Joe Hockey warning about ageing’s deleterious impact on the economy and Budget are set to get a warm welcome from fellow G20 finance ministers this week, whose economies are facing similar, if not more extreme, pressures from ageing than Australia, according to The AFR:

Joe Hockey has once again headed offshore to send his global message local. The Treasurer’s unmistakable warning in Washington that the ageing of the population is a ticking budget time bomb for governments around the world will certainly get nods at the table from fellow G20 finance ministers this week.

In the UK, one in three babies born today is expected to live to 100. George Osborne knows how Hockey is feeling peering ahead at what the Treasurer has termed a “demographic bulge”. Even China is facing a decline in its working age population, courtesy of its contentious one child policy.

One-quarter of the population in advanced economies will be aged over 65 by 2050, pushing up healthcare and pension costs above the current 40 per cent of total public spending…

It is undoubtedly true that the 21st century will be the century of old age, where declining birth rates meet longer life expectancies. And that the ageing of populations across the globe would have major adverse implications for consumption spending, asset values, and government revenues and taxation.

The impacts from ageing would likely be most acute in Western Nations, although some developing countries, most notably China, would also be negatively affected.

The problem stems primarily from the coming end of the demographic ‘sweet spot’. That is, where there is a high proportion of working age people supporting only a small pool of dependents. Such an advantageous age structure has effected almost all of the world’s major economies and produced a population structure optimal to economic growth – that is, where the largest segments of the population were neither young nor old, but in the middle (i.e. working age).

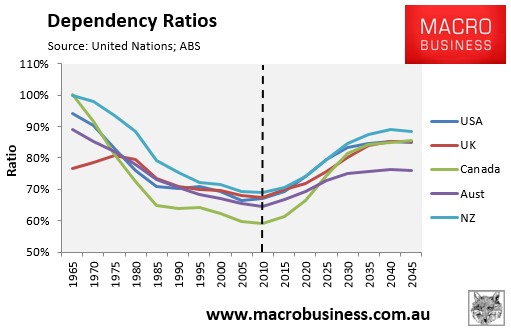

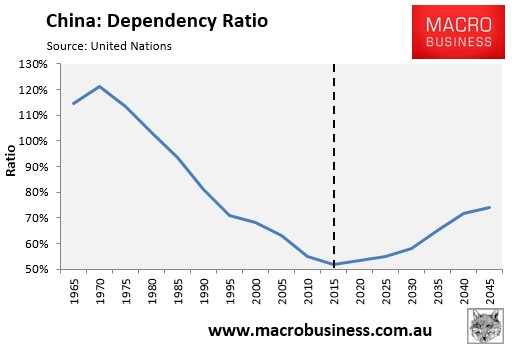

These demographic sweet spots can be seen in the below charts, which show the dependency ratios of each major economy – i.e. the ratio of the non-working population, both children (< 20 years old) and the elderly (> 65 years old), to the working aged population.

In the Anglosphere, of which Australia is a part, the dependency ratios fell steadily in the decades to 2010. However, in the decades ahead, their dependency ratios are projected by the United Nations to rise steadily as the baby boomers retire and their populations age [note Australia’s dependency ratio uses more recent ABS projections, which may not be directly comparable to the UN data for other countries]:

In some major European countries, as well as Japan, their populations aged earlier and their dependency ratios bottomed in the 1990s, which might help to explain some of the economic malaise currently being experienced across those regions:

And China is also staring down the barrel from 2015 as the demographic dividend from the One Child Policy turns into a curse:

The ending of the demographic “sweet spot” means that the high growth rates experienced in the decades leading-up to the global financial crisis were an anomaly and growth is likely to be far more sedate going forward as the world’s population ages and dependency ratios worsen. And although Australia won’t be hit as hard as some other nations, it too will feel the pinch.

Demographic shifts are inherently slow moving, so the impacts from an ageing society will likely be gradual and may go unnoticed by many for an extended period of time. Nevertheless, these longer-term challenges are significant and will likely to alter the path of the global economy and government finances in the decades to come. Hence, Joe Hockey is wise to begin making the necessary policy reforms now before it is too late.

unconventionaleconomist@hotmail.com