As noted by Houses & Holes earlier this morning, the Bank of England (BoE) has announced that it will implement so-called macro-prudential controls on higher risk mortgage lending by limiting 15% of all new mortgage lending (per bank) to 4.5 times income.

It is a positive step, and should help to curb housing excesses in places like London, where nearly 20% of mortgages granted in the first quarter of 2014 were at 4.5 times income or more. It should also forestall the need for the BoE to raise interest rates sharply, which could act to drive-up the British Pound, as well as stifle the recovery of the tradable sector and northern regions where housing and the economy remains depressed.

However, while the BOE’s actions are commendable, it is important to not lose sight of the fact that supply-side distortions afflicting the UK housing market are yet to be addressed by the government, which are arguably a far greater impediment to both affordability and financial stability. As noted by The Economist:

Advertisement

Population growth suggests as many as 250,000 new homes are needed in England alone to keep up with demand. Yet construction has undershot that for years: just 112,630 homes were completed in the year to April 2014, a third less than in 2007.

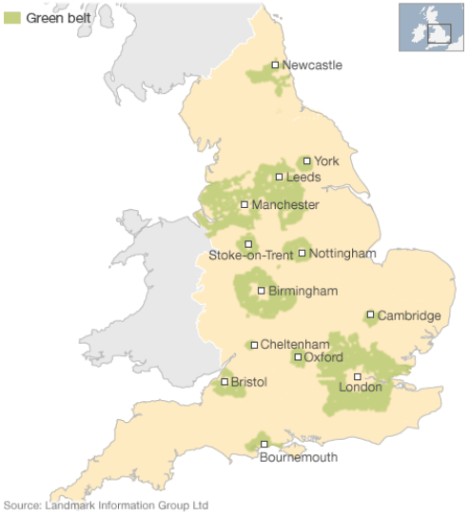

[The Government]…has offered no new solution to London’s unaffordable housing. The green belt surrounding the capital, on which building is banned, will remain intact. House-building will therefore be limited to former industrial sites which are expensive to build on. As a senior civil servant notes, Britain’s housing market is getting back to its pre-recession normal state: broken.

Indeed, while excessive mortgage credit has played a role, the underlying cause of the UK’s housing malaise is arguably its highly restrictive planning system, which has severely limited land supply and forced-up the cost of housing.

Most importantly, greenbelts have been established around UK cities, which have excluded large swathes of agricultural land from urban development (see below graphic).

Advertisement

Strict rules on development have also precluded high-rise development in brownfield areas, further precluding dwelling construction.

These constraints are exacerbated by the centralised fiscal system in the UK, which has created another road block to the provision of housing. Local authorities – which are the primary decision makers on development and have statutory obligations to provide services for new houses – receive very little revenue from increased population and housing. As such, they tend to be biased against development, which limits the provision of housing and related infrastructure.

Advertisement

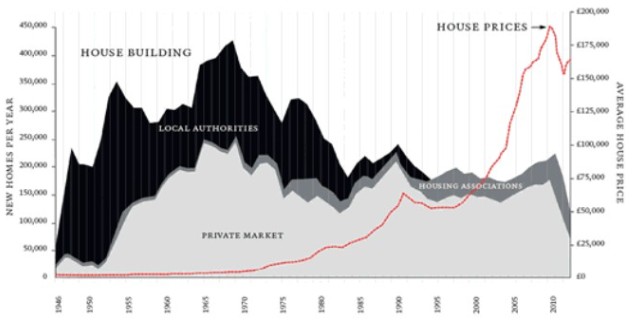

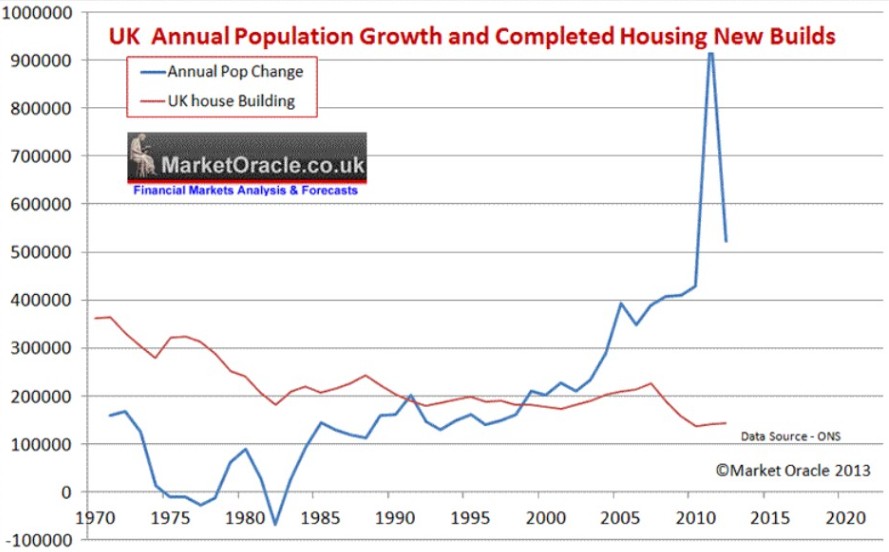

Combined, these regulatory constraints on new housing construction and vertical fiscal imbalances have meant that housing supply in the UK has been incapable of responding to rising demand, with the amount of new homes built in the UK crashing despite rising prices and high population growth (see below charts).

Advertisement

Advocates of the UK’s supply-side often claim that it is short on land and cannot afford to “concrete over the countryside”. However, according to the BBC, the urban landscape accounts for only 10.6% of England, with only 2.7% of the countryside actually “built-on” (see below graphic).

Moreover, as mentioned earlier, the UK is not just afflicted by barriers preventing the urban environment from expanding outwards, but also upwards via height restrictions.

Advertisement

In short, it is government regulation that is primarily to blame for the UK’s housing woes. And while the BoE’s macro-prudential rules will assist in mitigating boom/bust cycles via dampening the credit impulse, they represent a job only half done.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.