One could be forgiven for thinking thus. Oil is flying, iron ore soaring, base metals powering, charts have double bottoms. It’s all good! The US dollar was down hard again last night:

As bonds continued to price out Fed hikes:

Advertisement

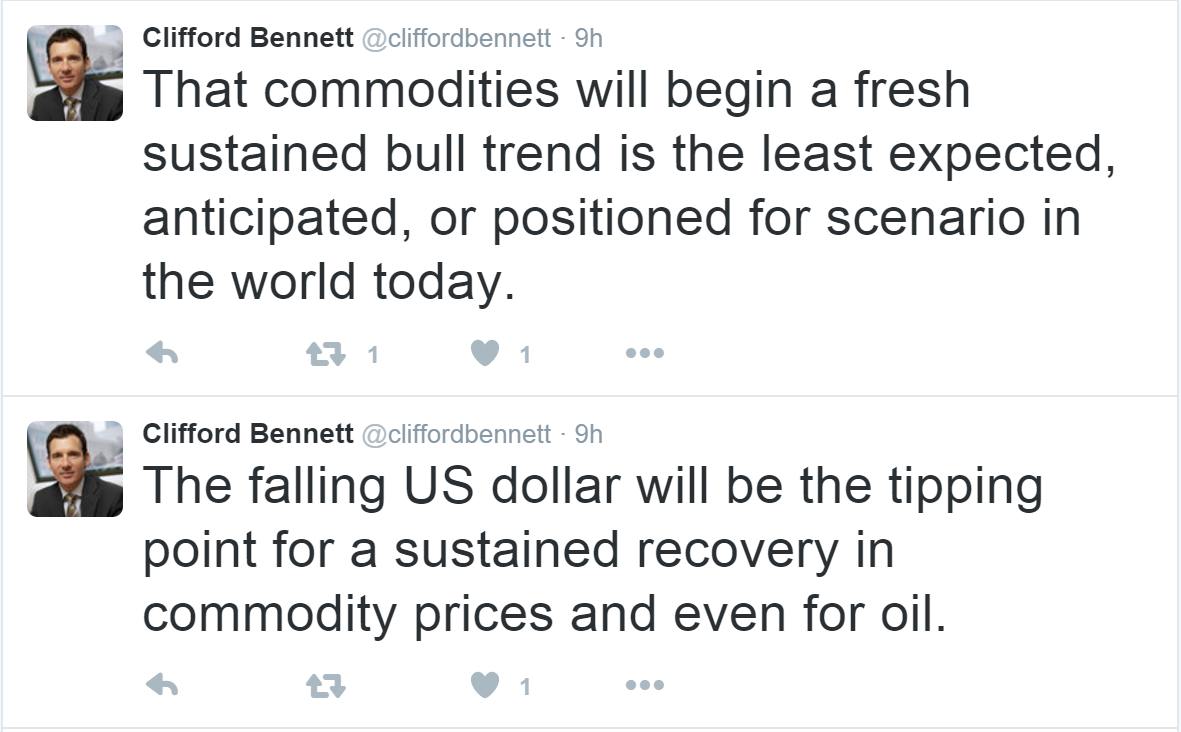

And commodity currencies soared:

Oil disappointed:

But base metals flew:

Advertisement

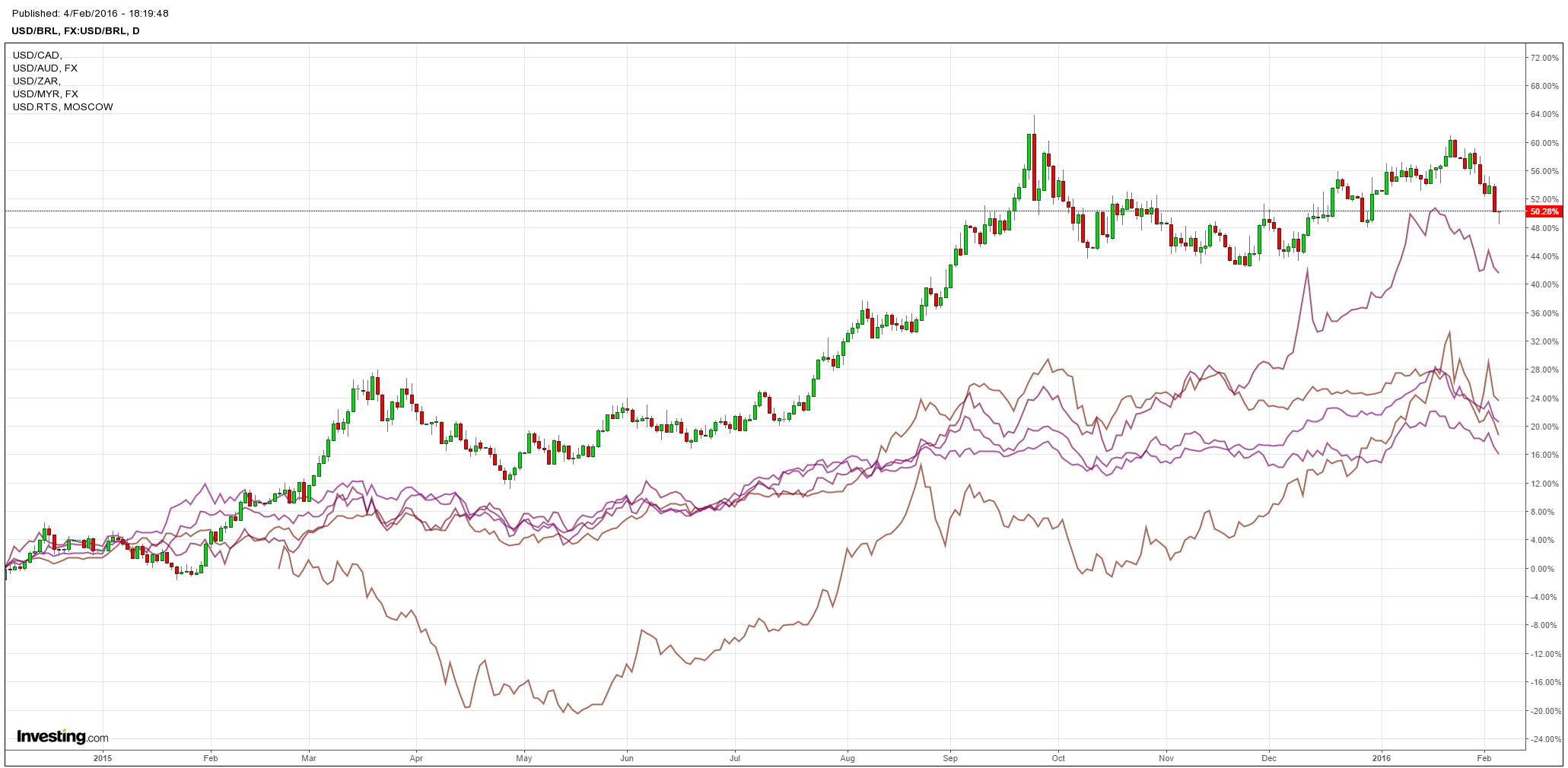

Big miners went wow!

But high yield debt fell:

So, with an easing back Fed and falling US dollar are we finally at an end to great commodities crash?

Advertisement

I remain unconvinced. The other major driver is falling Chinese demand and it will persist this year as iron ore demand falls as much as 60mt and supply expands 40mt in an already 100mt oversupplied market. Coal and LNG are much the same.

But that is no longer the central story for the commodities crash. The US is now an equal risk with China.

Oil is the main game and it is still unlikely that it has bottomed either. Markets are rallying on an incipient shift in the Fed to a neutral policy setting but it is helpless on oil because the only thing that can end its rout is lower prices to knock out supply and all the Fed can do is raise them, as we’ve seen in recent days.

Advertisement

So, the oil rally will flame out soon enough, indeed may have already. OPEC is at war with itself and low cost producers will not hand market share to higher. US shale is the marginal cost producer and can now expand at $50. But that’s all-in costs. At cash costs, with existing wells, it is $20 lower. A sustained period in the mid $20s will be needed to shut the US junk bond market for long enough that production tumbles.

The risk in this remains that the shakeout will be long and disorderly enough that the US stock market sinks along with its junk bond market. That in turn will disrupt consumers and wider activity and oil demand will falter, sending it into a price death spiral. From BofAML:

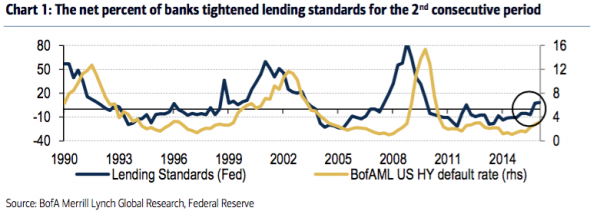

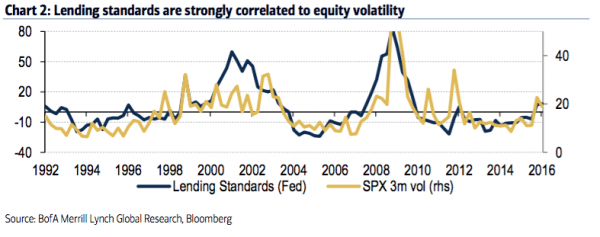

We have said in the past that companies don’t default because of impending maturities- in fact in 2001 and 2007, the maturity wall was just as benign as it is today. Issuers default because at some point in the credit cycle their access to funding dries up; case in point, the two best leading indicators of future default rates are C&I lending (Chart 1) and CCC issuer access to the primary markets. Troubling, we’ve written about how CCC access to the HY primary market has been in a cyclical decline since 2013 and breached an ominous threshold last year. Perhaps even more worrisome is the data coming out of the C&I lending survey which polls regional banks on their lending standards to small and medium enterprises. The Q3 survey showed that for the first time since the recession, a net higher number of regional banks are tightening their lending standards vs loosening them. A fresh update released by the Fed on Monday confirmed our fears that we are in the throes of a trend, as regional banks yanked the leash tighter in what now amounts to be two quarters of tightening in a row. Never before have we had two consecutive quarters where banks increasingly tightened lending standards without it ultimately leading to a recession.

Mounting default losses in the Oil & Gas sector is likely forcing banks to increase loss provisions against their exposure. The amount of direct exposure US banks have to energy companies through bilateral loans currently stands at $80bn which on average represents 5% of total loans on banks’ books. Indirect exposure is even more as there is a discernable spillover effect to banks’ non-energy portfolios too (e.g. real estate and business loans in energy dependent markets). And if history is any indication, we are only in the early phases of loss provisioning for the sector.

Stress in financial markets leads to general risk aversion. Just as capital markets temper down during volatile times, it’s reasonable to assume banks responding the same way. Sure enough, C&I lending data show a very strong correlation to equity volatility. Since we expect to be living in a VUCA world for some time, there is no catalyst in sight that could flip this downward momentum. Combined with an already high regulatory hurdle for lending in the post- Volcker era, more and more banks could be forced to freeze credit going forward.

HY primary markets are all but shut except for very high quality issuers. And if this trend continues for a while (the probability of which in our opinion is very high), we could envision a world where enterprises, big and small, find it harder to acquire financing across all industries, leading to widespread defaults, even outside of commodities.

Advertisement

If US shale turns out to be less durable than my estimates then we may be able to avoid that worst case.

Either way, lower for longer is needed and the end will not come with a huge rally but a painful grind. This is a recipe for lower prices yet across the commodity complex given oil is a key input cost for all, and oversupplied commodity markets with falling costs by definition pass savings on to the customer. The iron law of commodity markets is the lowest marginal cost producer sets the price.

Remarkably enough, a hard landing in China is not even needed to push this along. It’s shift away from commodity-intensive growth is enough. And as commodity markets collapse, China’s terms of trade are absolutely booming, pumping up income growth for its growing consumers. As the world’s largest consumer of commodities it may turn out be the greatest winner of the crash.

Advertisement

It may, in fact, be the US that takes leadership of the great commodities collapse and until that risk is cleared we’re in just another bear market rally. BofAML puts it nicely:

NIRP in Eurozone and Japan crushing bank stocks (Quantitative Failure); Fed now admits dollar appreciation could have “significant consequences” for the economy; and thus weaker US non-manufacturing data signals end of US “splendid isolation” and unwind of trades based on “higher US growth/rates” (US dollar & FANG the last of the dominoes to drop).

US dollar-reversal sparking bear market rally in humiliated EM/commodities/resources; note even retail sales in HK down 8.5% YoY; should China FX reserves beat expectations on Sunday, we think a tactical rally is likely to be vicious.

We remain sellers into strength in coming weeks/months of risk assets at least until a coordinated and aggressive global policy response (e.g. Shanghai Accord) begins to reverse the deterioration in global profit expectations (currently heading sharply south – Chart 1) and credit conditions.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.