The mining GFC has claimed another hefty scalp as it marches down the cost curve. This time, Brazil, from the WSJ:

Brazil’s recession deepened in the third quarter, with analysts saying it is the country’s worst economic crisis since the Great Depression, as political gridlock and a giant corruption scandal have halted investment and forced consumers to pare their spending to the bone.

Gross domestic product shrank 4.5% in the third quarter from a year earlier, the biggest contraction since Brazil started measuring GDP using the current system in 1996, Brazil’s statistics agency said Tuesday. The figures were dismal across the board and have already led economists to cut their forecasts for 2016.

“That report reads like an obituary,” said Andre Perfeito, chief economist at Gradual Investimentos in São Paulo. “There were no positive signals in this for the Brazilian economy in the next few quarters, and we still can’t say we’ve hit bottom.” Mr. Perfeito added that he cut his GDP forecast for next year to a contraction of 3% from 2%.

Much of the slowdown can be pinned on a political crisis that has stalled the passage of austerity measures in Congress needed to shore up Brazil’s fast-deteriorating finances.

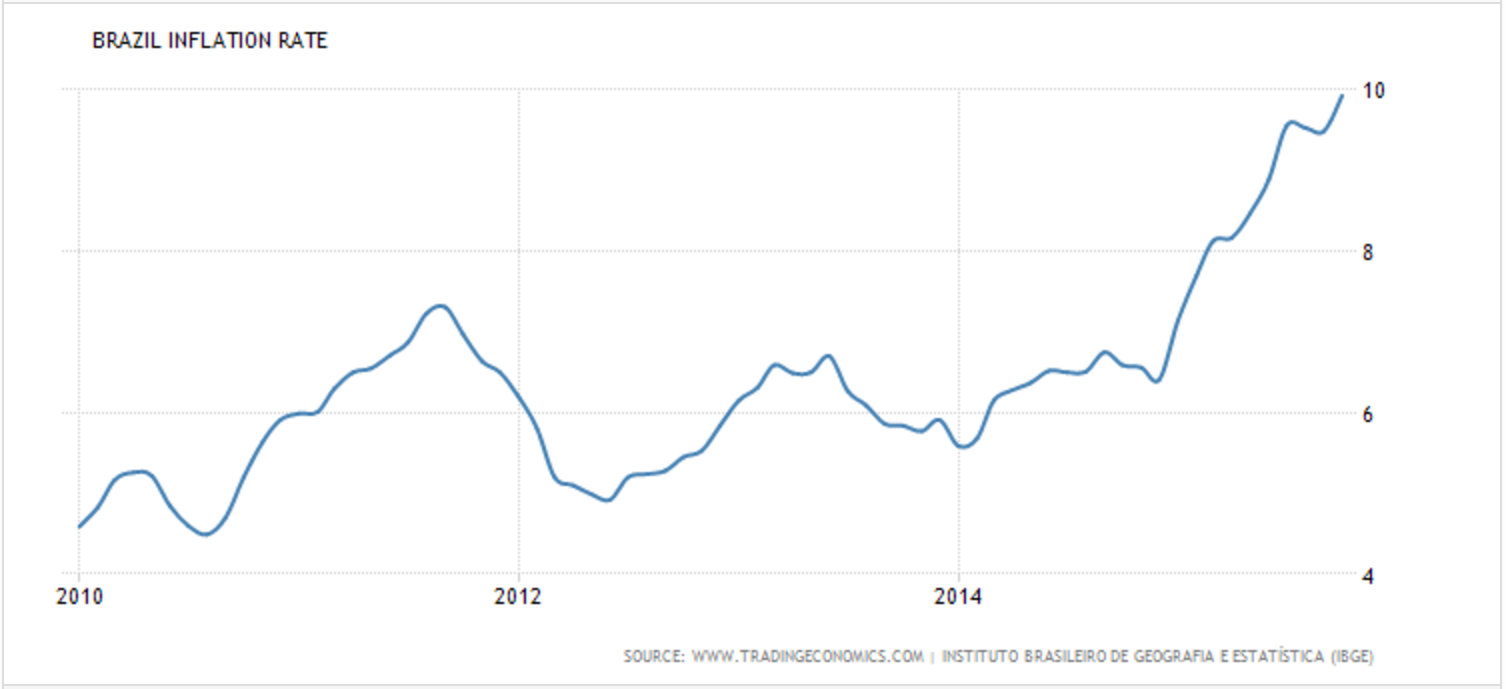

So the Brazilian economy is entering a depression because the government can’t cut spending fast enough? That’s a pretty perverse reading of events. The problem is not a lack of austerity, this is a classic capital run on an externally funded and over-indebted emerging market hit by an external shock. The real has collapsed driving inflation wild:

And pushing the central bank to tighten monetary policy in a pro-cyclical manner right into the bust:

That has led to the following, from Goldman:

Private consumption has now declined for three consecutive quarters (at an average quarterly rate of -8.5% qoq sa, annualized), and investment spending for nine consecutive quarters (at an average rate of -10.0% qoq sa, annualized). Overall, gross fixed investment declined by a cumulative 21% from 2Q2013. The declining capital stock of the economy (declining capital-labor ratio) hurts productivity growth and limits even further potential GDP. The sharp contraction of real activity during 3Q was broad-based: both on the supply and final demand side. Final domestic demand weakened sharply during 3Q2015 (-1.7% qoq sa and -6.0% yoy) with private consumption down 1.5% qoq sa (-4.5% yoy) and gross fixed investment down 4.0% qoq sa (-15.0% yoy). Finally, on the supply side, we highlight that the large labor intensive services sector retrenched again at the margin (-1.0% qoq sa; -2.9% yoy).

…What started as a recession driven by the adjustment needs of an economy that accumulated large macro imbalances is now mutating into an outright economic depression given the deep contraction of domestic demand.

It is only going to get worse, as well, as commodities keep falling and the US dollar keeps rising, rendering Brazil’s external private sector debts unserviceable. Brazil is a definite candidate for accelerated mining GFC debt contagion.

There is a warning in this for Australia on two fronts. First, if Brazil’s private sector is to default on US dollar loans then it will spread mining GFC debt contagion and raise funding costs for similar economies. Second, the dynamics afoot in Brazil are a difference in degree not kind to what is possible for Australia if that contagion were to reach our shores. The cost of borrowing for both the Federal Budget and our banks would rise as mining debt froze, leading to a crashing dollar, sovereign downgrades and inhibited monetary policy.

I am not saying that Australia will experience an outright current account crisis but some form of shakeout of that nature is quite possible.