by Chris Becker

Citi has an interesting report out on oil given the huge geopolitical shifts going on in Nigeria, Ukraine, Middle East and the US. It truly is a complex picture with such events having little impact on the spot prices of the two major oil markets – ICE Brent and NYMEX WTI crude – and indeed, the Australian landed price.

The main reason is the North American energy boom:

The markets have for good reasons shrugged off geopolitical risks. – The surge in crude oil output from North America is singularly responsible for bringing the Atlantic Basin back from being crude short to being crude neutral with prospects that by this time next year it will be crude long.

Moreover with global supply disruptions hovering around a record 3.5-m b/d, it now looks as though the probabilities of more supply coming back from disrupted markets, including Libya and Nigeria, are potentially greater than incremental lost supply.

Citi therefore sees downside risk on price with this increased supply and lower demand growth:

Demand growth from China, already lower than had been expected at around 2% this year, is at risk again next year, and Citi’s economics team has reduced its global growth outlook yet again for 2015 to 3.4% from bleaker outlooks for China, Europe, Brazil and Japan.

The USD is appreciating more rapidly than had been expected against most major currencies, creating a further headwind for commodity prices, but softening the price impact for producers.

And where do they see prices going?

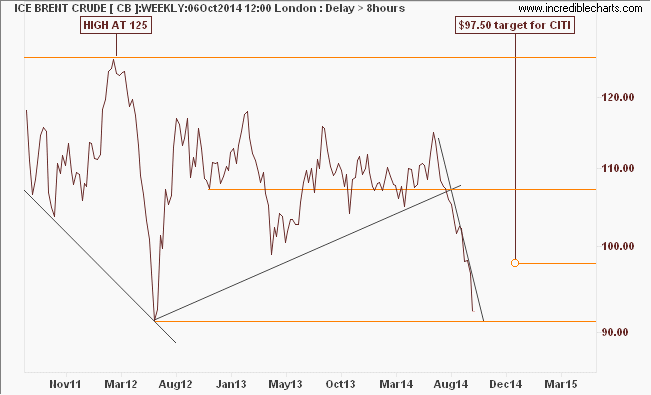

(we’re) dropping our Q4 Brent price to $100 from $109.3, with a neutral outlook for 2015, which we reduced from an average $105 to an average $97.50 and we are staying with that price call for now.

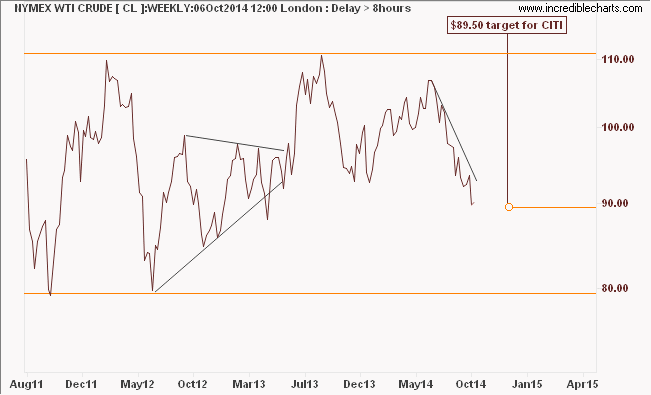

We’ve reduced our outlook for WTI from $99.50 to $89.50 for the year ahead.

The Brent call looks a little aggressive, although the spreads are widening, the correlation in price performance from the speculative side remains high:

The big question is what will the increasingly weaker looking OPEC do with surge an imbalance. Citi opines that the Saudis do not want lose market share by cutting production and will wait out the glut in US shale oil.

For Australian consumers at the pump and primary producers facing potentially higher fuel and diesel prices respectively, this imbalance is likely to see less pain even with a structurally lower AUD.