Fairfax’s Ross Gittins wrote a good article over the weekend questioning the economics profession’s infatuation with Gross Domestic Product (GDP), which Gittins argues is becoming an increasingly useless measure of economic well-being:

To estimate real GDP the bureau takes the nominal, dollar value of the goods and services produced, then “deflates” this figure by the prices of those goods and services relative to what those prices were in the base period.

We commonly take the value of the goods and services we produce during a period to be equivalent to the nation’s income during that period…

But [Saul] Eslake reminds us that “for an economy like Australia’s, the prices of whose exports are much more volatile than those of other ‘advanced’ economies, abstracting from swings in the prices of exports (and imports) obscures a significant source of fluctuations in real incomes”…

Trouble is, real GDP doesn’t capture the effects of these swings…

Next Eslake says that as the resources boom moves into its third and final phase – with mining investment winding down and exports ramping up – real GDP growth will be an even less useful guide to what’s happening to domestic income and employment.

This is because maybe 80 per cent of the income generated by resources exports will be paid to the foreigners…

(A separate issue Eslake doesn’t mention is that the highly capital-intensive nature of mining means the increased production of mineral exports will create far fewer jobs than you would normally expect)…

Last month I wrote an article arguing that “economists’, the media’s, and the Government’s infatuation with GDP is one of the biggest shortcomings in macro-economics”.

This infatuation with real GDP growth has led to spurious (and damaging) policies like the pursuit of endless population growth on the basis that it stimulates headline GDP (more inputs equals more outputs), even though it provides next to no benefits to everyone’s share of the economic pie and arguably reduces living standards of the pre-existing population.

Then there is the focus on the quantity of growth in GDP, rather than the quality (and sustainability) of growth, such as frivolous debt-fuelled consumption and the Government and RBA’s never ending drive to increase house (land) prices and private debt, which creates structural imbalances and damages longer-run productivity and competitiveness.

Finally, there are other anomalies with GDP, touched upon above by Gittins and Eslake, of which there is no better illustration than the pick-up in the volume of commodity exports as the mining investment boom ends. The transition from the mining investment boom to an export boom will see the loss of a large number of jobs – up to 100,000 according to NAB. And yet the rising export volumes will largely offset the negative growth impact from falling mining investment, effectively supporting GDP as unemployment rises materially.

To make matters worse, the increase in export volumes has dramatically lowered export prices (i.e. more goods are being sold at lower prices), yet this reduction in national income is not captured in headline GDP, which only measures volumes produced within an economy.

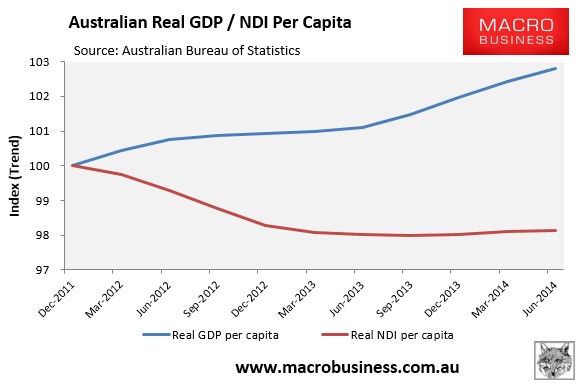

Accordingly, Australian real per capita national disposable income (NDI) has fallen by 1.9% since December 2011 despite the 2.8% growth in real per capita GDP over the same period, with further divergence likely as the terms-of-trade continues to fall (see next chart).

The sooner economists and commentators abandon GDP as a measure of economic progress, and replace it with broader measures of well-being, the better.

As noted last time, the ABS is thankfully developing new ways of measuring Australia’s progress, which includes a bunch of qualitative factors such as health, safety, equality, etc. Let’s hope that it gains greater prominence amongst commentators and policy makers alike.

unconventionaleconomist@hotmail.com