Today we return to the loneliest man in Davos from Oliver Wyman who predicted in early 2011 that the next GFC will spring from a commodities crash in 2015:

During phase 1 we distinguish between two sources of demand affecting commodities prices: demand for use in the production of other goods (“real” demand) and demand for the purpose of price speculation (“speculative” demand). There are three major groups of players in our scenario. Firstly, there are economies, such as Latin America, Africa, Russia, Canada and Australia, which are the largest commodities producers. Secondly, there is China, which is now the world’s largest commodity importer. Thirdly, there are the developed world economies, such as the US, which are pumping liquidity into the financial system through their loose monetary policies.

As with any bubble, our scenario contains a compelling narrative that allows investors to convince themselves that “this time is different”. In this case it is a story of strong economic growth coming from China creating a sustainable increase in demand for commodities.

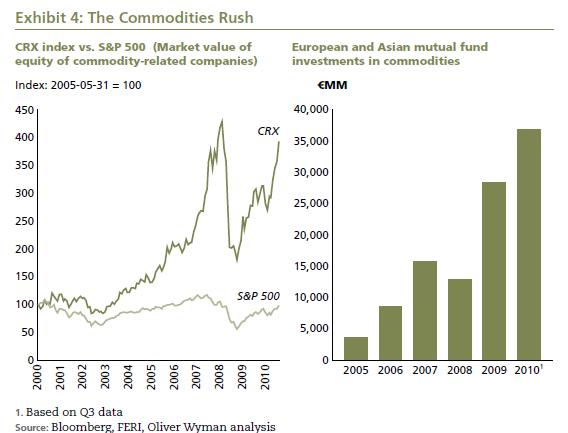

However, it is already apparent that increasing commodities prices are also creating inflationary pressure in China, which is exacerbated by China holding its currency artificially low by effectively pegging it to the US dollar. This makes commodities look like an attractive hedge against inflation for Chinese investors. The loose monetary policy in developed markets is similarly making commodities look attractive for Western investors. This “commodities rush” is demonstrated in the right-hand chart below, which shows the asset allocations of European and Asian investors. A recent investor survey by Barclays also found that 76% of investors predicted an even bigger inflow into commodities in 2011.

Based on the currently inflated commodity prices, commodity producers in countries such as Brazil and Russia have clear business cases for investing in projects to dig more commodities out of the ground. As competition to launch such projects increases, the costs of completing them also starts to rise, with the owners of mining equipment and laborers capitalizing on the increased demand by charging higher rates. Because a portion of the demand for the projects is not coming from the real economy, an excess supply of mining capacity and commodities will be created.

As with previous asset bubbles, we expect much of the debt financing for these projects to come from banks. And much of this bank financing is likely to be supplied by Western banks that are eager to preserve their diminishing return-on-equity and need to find lending opportunities that are sufficiently lucrative to cover their own increasing cost of funds. The balance sheets of life insurers will play a supporting role here, as insurers look for long-term investments that can match their liabilities and seek to earn additional illiquidity premia.

From the FT, several US banks are reporting troubled energy loans:

Now banks are also being affected, with Barclays and Wells said to face potential losses on an energy-related loan. Earlier this year, the two banks led an $850m “bridge loan” to help fund the merger of Sabine Oil & Gas and Forest Oil, US-based oil companies.

Investors, however, balked at buying the loan when it was first offered in June and slumping oil prices combined with volatile credit markets in the months since have scuppered further attempts to sell, or syndicate, the loan, according to market participants. Barclays and Wells declined to comment.

With underwriting banks unable to offload the loan to investors, they are now facing losses on the deal as the value of the two oil companies’ debt erodes.

…If the banks are not able to sell the loan, they may absorb it on their balance sheets rather than try to sell it into the market.

…Marty Fridson, chief investment officer at LLF Advisors, says that of the 180 distressed bonds in the Bank of America Merrill Lynch high-yield index, 52, or nearly 29 per cent, were issued by energy companies.

Advertisement

Banks getting caught with toxic assets as debt markets close to them…that all sounds eerily familiar. The junk bond market is the subject of similar discussion at the AFR:

The plunge in the price is “the most significant risk that could potentially deliver a volatility shock large enough to trigger the next wave of defaults” in junk bonds, Deutsche Bank said.

According to the bank, energy companies now account for about 15 per cent of outstanding issuance in the non-investment-grade high-yield – or “junk” – bond market.

It warned in a recent report that many of these issuers would come under severe financial stress if the price of benchmark West Texas Intermediate (WTI) crude dropped from its current level about $US74 a barrel to $US60.

…Deutsche bases this scenario on average debt leverage ratios of previously distressed issuers in all non-financial sectors. Once the ratio of debt to enterprise value (D/EV) exceeds 65 per cent, a company becomes vulnerable to default, it says.

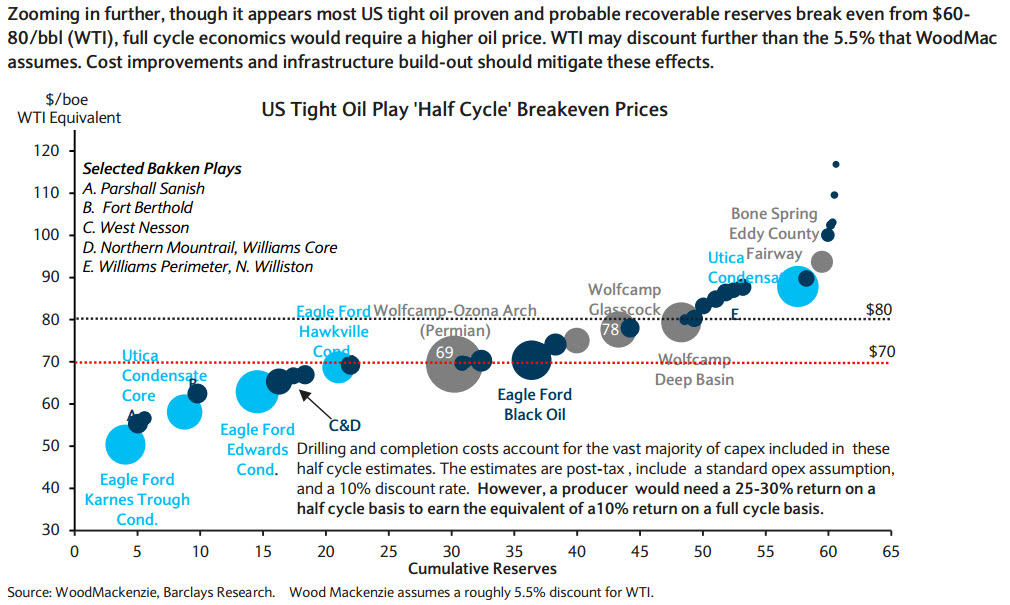

$60 would indeed put most of the US shale producers under water, according to Wood Mackenzie:

Advertisement

We learned overnight that Saudi Arabia has no intention of cutting oil output and FTAlphaville has some good material on what history can tell us about this. The following was dredged from the FT archive in 1961 when a similar bout of competition seized the oil market:

“Independents in oil”

Lord Godber, the retiring chairman of “Shell” Transport and Trading, took the opportunity of yesterday’s annual meeting to reply to some of the wilder accusations that have been made about the international oil companies, notably Signor Mattei’s recent statements that world oil prices were 40-45 per cent too high.

New competitors

Signor Mattei’s ENI is only one, and perhaps not the strongest of the numerous independent companies which are challenging the majors all over the world. It is arguable that there are now too many companies in business, and that, as margins fall, some of them will be forced out of business; thus, equilibrium will be restored to the oil market. This tidy picture is upset partly by artificial factors, such as the need to keep posted crude prices high, and partly by the fact that many of these newcomers are powerful concerns, with a cushion of profitable operations inside the US.

Frank Discussions

The competition that all this has produced can often be bitter. In this particular industry, however, the issuers are too important to be clouded in angry controversy. With growing protectionist pressure both from producing and from consuming countries, it is essential that the facts of the business should be made known as fully as possible. The foundation of the Organisation of Petroleum Exporting Countries may be a step towards franker consultation between the companies and their landlords: wild accusations among competitors can only hinder the industry’s progress.

Advertisement

That is, when one oil monopoly tumbled another rose in its place, but first there was the pain.

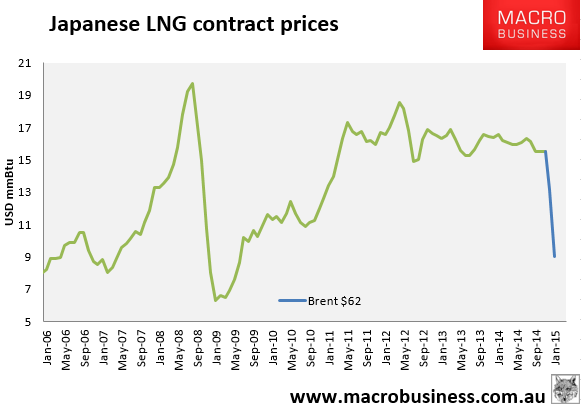

For Australia, the stakes could not be higher. If Saudi Arabia does declare a market share war then the magnificently expensive seven LNG projects are going to be born into a calamitous price crash. $60 oil is the equivalent of $9mmBtu LNG:

Advertisement

None of the new Australian projects will be making money at such levels, given breakevens that range from $11 to $14, though they will keep pumping because the price will still be above their cash costs. The write downs and equity carnage will be huge.

Of course, that is only the narrow industry impact. The bigger problem will be the global debt freeze coming out of the souring debts of the US shale implosion (which would likely drive oil even lower). That will raise funding costs everywhere and threaten Australian banks access to foreign capital, with all of the echoes of the GFC that that implies.

In the longer run, Australia would be a beneficiary of the war if the end result was less oil competition, once the shock had shaken out our costs.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.