RP Data’s Cameron Kusher has produced an interesting post this afternoon on Australian housing values in the wake of today’s December quarter CPI release from the ABS:

The raw capital growth figures show that combined capital city home values at the end of 2013 were 3.5% higher than at their previous peak. When these figures are adjusted for inflation, values are still -4.6% lower than their previous peak at the end of the September quarter in 2010.

Across each individual capital city market, inflation adjusted home values remain below their previous peak. This includes Sydney and Perth where unadjusted figures show values are 10.9% and 3.6% higher than their previous peak respectively. When adjusted for inflation, values across these two cities are currently -0.1% lower than their previous peak and Perth values are -8.9% lower.

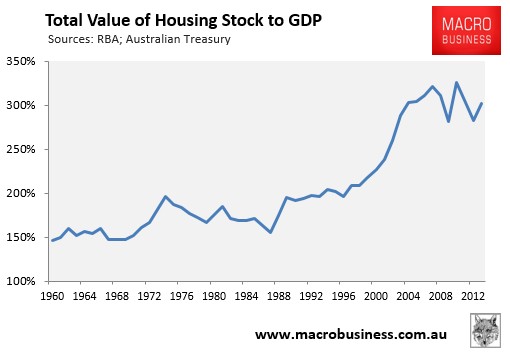

RP Data’s assertion that Australian housing is nearly 5% below peak in real inflation-adjusted terms is supported by the RBA’s dwelling assets data, which was around 7% below its 2010 peak when measured against GDP as at September 2013 (see next chart).

Advertisement

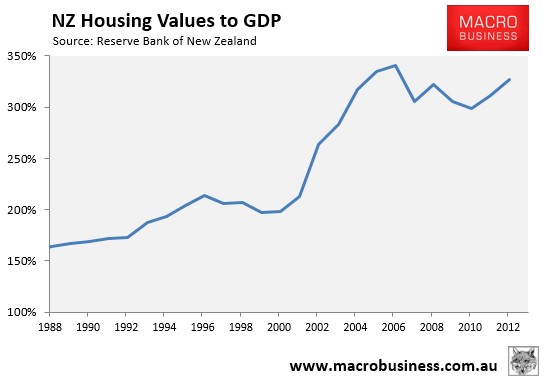

Incidentally, it’s a similar story across the pond, with New Zealand housing values around 4% below their 2007 peak when measured against GDP (see next chart).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.