From Moody’s today comes news that Western Australia’s credit rating has been downgraded to to Aa1 from Aaa and the outlook changed to stable from negative (my emphasis):

The ratings downgrade reflects the state’s ongoing deficit position, the deterioration in its debt metrics, and a growing risk that this trend may not be reversed soon. The challenges related to narrowing the budget gaps include greater volatility in the state’s revenue base, reflecting its increasing reliance on royalty income, expenditure pressures related to the rapid expansion in the state’s economy and population, and a weak policy response to the deteriorating financial and debt position.

These trends have led to persistent deficit results with the general government sector’s budget gaps averaging 5.0% of revenues from FY2008/09 through FY2012/13 and, in FY2013/14, the deficit is estimated to be equal to 6.2% of revenues as current expenditures continue to outpace revenues.

The state’s fiscal action plan — implemented in FY2013/14 to reduce its budget gap — including an increase in tax rates and a new wage policy that limits salary increases to inflation, are positive steps but are not expected to lead to significant improvements in the near term. Minimal improvement is expected in the financial performance in FY2014/15, with the gap budgeted to be AUD1.6 billion or equal to 5.7% of revenues, as revenues are forecast to ease in line with slower economic growth.

The state plans to narrow its deficits to 2.5% of revenues on average over the next four years and a low 1.1% in FY2017/18. But improved results will be challenged by an increasing reliance on more volatile mining royalties, which is forecast to amount to nearly one-quarter of revenues by FY2017/18, up from around 8% in FY2006/07. The state’s assumption on royalties is underpinned by a fairly optimistic forecast for iron ore prices.

In addition, the state will be hard pressed to meet its very low spending growth targets, unless the government’s fiscal resolve strengthens and new measures are identified. Projections rely on reducing the average rate of spending to 3.5% compared to 7.1% over the last four years, which incorporates much slower growth in employee costs and a steady reduction in the growth rates of healthcare and other social services. Moody’s notes, however, that flexibility is enhanced by the still high levels of capital expenditures, which the state plans to reduce as current works on large projects — in particular significant investments in new hospitals — are completed.

Western Australia’s debt burden has risen sharply in recent years as the consolidated sector incurred larger cash deficits. Net direct and indirect debt rose to a high 96.5% of revenues in FY2012/13, from a moderate 44.4% in FY2007/08, which is manageable but higher than most other Australian states. Over the medium term, projected cumulative cash deficits could push the debt burden up to 107.0% of revenues by FY2017/18. The state’s debt structure is quite short-dated, with average maturities at three years and short-term and floating-rate debt amounting to more than 50% of total debt in recent years. However, the state is making efforts to lengthen the maturity profile of its debt.

The stable rating outlook is supported by the state’s strong economic prospects and supportive Commonwealth government grants framework. Western Australia’s economy, while easing as mining investment comes off record highs, is still expected to outpace other Australian states, and remain supportive of financial and debt operations. While Commonwealth equalization grants will decline in line with the state’s above average revenue-raising ability, the system remains supportive through special purpose grants, and if economic performance weakens in relation to the other states, equalization grants also would provide a stabilizing effect and rise accordingly.

What Could Change the Rating — Up/Down

The lack of a strengthening in government resolve to slow the pace of expenditures without offsetting improved revenue trends — resulting in wider deficits and continued debt accumulation — could lead to downward pressure on the ratings. A more effective budgetary redress plan that allows the state to return to a surplus position and an associated easingin the debt burden could lead to a rating upgrade.

I am not surprised by this downgrade one bit, given the iron ore forecasts underpinning the Western Australian Budget were always far too optimistic (see here and here).

Advertisement

Moreover, I believe that Moody’s remains far too optimistic in its assessment of the Western Australian economy. As argued in last month’s Perth housing special members’ report:

…the ongoing unwind of both commodity prices (iron ore in particular) and mining investment threatens to cut Western Australia’s growth rate, reduce incomes and increase unemployment.

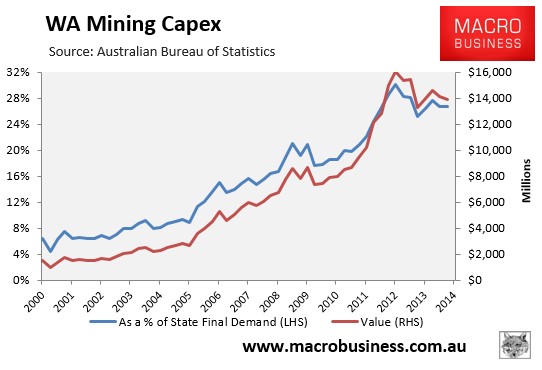

As shown by the above chart, mining and energy-related capex has only fallen moderately from its peak and has much further to fall. Iron ore capex has retraced some way already, supported by the the late arrival of the $10 billion Roy Hill project, which will begin to ship by late 2015. The energy spending spike was even larger, with two major gas projects in Gorgon and Wheatstone accounting for an astonishing $80 billion spend over six years from 2010. Gorgon is now 85% complete and will begin to ship in mid 2015. Wheatstone is about 40% complete and will ship from mid 2016. These three projects alone constitute approximately 20,000 jobs that will be reduced by 90% as construction moves to production.

From engineering to construction and ancillary mining services, tens-of-thousands of Western Australian jobs are now under threat as mining projects currently in the pipeline are completed.

Moreover, with iron ore prices falling sharply and Australian LNG uncompetitive versus the US’s shale gas boom, there will be increasing pressure on mining and energy firms to slash operational expenditure for years to come, which will further weigh on jobs and income growth in Perth. It also means that the likely retracement of the mining capex boom is a fall by 2017 to levels similar to those in the period 2000-2002.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.