The Bank for International Settlements (BIS) – the central banks’ central bank – has released a research note arguing that the fall in oil prices cannot be blamed solely on falling demand and rising supplies, but also debt and futures trading:

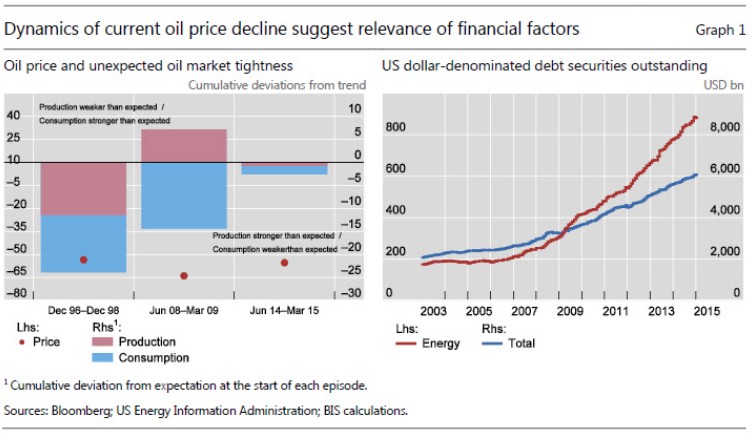

One important new element [contributing to falling oil prices] is the substantial increase in debt borne by the oil sector in recent years. The greater willingness of investors to lend against oil reserves and revenue has enabled oil firms to borrow large amounts in a period when debt levels have increased more broadly. Issuance by energy firms of both investment grade and high-yield bonds has far outpaced the already substantial overall issuance of debt securities (Graph 1, right-hand panel).

The BIS argues that the huge increase in debt in the oil sector has exposed producers to solvency and liquidity risks, and in turn added to price volatility:

Lower prices tend to reduce the value of oil assets that back the debt.

…a fall in the price of oil weakens the balance sheets of producers and tightens credit conditions, potentially exacerbating the price drop as a result of sales of oil assets (for example, more production is sold forward). Second, in flow terms, a lower price of oil reduces cash flows and increases the risk of liquidity shortfalls in which firms are unable to meet interest payments. Debt service requirements may induce continued physical production of oil to maintain cash flows, delaying the reduction in supply in the market…

The build-up of debt in the oil sector is a reminder that high debt levels can induce significant macro-financial interactions. Such interactions need to be understood better in order fully to appreciate the macroeconomic impact of falling oil prices.

Advertisement

It’s worth pointing-out that the phenomenon described above is not confined to the oil sector, but runs the gamut of commodities. For example, for years we have read about speculation in the copper market driving price volatility, along with coal producers accepting unpalatable take or pay contracts, which have prevented supplies from falling in line with prices.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.