneled into businesses and infrastructure. Instead, Australia has been left with hollowed-out industries and an infrastructure deficit that will likely never be closed, made worse by rampant population growth (immigration).

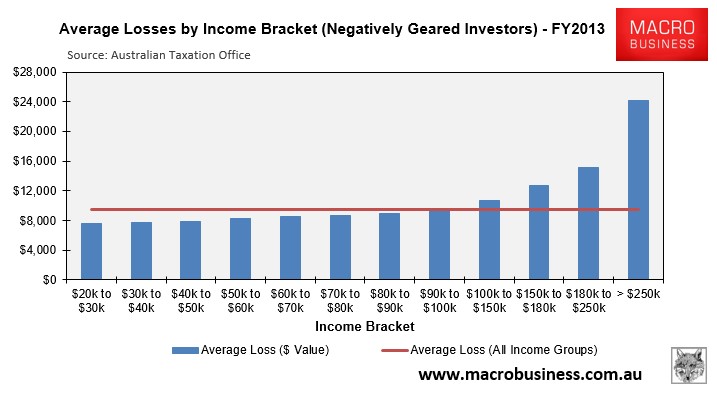

As reported in The Australian, over the weekend, the Turnbull Government is still considering applying a $20,000 annual cap on negative gearing deductions. However, the average negative gearing loss was around $9,600 in FY2013 (latest available data):

Therefore, any cap would need to be set at a much lower level, say $10,000 per annum, to have much impact on Budget revenue or equity. As it stands the $20,000 threshold would really only act as a fig leaf to cover ongoing rorting of the tax system.

Another shocking aspect of Turnbull’s scare campaign is that is seems to go against his personal views about negative gearing and the tax regime more generally.

In his 2005 tax policy paper, Turnbull described negative gearing and the CGT discount as a “sheltering tax haven” that is “skewing national investment away from wealth-creating pursuits, towards housing”, and has caused a “property bubble”. Turnbull also acknowledged that “Australia’s rules on negative gearing are very generous compared to many other countries” and that “the normal deductibility principles do not apply to negatively geared real estate such that the taxpayer is not obliged to demonstrate that the negatively geared property will generate positive cash flow at some point in the distant future”.

Moreover, in 2014 Turnbull acknowledged that the tax system favours richer older people over younger working Australians:

“Looking at Australia’s tax regime you would say that it is too tough on people earning income… but is incredibly concessional to older people who have made their money…

All of these areas are very hard to deal with because any change invariably… [leads them]… to become very angry. That’s why reform is very difficult…”

If Malcolm Turnbull had any integrity and backbone, he would back Labor’s reforms reforms to negative gearing and the CGT discount instead of running an Abbott-styled scare campaign in a cheap appeal to property owners’ selfishness.

The unfortunate truth is that Turnbull is no longer managing an economy but a property bubble.