John Roskam, executive director of the Institute of Public Affairs, has penned a piece in The AFR today debunking the “myth” that Australia is a low taxing country, and arguing that the only true tax reform is one that cuts taxes:

It is a myth that Australia is a low-tax country, because we’re not…

The claim that Australia is a “low-tax” country is based on data collected and presented by the Paris-based Organisation for Economic Co-operation and Development (OECD)…

When the OECD calculates taxes in Australia, it includes taxes collected by local, state and federal governments. However, compulsory superannuation contributions paid by employers are not counted as taxes, nor are the private health insurance premiums Australians are required to pay… In contrast, the OECD does count as taxes in other countries the amounts paid through the tax system to fund retirement benefits…

When superannuation and health insurance are counted as taxes, Australia’s tax-to-GDP ratio starts to look very different…

If superannuation and health insurance are counted as taxes, Australia’s tax-to-GDP ratio in 2012 was 33.5 per cent. That’s at a lot closer to the OECD average of 33.7 per cent than the figure of 27.3 per cent that got all the publicity…

The only reform worth talking about is that which cuts the overall tax burden…

For the record, I agree with Roskam’s critique of the OECD’s figures showing that Australia is a “low taxing” country.

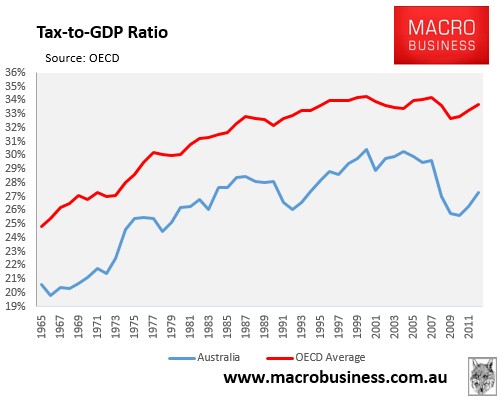

According to this data, Australia’s tax-to-GDP ratio of 27.3% in 2012 was the equal fourth lowest in the OECD, and well below the 33.7% OECD average (see next chart).

Advertisement

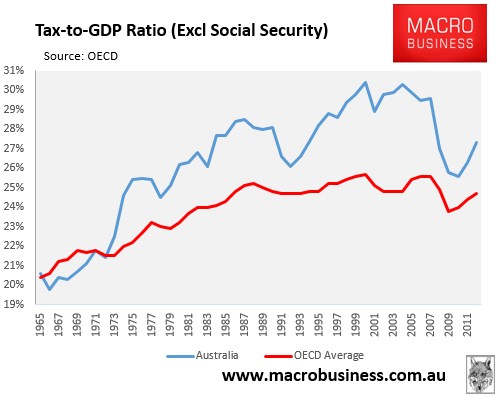

However, if social security is excluded from the tax-to-GDP measure, as Roskam thinks it should be, then Australia’s tax-to-GDP ratio of 27.3% in 2012 is actually above the OECD average of 24.7%, and has been above the OECD average for the entire period since the election of the Whitlam government (see next chart).

Advertisement

Given that Europe’s compulsory social security levies work in a similar manner to Australia’s superannuation system, then there is a legitimate argument that they should be excluded from any tax-to-GDP measurement for comparison purposes.

That said, I don’t necessarily agree that Australia’s tax take is too high. Tax revenue is required to fund the public services that the community both expects and needs. And I personally wouldn’t care if taxes were increased a little if it meant important social programs remained (or were expanded), along with the provision of well-targeted infrastructure.

Of primary importance is ensuring that the tax base is broadened and based on efficient and equitable sources. And this is where Australia’s tax system is failing.

Advertisement

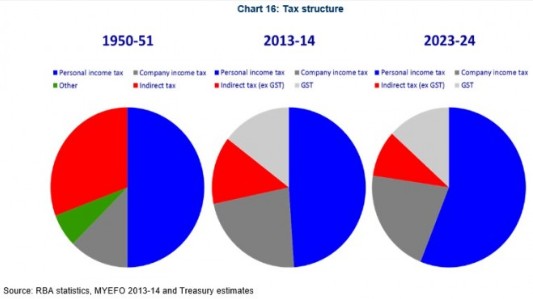

As highlighted frequently by the Australian Treasury, Australia’s tax system is becoming increasingly narrow and overly reliant on personal income taxes – precisely what you do not want as the population ages and the share of workers in the economy is forecast to shrink.

Under current taxation arrangements, the share of total federal budget revenue raised via personal income tax is forecast by the Treasury to rise inexorably over the coming decade, whilst the take from company taxes, indirect taxes, and the GST will shrink (see next chart).

Advertisement

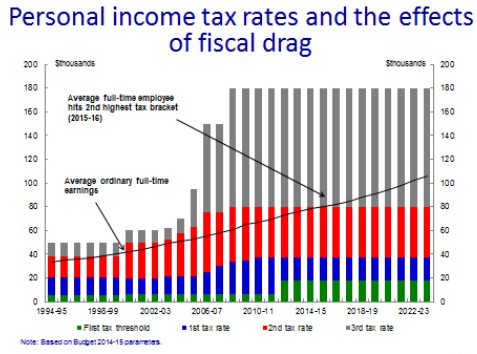

As noted in recent speeches by former Treasury Secretary, Dr Martin Parkinson, bracket creep will adversely impact workers across the income spectrum, but lower income earners in particular:

Fiscal drag [bracket creep] will pull someone on average full-time earnings into the 37 per cent tax bracket from 2015-16, and will increase the average tax rate faced by a taxpayer earning the projected average from 23 to 28 per cent by 2024-25 — an increase in their tax burden of almost a quarter.

If fiscal drag is not periodically returned in the form of personal income tax cuts, it can reduce incentives for workforce participation at low levels of income, and increase incentives for tax minimisation at higher levels of income.

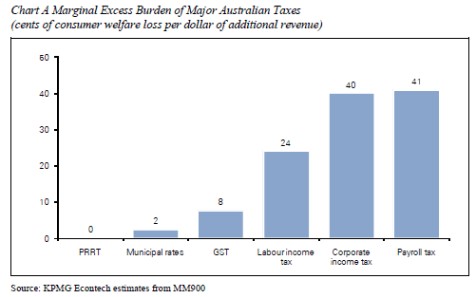

Further, as the Henry Tax Reviewshowed, personal taxes have a relatively high “marginal excess burden” (i.e. a big loss in consumer welfare relative to the net gain in government revenue). This is partly because they discourage work, leading to lower labour force participation, as well as encourage inefficient tax avoidance activities.

Advertisement

By comparison, indirect taxes, the GST, and taxes on land and resources have much smaller marginal excess burdens, and would therefore confer productivity gains to the economy if the tax base was shifted away from productive enterprise and onto these sources, along with adequate compensation for the poor (in the case of raising/broadening the GST).

Reform of this nature would also broaden the tax base – since virtually everyone would be captured – and would be far more equitable than making the diminishing pool of workers shoulder the lion’s share of the tax burden.

Advertisement

Any tax reform program must also address Australia’s world-beating and poorly targeted tax expenditures – including superannuation concessions, negative gearing and CGT concessions – which are starving the Budget of crucial revenue and are broadly inequitable.

In particular, there is a very strong case to limit superannuation concessions, which have increasingly become a mechanism for richer older people to avoid paying tax, rather than a genuine means for Australians to pay for their own retirement and avoid drawing on the Aged Pension.

The cost of superannuation concessions, which overwhelmingly flow to high income earners, as well as the tax free treatment of superannuation once one turns 60, are ripe areas for reform, both on Budget sustainability and equity grounds.

Advertisement

There are also very good reasons to quarantine negative gearing losses, so that they can only be applied against income from the same asset, as well as removing the capital gains tax concession on investments (why should they be taxed at a lower rate than income?).

Again, the key issue is that tax reform broadens the tax base and shifts it towards more efficient and equitable sources. This requires a shift in sources from productive effort (e.g labour) towards taxes on land, resources, and consumption, along with the closure of generous taxation concessions favouring the old and the asset rich.

An adequate tax take is a vital element for a civilised society. And a high tax take is not an issue provided it is raised in and equitable and efficient way, along with well-targeted expenditure.

Advertisement

But simply relying on never-ending increases in personal income tax via bracket creep, while the base of workers shrinks as the population ages and the proportion of retirees rises, is neither efficient, equitable or sustainable in the longer-term.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.