While all eyes today will be on the headline (“real”) GDP number for the September quarter, released as part of the national accounts, most commentators will once again ignore the much more important data on national income, which will very likely register another sizeable fall when measured in per capita terms.

I have explained previously why I believe that real GDP is a rubbish measure of economic well-being (here, here and here), and have argued that “economists’, the media’s, and the Government’s infatuation with GDP is one of the biggest shortcomings in macro-economics”.

Essentially, because real GDP measures volumes, Australia’s growth rate has been boosted significantly by the transition from the mining investment boom to an export boom as new mines have come on line.

However, mining investment is labour intensive, whereas exports employ few workers. Hence, overall GDP growth is being supported as mining-related workers lose their jobs, thus masking the structural adjustment underway.

Even worse, the increase in export volumes is lowering export prices, meaning that Australia is now selling more goods but at lower prices. Hence, profit margins are being crunched and national income – the important measure that more closely reflects well-being – is falling, despite ongoing rises in real GDP. The mines are also predominantly foreign-owned, which means that much of the profits from mining activities flow offshore.

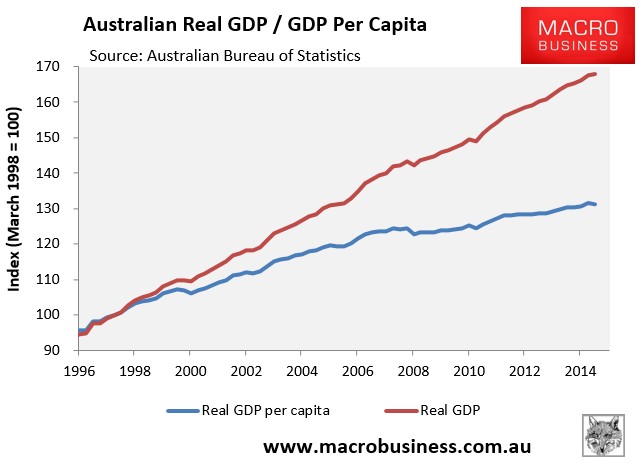

Of course, there is also the problematic convention of measuring GDP in aggregate, rather than on a per capita basis. This approach has led to spurious policies like the pursuit of endless population growth on the basis that it stimulates headline GDP (more inputs equals more outputs), even though it provides next to no benefits to everyone’s share of the economic pie, as measured by GDP per capita (see next chart), and likely reduces living standards of the pre-existing population.

So, what should we expect in today’s national accounts release for the June quarter?

Well, Westpac forecasts that headline GDP will bounce back hard on the back of rising commodity export volumes. It forecasts that September quarter GDP will grow by 0.9% over the quarter and by 2.3% year-on-year, with net exports contributing a whopping 1.5ppts over the quarter, partly offset by a fall in domestic demand of 0.7ppts.

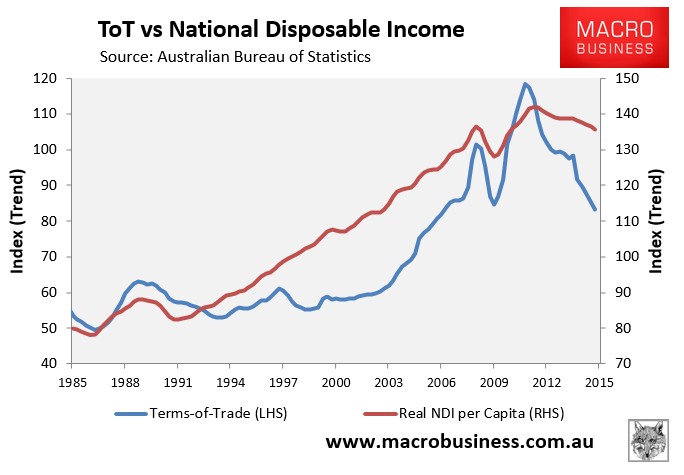

Regardless, the far more important measure of national disposable income (NDI) will once again be weighed down by the falling terms-of-trade.

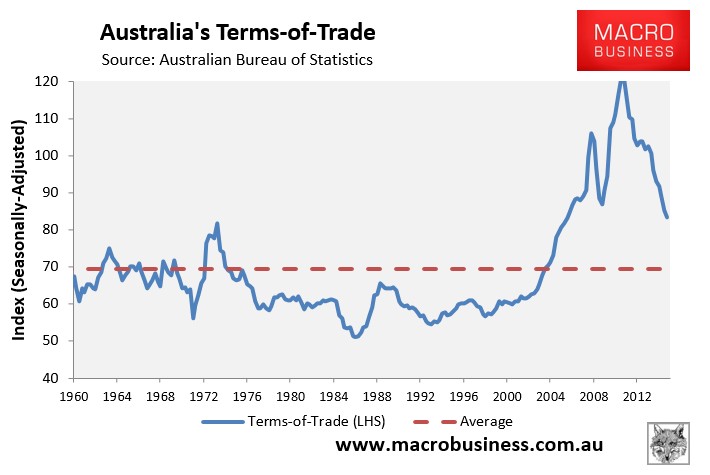

We know from yesterday’s Balance of Payments release that Australia’s terms-of-trade fell by 2.3% (seasonally adjusted) and 2.9% (trend) over the quarter to the lowest level in more than 9 years (see next chart).

The terms-of-trade is the biggest determinant of NDI (see below charts).

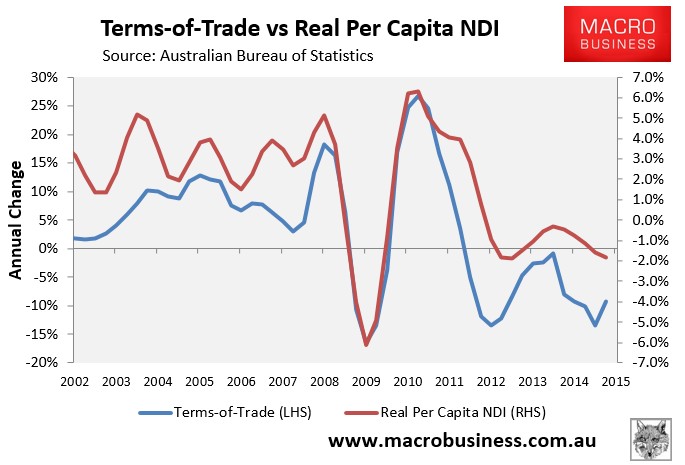

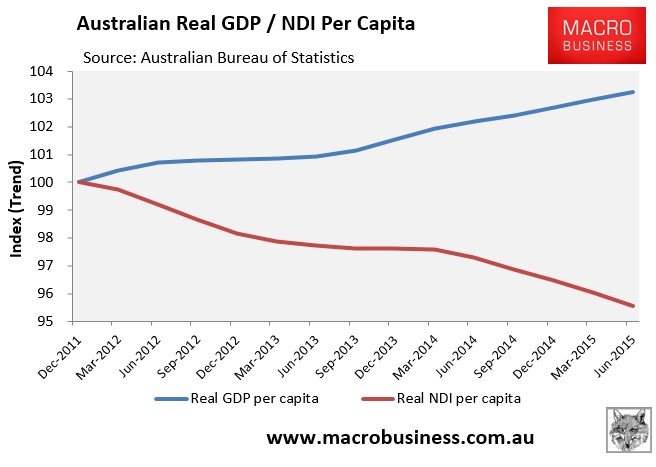

And is the fundamental reason why per capita NDI fell by 4.5% in the 14 quarters to June 2015, despite the 3.2% rise in real GDP per capita (see next chart).

And with Australia’s terms-of-trade still well above its historical average (see second chart above) and facing a multi-year adjustment downwards, the income recession that has already been in place for the past three-and-a-half years is set to continue, raising the prospect of Australia’s own “lost decade”.

This is the story that Australia’s economists, commentators and policy makers should be focusing on, not the meaningless growth in headline GDP, which is a very poor measure of Australian living standards.