For years I have argued that markets where land/housing supply is unresponsive (inelastic) – via planning constraints or geographical barriers – are far more prone to suffer from more expensive housing, higher house price volatility, and bigger boom and bust cycles than markets where land/housing supply is relatively responsive (elastic) to changes in price.

These dynamics were explained in detail in last year’s presentation to a mortgage risk roundtable in Melbourne (available for download here).

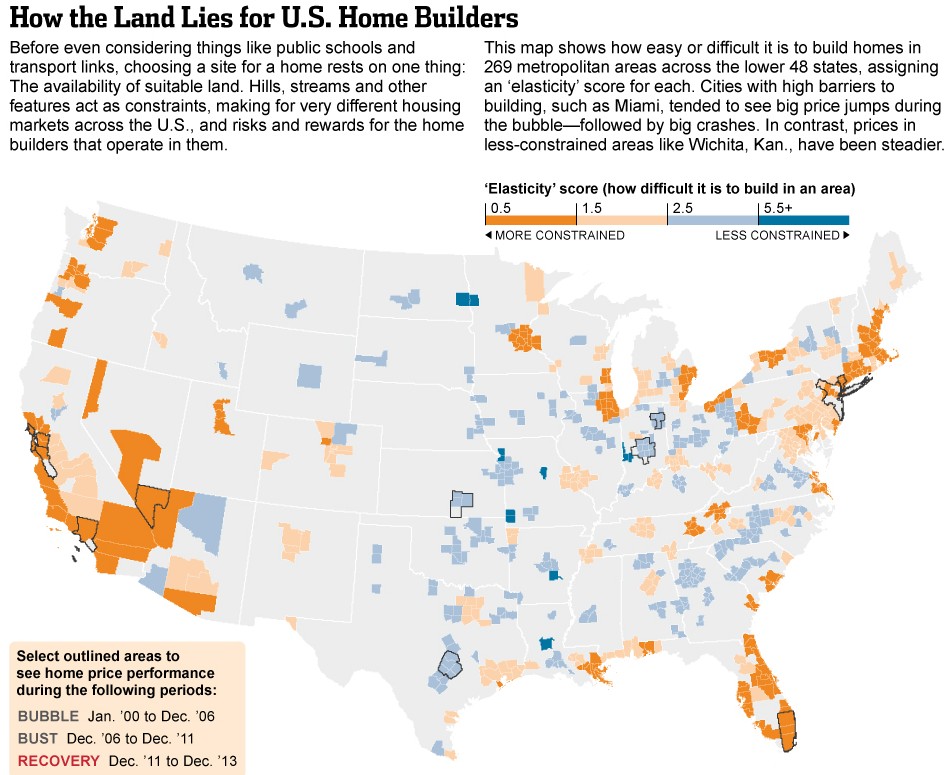

Last night, the Wall Street Journal published a great article explaining how differences in the elasticity of housing supply across the US housing market has affected housing market outcomes, with bigger booms and busts experienced in supply-restricted markets (e.g. California, Florida, Arizona, and Nevada), and the more risky profile of home builders working in those markets:

Advertisement

The crucial difference between housing markets in places such as San Jose, Calif., and Austin, Texas—more important than considerations like quality of life—is the availability of land…

Each metro area [has been given] an “elasticity score”—the higher the number, the easier it is to put up a home. San Jose scored 0.76, ranking it the 10th most constrained among the 100 largest areas by population. Austin, scoring 3.0, ranked a decidedly easier 88th. The range for all 100 was 0.6 to 5.5… the scores correlate with other constraints, such as zoning and taxes…

Tapping this data, economists Atif Mian at Princeton University and Amir Sufi at the University of Chicago’s Booth School of Business have shown that more constrained areas saw bigger booms in the housing bubble—but also bigger busts on the way down.

While house prices in constrained areas have bounced around more than in less-restricted areas, they also have done better over the long haul. Consider two gauges of home prices, one made up of the 10 most elastic areas in 20 separate S&P/Case-Shiller metropolitan home-price indexes, the other of the 10 least-flexible areas. The latter is more volatile but up 65% since January 2000. The former is up 39%…

Constrained builders, conversely, must navigate markets where securing land can be tricky and there can be sudden price declines. But when prices rise, they can do very well, making them more suited for investors with a broadly bullish view on U.S. property…

At the other end of the spectrum… [unconstrained builders]… should offer investors relative insulation if house prices crack. In periods of growth, they should generate steady profits as they buy land, build on it and sell. Their biggest risk may be that they operate in markets where barriers to entry are lower.

The above article summarises why it is so important to liberalise the supply-side of the housing market. Not only does it improve overall housing affordability, but it also reduces price volatility and the potential for boom/bust asset prices as demand changes.

Housing markets where strict regulatory barriers are in place – such as urban growth boundaries, restrictive planning/zoning requirements, minimum lot sizes, and upfront development taxes – are incapable of quickly and efficiently supplying low-cost housing. These supply constraints thereby ensure that increases (decreases) in housing demand feed primarily into higher (lower) prices instead of changes in new construction. The perceived land/housing shortages and rising prices during the upswing also encourages speculative demand and ‘panic buying’ from first-time buyers, which assists in driving home prices up even further. However, when the economy and sentiment sour, such as in the wake of the financial crisis in the US, the slump in housing demand can cause prices to collapse.

Advertisement

By comparison, in housing markets with lighter-touch land-use regulations and planning, low-cost housing is more able to be built quickly and efficiently in response to rising demand. The rapid supply response thereby prevents prices from rising dramatically, which also reduces speculative intent, since there is little prospect of achieving strong capital gains. And with house prices remaining relatively stable, ‘panic buying’ from first home buyers is generally less prevalent. Affordability is also generally much better.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.