The Mining GFC crisis deepened last night as rumoured US shale bankruptcies swept the market and stocks were pummeled -2.5% then rebounded some:

Those low 1800s support levels on the S&P500 do not look strong. US bonds were bid big and the short end of the curve is pricing out all further rate hikes now:

Advertisement

The US dollar was thus weak:

And commodity currencies stronger than they should have been:

But, oil fell hard anyway:

Advertisement

Though base metals went the other way on US dollar weakness:

As did gold which is threatening to bottom:

Advertisement

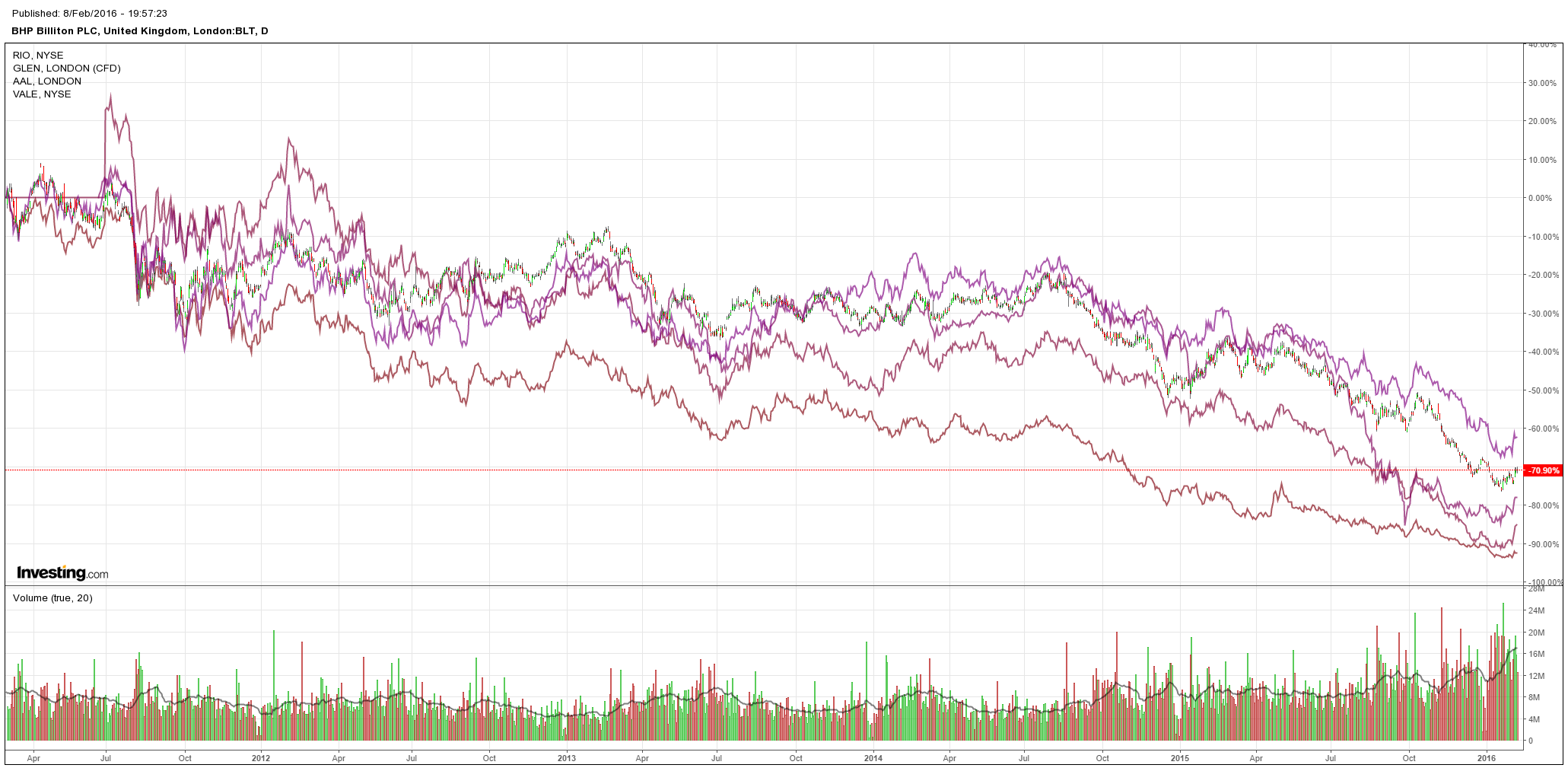

Which helped major miners:

But US high yield was crushed and EM is poised to break:

Advertisement

So, right now we have a developing tension between the growing realisation that the US tightening cycle is done and the ongoing rout in commodity production. We can expect this to continue for some time but I caution those that think now is the time to buy miners because the Fed is finished. JPM put is well last night:

While we earlier mentioned that negative nominal rates should affect the economy no differently than ordinary policy easing, there is some evidence that the exchange rate channel is particularly pronounced in the case of NIRP. The leadership role of the Federal Reserve in the global monetary system may lead to some hesitancy to engage in what may be uncomfortably close to a skirmish in the currency wars. Lastly, there is the political issue. To be sure, political concerns about NIRP are not unique to the Fed; presumably one reason central bankers abroad sought to limit the pass-through to retail depositors was to avoid pushback from the political establishment. Even so, it seems reasonable to judge that the Fed’s current political situation is more parlous than is the case among its overseas counterparts. For all of the above reasons, we believe the hurdle for NIRP in the US is quite high, and we would need to see recession-like conditions before the Fed seriously considered this option.

Exactly. There is a big difference between not tightening and actually easing and with other central banks still experimenting with negative rates and seeing backfires the concern over quantitative failure is still alive and well too. Finally, the US is only the leading edge of the global bust. Emerging markets are the main game and remain in big trouble.

Advertisement

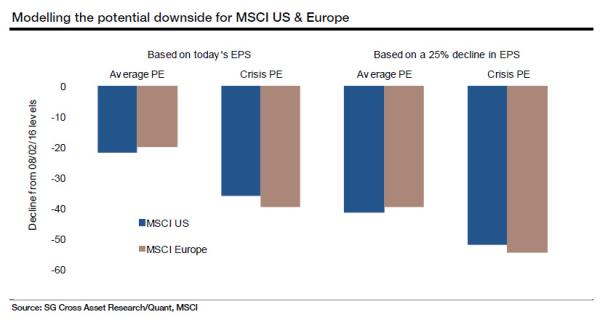

How low would share markets have to sink to trigger a full Fed response? Soc Gen:

…in the chart below reproduced from last week’s risk premia note we look at the potential downside if MSCI US & Europe were to mean revert to their average P/E since 1970. This equates to 14.7x for the MSCI US and 13.3x for the MSCI Europe based on operating EPS as defined by MSCI.

We also look to see what the decline would be if we went back to crisis reported P/E multiples, which we put at roughly 12x for the US and 10x for Europe (though both have been much lower). These types of declines would leave indices down rough 60-65% from peak, and would send leverage ratios skyrocketing.

I’m not that bearish but the potential downside in an end-of-cycle event is still large.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.