By Catherine Cashmore, a market analyst and journalist with extensive experience in all aspects relating to property acquisition. Follow Catherine on Twitter or via here Blog.

Since I started writing about housing policy and citing the growing concerns many are having with the rising price of accommodation, it’s been somewhat heartening to see a greater array of individuals acknowledge an undeniable widening gap between existing owners, and a growing pool of ‘wannabe” renters.

Most recently, ALP member for McMahon in New South Wales, Chris Bowen, was reported saying “”I can see the difficulties for young and first home buyers of getting into the market,” citing an ‘affordability crisis’ to be a “serious national issue”.

Whilst many parents would recognise the struggle first homebuyers face and wish for an easier path to enable their children, to gain a foothold into what’s too commonly termed the ‘property ladder’ – as if it’s something to be conquered – emphatic remarks such as those offered above are easy to make when decision-making is out of party hands.

Yet, it was only a few months ago, when challenged over affordability on Q&A, and lacking any real policy initiative going into the federal election, that Chris Bowen remarked:

“There (are) two big things that we can do to help with housing affordability. That’s keep unemployment as low as possible. Because you have got a job, that’s the best thing you can do to get into the housing market. And also to keep interest rates low and interest rates are as low as they’ve ever been in Australia”

No one would doubt keeping unemployment numbers low is an important component to a steady housing terrain – however, as for low interest rates, they have done little more than inflate established property prices and speculation on financial markets, which is scant benefit to those facing rising yields, or paying an inflated cost to secure a property at the offset.

On the same program, Joe Hockey’s comments took a similar stance – except he did touch on the issue of supply:

“..the fact is you’ve got to increase the supply. I mean it’s a market. There is plenty of demand and increasing demand but what are we going to do for supply? I have some plans on that which we’ll be talking about before the end of the election.”

When making these comments, it’s unclear whether Joe Hockey had prior awareness of the Coalition’s plan to abolish the National Housing Supply Council, which was established specifically to identify gaps between housing supply and demand.

Apparently, the council’s activities are ‘no longer needed’ and will be ‘absorbed’ into other departments which aren’t entirely transparent, as Scott Ludlum found when questioning as such. Whatever the reason, it’s clear the current government does not hold supply policy high on the priority list.

As it is, saving hard on an average wage is no longer a guaranteed ticket into the breastfed dream of home ownership – especially if you live anywhere close to Sydney.

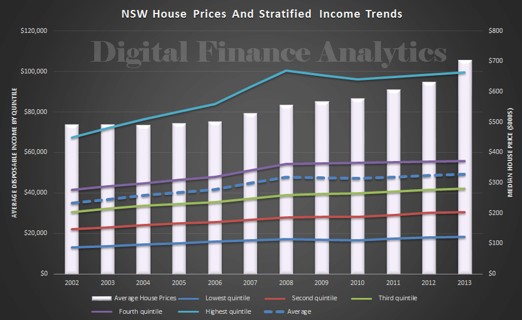

Martin North Principal of Digital Finance Analytics demonstrated this on a recent blog entitled “The Truth about House Price and Income Growth” charting house prices compared to average disposable income across the NSW market back to 2002.

Whilst the higher quartile’s income has kept pace with house price inflation, the other quartiles have only seen their wage grow marginally, his study clearly demonstrates that prices are now outpacing earnings for the larger proportion of residents and therefore effective solutions need to be found.

Of course, each state faces its own challenges, and some are fairing better than others. But presently first homebuyers are clashing budgets with an equal to larger proportion of investors and downsizers and therefore targeting similar stock against those who have an existing equity stream to tap into.

Unfortunately, aside from some tinkering around the edges of housing policy with schemes such as the NRAS, which quickly became over subscribed and jumped upon by SMSF spruikers, it remains a reality that neither political party has yet seen past burdening new buyers with cheap credit by way of grants, low interest rates and incentives, in a vain effort to mask the rising cost of accommodation under the false premise that they’re doing ‘something.’

And Australia faces challenges ahead – with a falling participation rate due to an aging population, fewer full-time positions coupled with a rise in part-time work inflating the ‘underemployment’ figures – job creation is not keeping pace with increases in our working age population.

This was outlined in the freshly released Productivity Commission paper entitled “An Ageing Australia: Preparing for the Future” which projected:

“Australia would have four million more people aged 75 years or older by 2060, with 25 centenarians for every 100 newborns, compared with one centenarian for every newborn in 2012.”

Not only will aging Australian’s have to work to the age of 70, to bridge a shortfall in savings, but the report suggested retirement should be funded in part through a house value ‘equity release scheme,’ claiming:

“House prices have risen over time in real terms, a trend that is likely to continue. Against this backdrop, even under conservative assumption allowing households aged over 65 years to easily access their home equity to help fund health and aged care costs could have a significant impact on reducing fiscal gaps”.

However, under such schemes, not only do Governments have a vested interest in keeping house prices high and rising, they are pinned to the necessity of such to fund future budgets.

Balancing an economy for an aging demographic is not unique to Australia. However, if house prices weren’t as burdensome, requiring an increasing proportion of savings just to enter ownership, not to mention the longer mortgage terms needed to pay down the loan, it would be possible to invest a greater proportion of the household budget into areas of productivity and small business development, as well as channeling savings elsewhere for retirement without the need to use the principle place of residence as a sole equity fund.

In this respect, Australia differs little from its closest Neighbour, New Zealand, where the costs of rising accommodation also bites a good way into a household’s budget for new buyers.

In an article in the New Zealand Herald concentrating on an increasing difficulty accessing ownership following a sensible requirement on lenders by the RBNZ to maintain an 80% loan to value ratio, a young couple were highlighted as a somewhat typical case study.

Putting aside the additional ‘useful’ tips for saving the $90,000 deposit needed for their $450,000 purchase, such as ‘take a packed lunch to work’, it seems the only way this couple were able to purchase adequate accommodation in the Auckland locality was to tap into the ‘bank’ of their respective parents, who borrowed against the accumulated equity in their own home to shore up their children’s deposit.

The couple’s take home pay is $6000 per month, therefore a weighty 50% will go toward mortgage repayments – yet the price of their accommodation is not out of step with what we expect our own duel income first timers to pay for a modest sized home which will provide adequate facility for more than 2 or 3 years.

New Zealand resident and Co-author of the Annual Demographia International Housing Affordability Survey – Hugh Pavletich – makes some sensible comments in relation to this:

“Within normal housing markets with properly functioning Local Governments that have not lost control of their costs, young Jamie Clark and Jenna Close on their household income of $70,000, should be able to buy a new home for about $210,000 with a sensible mortgage load of $175,000 requiring a deposit of about just $35,000.”

Pavletich’s comments are endorsed by Australian Senator – elect Bob Day who in reply to the comment above stated:

“For more than 100 years the average New Zealand family was able to buy its first home on one wage. As you have frequently reported, the median house price was around three times the median income allowing young homebuyers easy entry into the housing market.

As discussed in your report, the median house price is now, in real terms i.e. relative to income, up to nine times what it was between 1900 and 2000…a family will fork out approximately $500,000 more on mortgage payments than they would have had house prices remained at three times the median income.”

The demographica survey rates 337 different housing markets using a “Median Multiple” (the median house price divided by gross annual median household income) to assess affordability. The methodology is a measure recommended by the United Nations and World Bank Urban Indicators Programs and employed by Harvard University’s Joint Centre for Housing – to name but a few.

An affordable market is therefore deemed to be one with a median multiple of 3.0 or less, and whilst it’s never easy to draw an exact correlation between the complexities of international policies compared to our own, the report does provide a basis for research into precisely how other markets with rising populations and relatively healthy economies, manage to maintain their affordable nature.

Supply

The reports primary focus is on supply – removing barriers such as urban boundaries and tax overlays, and portrays the model employed in Texas, where aside from environmental compliance there are no zoning restrictions outside the city outskirts, and planners see themselves as regulators rather than interested parties in town design.

Texas is also a market, which has successfully financed infrastructure by electing local residents onto boards and providing them with access to tax free bonds, which are subsequently allocated for the provision of essential amenities.

Property rights in Texas are clearly strong in nature with limited regulation, covering little more than the land itself – therefore, housing affordability isn’t a burning concern for Texans, and judging by the number of American’s moving there, the market is an attractive one.

Tax

Secondly, as I highlighted last week, markets such as Pittsburgh in the USA, which has a median multiple below 3.0, is an example where land value tax has been successfully employed.

When land value tax is implemented – with the burden taken of buildings and their improvements ensuring good quality assessments and sensible zoning laws – it not only assists affordability keeping land values stable, but also benefits local business through infrastructure funding, discourages urban sprawl, incites smart effective development of sites, reduces land banking, and as examples in the USA have demonstrated – assists in weathering the unwanted impacts of real estate booms and busts.

Speculation and strong tenancy laws

Another commonality shared amongst ‘affordable’ markets is the lack of speculation that inspires the ‘get in quick’ feeling for aspiring owners. Germany is one such example where until fairly recent times; real house prices had remained stable since at least the 1970s.

Home ownership in Germany is not embedded in their culture. And as I pointed out a few weeks ago, strong tenancy laws along with liberal supply policies ensures when time does come to purchase, there is plentiful option to do so without breaking the budget.

Australia?

Whether we will ever achieve the significant reform needed to turn Australia’s housing market into an affordable one is debatable. However, with the rise of the internet and the ability of those searching for answers to delve a little deeper than they perhaps would have done before the world became a mirror of reflections, as every action and movement is recorded, posted and photographed in real time, and offered up for an immediate judgement on social media – it can only be hoped, that a majority, not minority, are taking opportunity to look past the frivolity of what I think most would agree, (whether by design or purpose) have to date been fairly meaningless and unsatisfactory open government debates on housing policy.

In the end, it will be up to the growing generation of struggling first timers and priced-out renters to vote for the brave advocates who enter politics with what are currently deemed unpalatable plans for true and meaningful reform.