Last night the Mining GFC ran smack into worries about quantitative failure. From RBS:

Seeing relief off lows but fading again, as thematically we just saw essentially ‘the’ crowded ’15 macro trades come unglued on obvious unwinds: long stocks (SPX -1.3%, Estoxx -2.3%), long HY (HYG -0.2%), long Dollar (DXY -1.4%), short UST (+0.4%), short VIX (+6.5%), short crude (+5.1%), short Euro (+1.4%) / Yen (+1.8%) / EMFX (+0.5%), short copper (+1.9%)…all going wrong-way.

Plenty of attribution going around, first being portfolio de-risking as performance for active-types (read: humans) has just been brutal.

Others are re-treading the idea of ‘petro-state’ selling of liquid assets in light of the crude harsh fade from just 5 days ago. I would posit that the violence (“price insensitive”) and synchronized nature of it looked quantitative in nature.

Single-stock world shows somewhat similar picture as broad macro, with popular shorts and longs trading-backwards generally speaking, although pockets of shorts continue being pressed. Check-it:

The mixed-bag on equities short-side could be rationalized: some leveraged players outright taking grosses down by selling longs and covering shorts; while others are focused on taking net exposure lower, selling longs but adding selectively to shorts.

Lousy US data (weakish services ISM and average ADP employment report) combined with dovish comments from Fed member William Dudley to trigger a rout in the US dollar:

Advertisement

Oil roared despite weak data:

Base metals rocketed:

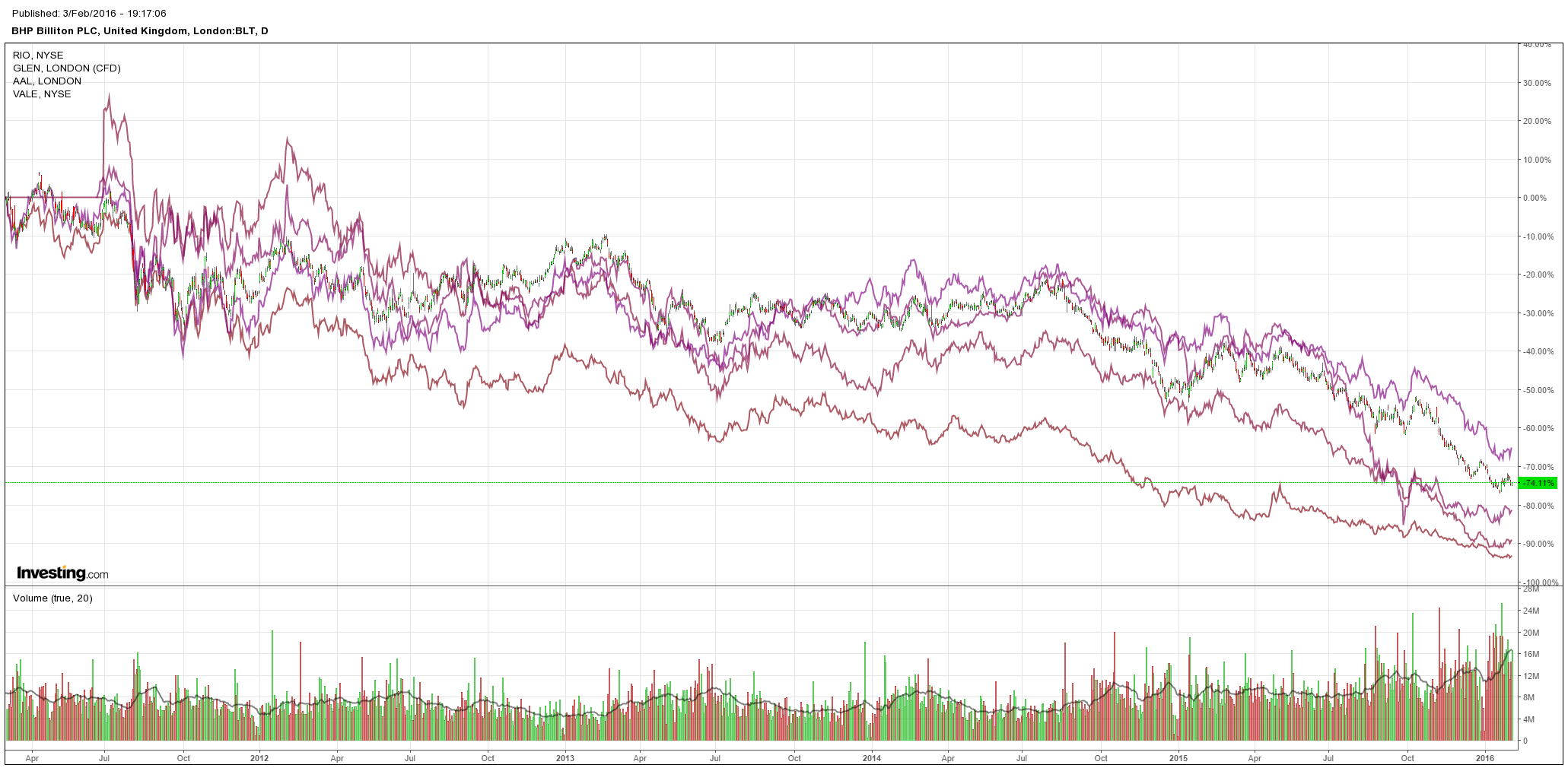

Miners caught a weak bid:

Advertisement

Commodity currencies launched:

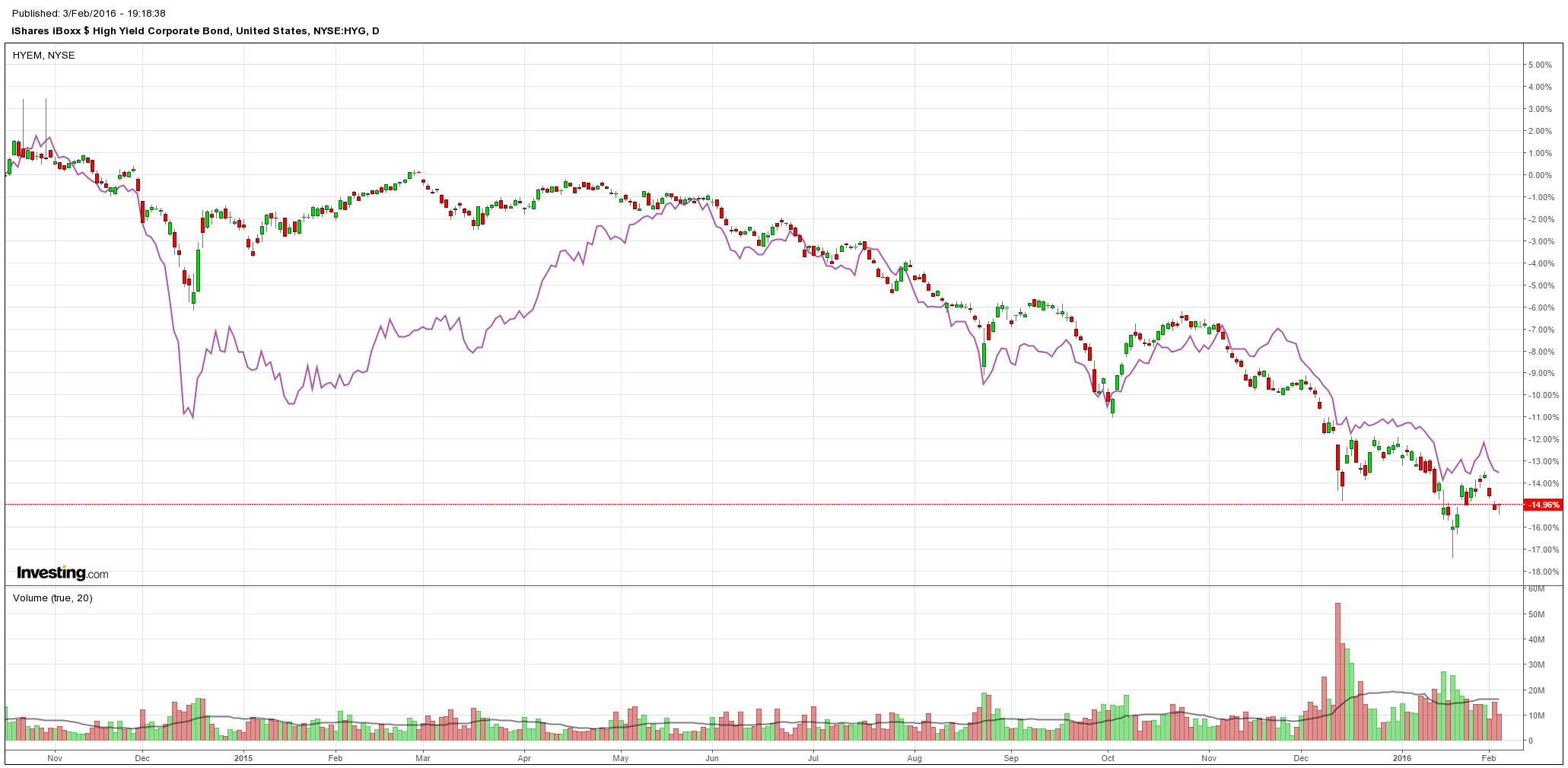

High yield rallied modestly in the US but not in EM:

Advertisement

And US bond yields crashed again with the 2 year beginning to price out any further rate hike:

So, that part is relatively straight forward. Markets are pricing a reversal of FOMC hawkishness.

Advertisement

But, stocks decoupled from the Mining GFC reversal and were flat or falling instead of powering upwards as you’d expect:

The cause appears to be that global banks (and central banks) are now caught in a growing whirlwind of their own. Credit risk is soaring across the developed world as worries deepen about where the Mining GFC will blow back into banks. As well, with negative interest rates now the Monetarist’s panic de jour, markets are doubting the efficacy of central banks to actually fix anything, from Macro Man:

Advertisement

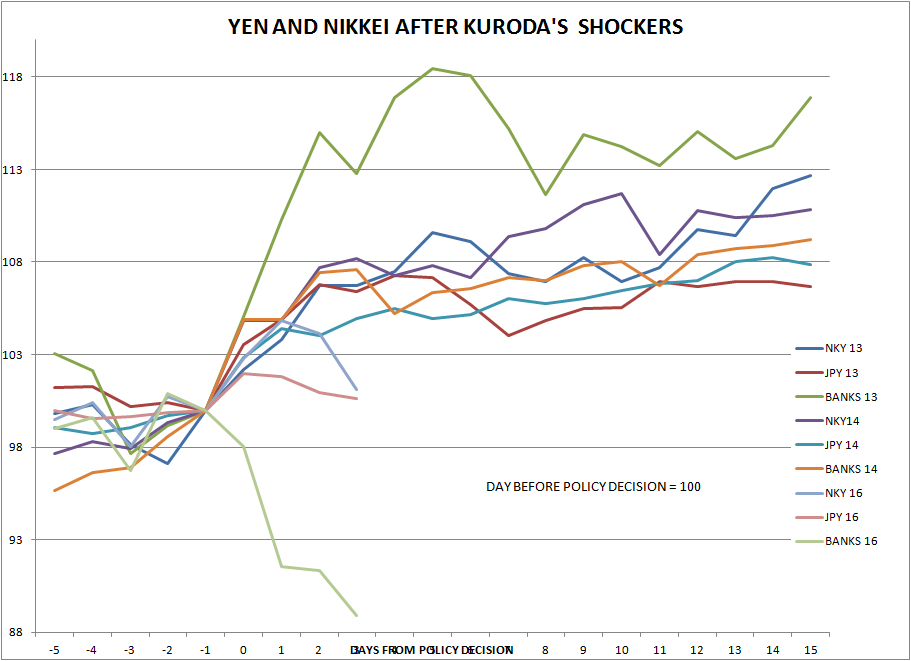

Kuroda and the rest of the NIRPsters ought to fire their screenwriters, because markets are not playing out according to the script. Although the Nikkei and USD/JPY are still higher than they were before last Friday’s BOJ announcement, the same cannot be said for Japanese banks, which have tumbled further since Macro Man highlighted them on Monday. It’s quite a contrast, really: banks were the star performer after QQE 1, generated middle-of-the-pack gains after QQE2, and are a steaming pile of dog dirt this time around. Although perhaps not conclusive, it is nevertheless persuasive evidence of how the market views the impact of negative rates.

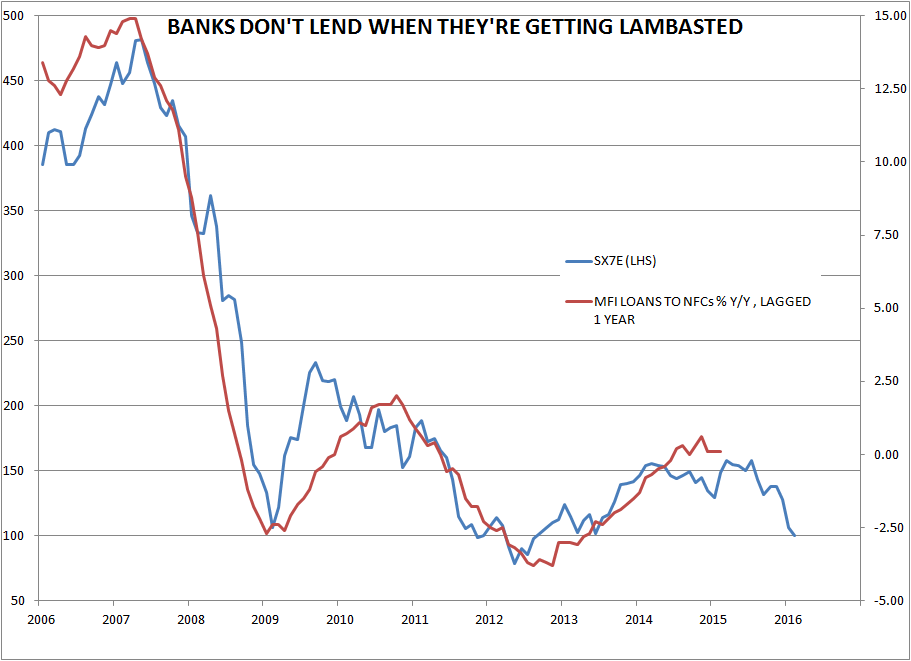

After QQE versions 1 and 2, USD/JPY rallied forthwith and never came close to touching its pre-announcement levels. This time around, both the yen and the Nikkei have retraced sharply, and it seems only a matter of time before last Thursday’s levels are reached and breached. Indeed, it’s looking increasingly like Kuroda’s gambit may have been the opportunity to get short USD/JPY as alluded to last week.Not that the pain is confined to Japan, of course. The SX7E plunged to a new low yesterday as markets are coming perilously close to entering “DB deathwatch” mode. Macro Man has yet to hear any rumours of counterparties failing to take DB’s name, though in fairness he is not in the best place to be cognizant of them even if they are there.In any event, yesterday the SX7E broke 100 for the first time since July 2013, which might be notable if every other banking index weren’t also tumbling including that in the US. If Macro Man has done his sums correctly, something like 10% of the stock of global government debt currently offers a negative yield. Given the regulatory incentive to hold these securities (which surely outweighs the monetary incentive to sell them), is it any wonder banks are getting crushed, beyond the margin considerations raised yesterday?

Naturally, as is so often the case, the micro-incentives faced by economic actors in the real world fall outside of the models espoused by policy-making theoreticians. The bitter experience of the last several decades has demonstrated that these externalities usually bear negative consequences.

Although the academic and policy-making tide appears to be firmly in favour of NIRP at the moment, Macro Man cannot help wonder if at some point economists will ask not whether the US can afford to have modestly positive short rates….but whether Europe and the rest of the world can afford not to?

Quite right. The Mining GFC has run into quantitative failure. Liquidity is abundant but there nothing in which to invest. Dangerous territory.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.