By Terry “Macca” McFadgen, former Reserve Bank of New Zealand advisor and multiple CEO

One of the abiding mysteries about the Great Recession is why economies have taken so long to recover from it. Only in recent months has output from the US and UK economies recovered to pre- recession levels-and it is still well below pre-recession levels in per capita terms thanks to seven years of population growth. Europe is even further off the pace.

Nor is there any sign of vigorous growth just around the corner. The US economy is growing at about 2% pa or close to 1% pa in per capita terms. Europe is basically stalled and facing the risk of outright deflation. The UK is an exception but economic growth built on house price bubbles has been tried before and found wanting so the BOE is going to have to close down that party. Japan is growing faster than it has for years but much of that growth is courtesy of a QE induced currency devaluation. China is now slowing and the only debate is by how much. All up it is hard to get excited.

What is more, growth rates are being revised down. As I write the FOMC has revised this year’s growth rate for the USA down to 2.2% and the IMF has revised its long term growth rate for the USA down to 2% from somewhere in the 3%’s.The FOMC is holding to its view that it will raise rates in 2015, but, in open revolt, the IMF says 2017 is more likely.

One possibility is that the Great Recession had some characteristics that caused more damage to the deep tissues of the world economy than its predecessors. If so, time will ultimately repair most of that damage. The other explanation is that cyclical effects are only at play around the margin and some fundamental changes have occurred over the past few decades which have hollowed out the capacity of the developed economies to grow beyond a crawl.

Larry Summers and Paul Krugman are two the smartest guys on the planet and they favour the latter explanation, at least as a strong working hypothesis. We should all listen.

They and their fellow travellers believe the most likely explanation for the long trajectory back to full employment is partly a matter of policy errors (too much being laid at the door of monetary policy and too little being done on the fiscal side in both the USA and Europe) and partly a failure to confront some obstacles to growth which are non- cyclical and have been bubbling under the surface for years. “Secular stagnation” is their catch word.

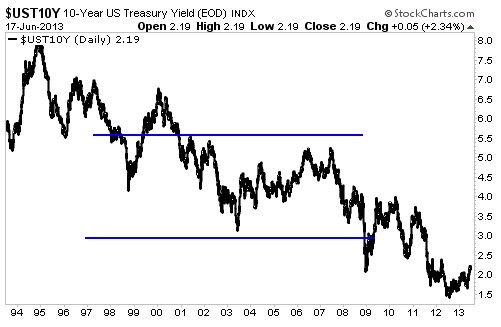

The secular stagnationists invite you to look at the picture of the last 30 years and observe that over that period-with its myriad business and monetary cycles- the long term trend in bond rates has been relentlessly downwards. In other words, for a long time now there has been a consistent and growing surplus of savings over demand for those savings. Repeated doses of cheap interest rates have done very little other than to fuel weak, relatively short recoveries.

Look what has happened to ten year yields since about 1990-they have fallen relentlessly from about 7% to about 2.5% today:

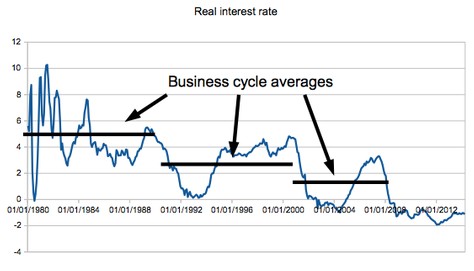

And in a recent lecture at Oxford Paul Krugman presented this following chart, arguing that each business cycle in recent times has seen rates step down to the point where now they are trapped against the wall called “you can’t go lower than zero”. (Note that he is using real not nominal rates in his chart).

The stagnant world envisaged by Summers et al is characterised by low levels of demand relative to potential output (capacity), persistently high levels of unemployment, low inflation, a lot of surplus capital and commensurately low yields on savings (and bonds). This is not the consensus view (except maybe in bond markets) – but then the consensus thought all was good in Q1 2007 so we shouldn’t be too fussed about that.

There are a number of reasons advanced as to why the developed world might have burnt out its growth engines. Here are the most compelling in my view:

Demographics

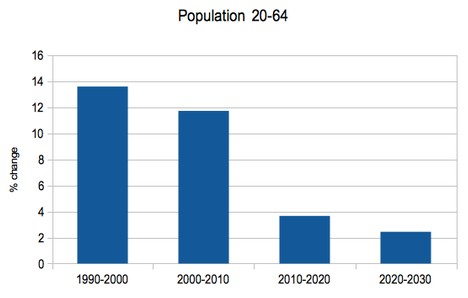

The ratio of drones to worker bees in the developed economies has been deteriorating for decades thanks to falling levels of fertility and a big cohort of baby boomers who now want to be looked after. In Japan these trends are to be seen most dramatically where the workforce is shrinking by about .5% pa. Europe is not a long way behind and even in the USA where the size of the workforce is supported by immigration, legal and illegal, the trend is only static but still declining relative to a positive historical growth rate.

Here is another Krugman chart showing the declining growth rate of worker bees to drones in the USA from 1990:

As the workforce ceases to grow in relative size the demand for capital expenditure shrinks – existing industrial capacity is adequate – and corporate chequebooks are kept in the safe.

The Demise of Manufacturing

Over the last 30 years a huge number of basic manufacturing and assembly jobs have simply been uplifted from the developed economies and deposited in China, India, Vietnam and Mexico as global supply chains have evolved and quality standards lifted in the developing world. A small proportion of these jobs may return but the vast bulk are gone from the developed world for good.

In a similar vein, it is argued that as the developed economies have migrated from manufacturing to services, the required level of investment to support the old economies has fallen (compare the capital cost of a steel mill with say Google’s servers). Facebook serves around 500m customers with a staff of just 2000. In its heyday GM employed 600,000 people!

So maybe the slump we are seeing in investment spending is not just a cyclical event.

Chinese Deflation-Thanks for Nothing

Over the last 30 years China has built a vast amount of capacity in basic materials like steel, aluminium and cement. (Last year China produced as much steel as the rest of the world combined – yes that means the USA, Europe, Japan, India, Korea and Turkey along with a myriad of smaller producer countries.) These business do not need to deliver a return on capital-they serve other masters. An assembly industry built on very cheap labour has had a similar impact on assembly based industries.

Excess Chinese capacity has driven world prices for all basic materials down down-and with it the price of all manufactures. In one sense that has been great for consumers but it has a dark side-and that is deflation.

Deflationary pressure can be helpful, but definitely not when households and Governments are carrying excess debt and are mired in low growth. Deflation prevents debt levels being massaged away by inflation, and it renders monetary policy impotent as rates – even at zero- are stuck at levels too high to be effective in restoring full employment. (Using standard methodologies -e.g. Taylor rule – the level of short rates required in 2008/09 to restore full employment was -5%)

Growing Inequality

Inequality has grown over the last 30 years – whether or not you agree with Piketty’s thesis that it is a systemic problem with capitalism. Twenty percent of American population now own at least 80% of the value of the S&P 500 index, whilst one in five American families have to rely on food stamps.

The problem for the wider economy is that dollars in the pockets of the wealthiest get saved, not spent. In economist’s jargon, the wealthy have a lower marginal propensity to spend on consumption than the rest of us. A dollar in the hands of a family on welfare immediately gets spent on food or clothes, but-a dollar in the hands of the 1% probably gets invested in a mutual fund. Asset values are boosted, but economic activity goes begging and so do jobs.

Stand at Ease Humans!

Gordon Roberts from Northwestern University has taken the theme of declining capital needs even further and has advanced a big picture thesis which goes like this (these are my words not his):

Take yourself back 200 years to the year 1814, and consider your environment. There were no combustion engines (although they were on the way thanks to Watt), and almost no industrial machinery. There was no electricity or electric devices. There were no sewers or clean water for consumption. If you lived in the world’s biggest city – population 1 million – then all your sewage went into the street then into the Thames where it festered, promoting periodic outbreaks of cholera which killed thousands at a time. (London’s sewers were not built until the mid-1800’s)

Heat for cooking and warmth came from coal and wood, and light came from tallow candles. It was unsafe to be outside after dark. Transport was by foot, or by horse for the more wealthy.

There were no radios, telephones, light bulbs or refrigerators, and certainly no cars or aircraft. There were no locomotives or railways and no handy appliances to wash dishes and clothes and do other chores. The computer and the internet were not even dreamt about. Communication – for those that could write – was by a feather dipped in a soot based ink, to create words on paper.

And so it had been for many thousands of years since the discovery of the wheel, the domestication of animals and the discovery of the metals and how to smelt them. In fact, the ordinary citizens of London were probably worse off than free Romans of 2000 years earlier (certainly that was true in relation to water and sewage), and indeed not an awful lot had changed for maybe 5000 years.

Disease and early death were not unexpected. Cholera, typhoid, smallpox, dysentery, tuberculosis and polio were common, and untreatable. There was no treatment for infections. The average life expectancy in the early 1800’s in London was 40 years.

Then followed an utterly extraordinary 200 years which saw the development of the internal combustion engine, the railways, steel ships and industrial plant, electricity, the light bulb, the radio, telephony, powered flight, refrigeration, nuclear power, the microchip, computing and the internet. And of course a myriad of gadgets that make our life a stroll in the park. It is a stunning “event” which we tend to take for granted.

In the process most of the diseases that devastated earlier generations for thousands of years were eliminated from the developed economies, or reduced to miniscule levels. Life expectancies have more than doubled. (As an aside, penicillin was not available for clinical use until 1942).

In parallel with these advances in technology, mankind “cracked “the intellectual challenges of the universe. Thanks To Marshall and Darwin, Crick and Watson, Einstein, Schrodinger, Bohr, Hubble and a handful of others we now know where we came from, how long we have been here and generally how the whole show works.

Gordon’s thesis -put crudely – is that that 200 year burst was unique and it won’t happen again. We have done it. There is nothing “big” to be discovered, which is going to require massive capital investment (e.g. the railways in their time) and henceforth it’s all about refinement around the edges. Mankind is “all done” on the technological front, at least in the developed economies.

This is a glib summary of Gordon’s work which is detailed in the paper noted below and which you will enjoy reading.

The Cyclical Overlays

Plastered over the top of these structural issues are two cyclical problems of major import:

The Boomers Are A Lot Less Wealthy

The Boomers were sitting pretty until the Great Recession thanks to handsome levels of savings – much of which was represented by house prices – and a reasonable expectation of decent earnings on fixed interest investments. Those savings – and earnings expectations – have now been blown away as house prices have fallen (US and Europe) and interest rates are close to zero in real terms.

Boomers are rushing to repair their savings by working longer and spending less. But as the old saying goes one man’s savings is another man’s loss of income – and it may be long time before the boomer “drag”’ works its way out of our economies.

The Long Shadow of the Housing Bust

In their new book House of Debt (recommended), Mian and Sufi estimate that at the beginning of this year about 9 million American households were still under water with their mortgages. If we add to that group those who are sitting at about break even and those who are just a little above that then it is easy to envisage 20 million households who are living from hand to mouth and in great uncertainty about their financial futures. They are not likely to resume old patterns of spending any time soon.

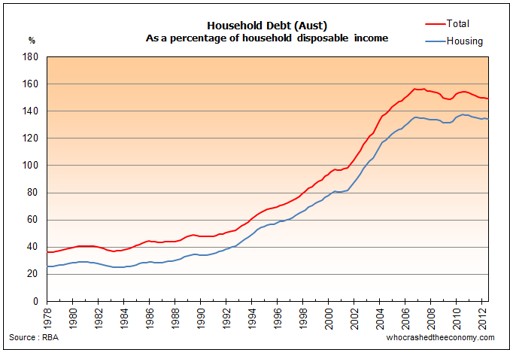

Factor in also the fact that in the Anglo Saxon developed economies household debt levels are still very high, and will inhibit growth in consumption for quite some time. Australia, New Zealand, the UK, Canada and the Netherlands are the major offenders. This chart for Australia tells the story:

So What?

If secular stagnation is indeed where the developed world is heading then what might it mean? Here is a view:

1. Growth will be lower and interest rates lower much longer than markets currently expect. Unfortunately higher unemployment for longer is a corollary.

2. Policy makers face a major problem. Monetary policy cannot revive the tired donkey because the required short term rates (Taylor rule) are negative. So fiscal policy must step into the breach but it won’t because of political gridlock (USA) or German obduracy (EZ). In consequence, a prolonged standoff is in prospect in which the unemployed especially will suffer. In the meantime, significant long term damage to the developed economies may be unavoidable as the unemployed become unemployable.

3. It is hard to see how the European Monetary Union will survive a multi-year period of low growth. Youth unemployment rates of 40-50% (Spain, parts of Italy) are tolerable far a short period as monetary medicine works its magic, but if there is no magic in the wings then the political costs of maintaining a single currency will surely be too high.

It will soon become evident to the world that the EZ crisis has simply been in abeyance and the same hard choices confronted a year or two ago will have to be faced again – this time without the fall-back of a wait and see strategy. Germany will have to choose between breaking up the Euro zone currency bloc (and creating severe headwinds for the German export machine as its currency appreciates sharply), or bringing out the chequebook and paying the south whatever is needed to keep the currency intact. The politics of these choices are horrific, to say nothing of the economics.

Conversely, in the south the prospect of an export revival built on a significant devaluation will become irresistible. There will be defaults on EUR denominated debt, but that will be seen as reasonable price to pay for release from the grip of endless austerity and a lost generation of youth.

4. As already noted the boomers are going to be hard hit in the revenue department. Yields on savings instruments of 3% or so are not going to pay all the bills so consumption will be cut and retirements deferred as long as possible. At some point they may kick up a political fuss also.

The chase for yield will continue unabated bringing the near certainty of a rolling series of asset bubbles. Central banks will face big challenges in finding the tools to manage asset prices. Macro-prudential tools (loan to value ratios, loan to income ratios) are already being utilised at the front line of activity (RBNZ take a bow). The IMF is pushing central banks everywhere to do likewise.

5. Currency wars will continue unabated. The ECB is going to have to join the war in the next 6 months unless European growth and inflation surprises on the up side. The BOJ is already committed to printing until and ink runs out and it is hard to see the Fed allowing the USD to appreciate very much. In this global war, the small currencies will be corks on the ocean and will simply have to live with their fates – unbounded appreciation being the most likely. Buying carry trade currencies will remain one of the trades du jour.

6. In a world of flat demand the pressure on corporates to support earnings by cost-out measures will not abate. This has worrying implications for employment growth, particularly employment opportunities for the unskilled. The implications for a further expansion of social inequality are also serious. Robotics will flourish.

7. If the stagnationists win the day, pressure will increase for central banks to lift their inflation targets to provide more elbow room for monetary policy to work. The IMF is already pushing this barrow.

Any Good News Here?

Actually –yes. Here are four upsides:

1. Current asset prices – which are toppy by conventional measures – may not be all that toppy at all if the “new normal” risk free rate has fallen from the 4%s to the 3%s. That is a big step down in capital costs. Of course the other side of the coin is that the markets may be over optimistic about future earnings, but for those companies with secure earnings the share price benefits could be very real.

As it becomes increasingly apparent that the world is awash with capital and interest rates are going to be suppressed for a long time, sovereign debt levels will become much less of an issue – maybe they have already.

The developing economies are going to look more attractive to investors. Growth rates should be maintainable (no demographic headwinds) and their cost of capital will fall.

There will be a large universe of public (and private) projects able to demonstrate potential levels of return well above their cost of funding. The obstacles will be political not economic. There are some hopeful recent signs from continental Europe that the political barriers may be falling. We shall see.

Something Has To Give

We are getting two very different messages about the future. The first, from bond markets, is that we face ten years of very low inflation, low, growth, spare capacity and high unemployment. The bond market appears to have bought the secular stagnation story. The second, from equity markets is that earnings are going to be fine and will surprise on the upside. Both cannot be right!

Somehow these two views need to converge, either by an equity market correction, or a bond market correction based on significantly higher yields.

Based on the most statistically reliable measure of share values (CAPE), share prices are seriously but not absurdly overvalued. A 25% correction would certainly be no great surprise. Conversely it may be bond yields that move.

In a perfect world markets would just quietly adjust without a lot of fuss. But as Mandelbrot demonstrated that is not how markets behave. They get all jammed up and then release in a flurry of movement.

Macca has no idea which way the adjustment will flow or when it might happen. But judging from the amount of cash still sitting on the sidelines of the investment universe he is not alone. Of course with a few positive surprises that cash could flow quickly into equities and the equities “bubble” could be inflated even further. Or maybe the stagnationists will win the day…in which case its back to “rinse and repeat” for the central banks as they hit their heads against the zero lower bound.

Macca struggles to see how this all ends without a lot more drama.